ESAF Small Finance Bank Business Analysis

Operating metrics

Loan book composition as on FY23

Microfinance 12250cr (75%)

Retail loans 2610cr (16%)

Agri loans 690cr (4.5%)

Loan to fin insti 619cr (3.7%)

Out of 16%, retail loans 13% ( of total) is gold loans.

Total AUM 16330cr ( AUM as on Q1 FY24 - 17200cr )

75% of loanbook is unsecured ( vs 66% Utkarsh, 73% Ujjivan)

Deposit book 14660cr ( last 2 year CAGR 27%)

CASA deposits 21.4%

Term deposits 78.6% ( Retail 69%, Bulk 9%)

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

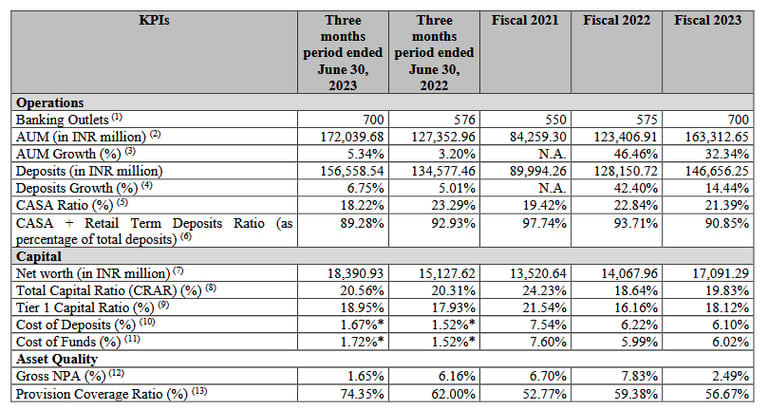

ESAF Small Finance Bank, promoted by Kadambelil Paul Thomas (MD & CEO) started in 1995 as a ESAF Foundation, a microfinance institution, received RBI banking license in 2016. The operate through 700 branches spread across 21 states, based out of Kerala.

Total Asset under management ( AUM) FY23 16330cr, 71% of which is from rural/ semi-urban towns.

Microfinance loan products are of Rs 40000-Rs 1,50,000 ( tenure 12-35 months)

55% of collections are weekly payments ( they have weekly, bi-weekly, monthly payment options for customers)

Total banking outlets 700

Customer service centre 767 ( operated by business correspondents)

Banking agents 2116

ATMs 559

Banking outlets ( major states)

Kerala 304

Tamil Nadu 97

MP 68

Chattisgarh 35

504 of 700 outlets are in 4 states, 43% being only in Kerala.

71% of banking outlets in rural/ semi-urban areas.

Digitization and analytics

1. Customer on-boarding process digitalized for Micro Loans ( doorstep service - account opening via tab)

2. Technology based for underwriting and credit sanctioning ( using analytics)

3. Technology solutions for cashless disbursement of loans - e-sign for loan documents

4. Collections mechanism digitalized through mobile applications

Future plans

1. to increase retail loans ( current 2610cr AUM FY23)- gold loans, mortgage loans, vehicle loans

2. to increase MSME, agri loans

3. increase NRI services, since significant percentage of households in Kerala has NRIs ( 21% of book is NRI now)

4. Target HNIs

5.to offer bank guarantees and letters of credit to MSMEs.

6. to increase fee-based income by cross-selling third-party products

They offer third- party life insurance/ general insurance products, mutual funds, depository services.

Industry overview

Small finance bank scenario is dominated by 3 prominent players, AU Small Finance Bank, Equitas Small Finance Bank and Ujjivan Small Finance Bank, whereas AU has shifted itself from unsecured loans portfolio that is usually done by small finance banks and microfinance institutions.

ESAF's loan book size is 16330cr (bigger listed peers Ujjivan 25000cr, Equitas 30000cr)

Rural India has immense scope in terms of banking sector. 47% of India's GDP comes from rural India, but rural contributes only 8% of total credit sector. With the series of banking reforms like Jan Dhan Accounts, launch of UPI, increasing smartphone penetration and cheaper mobile internet, high speed broadband connectivity to rural- all these combined is going to increase penetration of credit to rural India. Since large and mid sized traditional banks do not have that much presence amongst the currently unbanked section of the society in rural india, microfinance institutions and small finance banks ( all erstwhile MFI) are best placed to capitalize on this growth story.

Microfinance sector had been hit from loan defaults due to covid, but most players have recovered from . Usually, despite doing unsecured loans and lending to the unbanked section of the society, good microfinance institutions or SFBs (small finance banks) maintain NPA (non-performing assets) levels comparable to the best traditional banks catering to the upper, middle class or corporates.

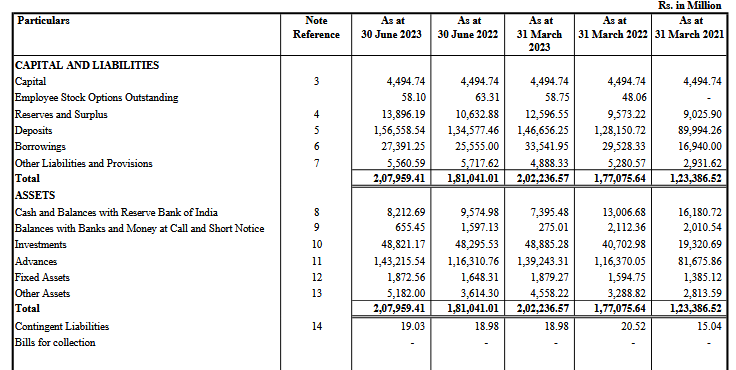

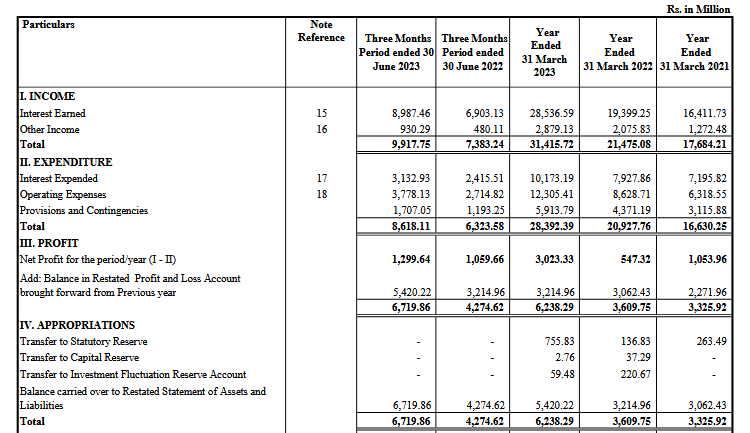

Financials

Operating profits of 890cr ( became > 2 times in 2 years)

PAT 300cr ( close to 3 times in 2 years)

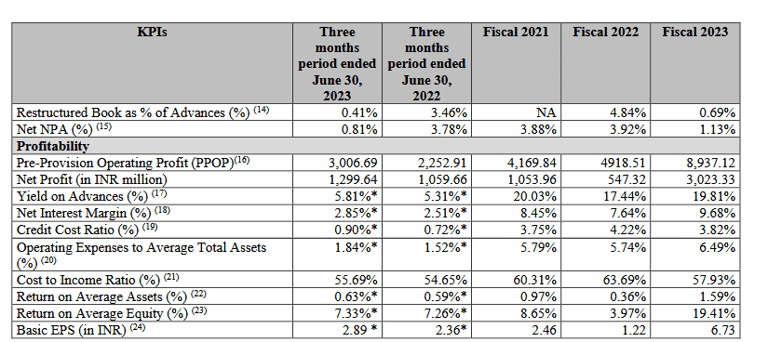

Gross NPA of FY23 is 350cr ( GNPA 2.49%) ( Ujjivan 2.62% )

GNPA FY22 7.83% , FY21 6.7% FY24 Q1 1.65%

NNPA 1.13% ( FY22 3.9%) Q1 FY24 0.81% ( Ujjivan 0.06%)

1090cr amount write off+restructured in FY23

Provision coverage 57%

Financial ratios ( FY23)

Comparable peer Ujjivan/ Utkarsh

Cost of funds 6.19%

Yield 19.8%

NIM 9.68%

Rates similar to Ujjivan, Utkarsh

Cost to income 58%

Credit cost 3.82% (Ujjivan 0.09%)

ROA 1.59% (Ujjivan 3.86%, Utkarsh 2.1%)

ROE 19.4% (Ujjivan 31.8%, Utkarsh 22%)

CRAR 20.5% ( Tier 1 18.95%) Q1- 20.5%

Points to consider

Overexposure to Kerala (43% of loanbook) and Tamil Nadu ( 22% ) can bring stress to loanbook if specific natural/ economic events affect these states. 65% of book- 2 states.

Very fast growth ( 39% AUM CAGR last 2 years) of loanbook was possible as it was < 10000cr. With loanbook crossed Rs 13000cr now, growth rate may taper as was seen in other peers.

Though interest rates are similar, Equitas is strong competition working in South( 50% business from Tamil Nadu) .

Credit costs are quite high at 3.82% vs peers.

Largest markets of microfinance are UP, Bihar, WB, Odisha, Tamil Nadu- where UP, Bihar are the most underpenetrated in terms of credit. Barring Tamil Nadu, ESAF SFB does not have much presence in these states.

Valuation

ESAF SFB is valued at Price/ Book ratio 1.57 ( FY23) and 1.46 at FY24 Q1. Comparable peers Ujjivan at 2.7 and Utkarsh at 2.1

Detailed analysis of Utkarsh Small Finance Bank ( recent IPO)

Follow us on twitter

You may be interested in

PB Fintech Business Analysis

Will Jio Financial disrupt Bajaj Finance

How to avoid companies like Brightcom/ BCG ? Investing red flag

SBFC Finance Business analysis

#themoatinvestor #dmoatinvestor #esafsfbipo #listinggain