SBFC Finance Business Analysis

Contents

History of company

Industry overview

Geographical presence

Operating metrics

Financials

IPO Size & utilization of funds

Points to consider

Valuation

1.History

SBFC Finance, based out of Mumbai, started in 2008, is an NBFC which offers secured business loans and loan against gold to MSMEs and individuals ( mainly targets self-employed), serving the underbanked and unbanked segment of the society.

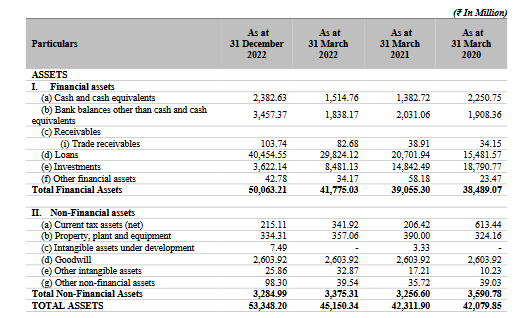

Total loanbook size or AUM of 4415cr ( Asset under management) .

2.Industry overview

In the small ticket business loans to MSMEs, MFIs ( microfinance institutions) like CreditAccess Grameen, SFBs ( small finance banks) like Ujjivan, Equitas, affordable housing companies like Aavas, Homefirst, Aptus and other NBFCs are working, none of them are focussed solely on MSME loans, so directly comparable listed peer is not there. Paytm is also targeting MSME credit sector for their next growth leg( through NBFC tie-ups), but they don't have any physical credit underwriting process.

Size of secured MSME/ individuals credit (Rs5-30 lakh ticket size) is Rs 2,50,000cr. Segment growing at 24% CAGR for last 5 years. NBFCs has 51% market share in this.

7 crore MSMEs employ 11 cr Indians and contribute 30% to India's GDP. Credit penetration amongst MSME is only 15%, leaving a huge scope of credit business to this sector.

With UPI players like Paytm/ Phonepe aggressively encouraging MSMEs to take digital payments ,digital trails being created, which can be used for extending credit along with traditional methods can increase scope of credit lending.

Since large and mid sized traditional banks do not have that much presence amongst the currently unbanked section of the society in rural india, microfinance institutions and small finance banks ( all erstwhile MFI) are best placed to capitalize on this growth story.

MSME Sector had been badly hit in CoVid, now showing signs of recovery after government announced a string of breathers in the form of interest subvention, waiving off 20% of loans taken ( govt backed)

3.Geographical presence

SBFC operates across India through 137 branches , distributed evenly. South contributes 38%, North 31%, West/East 38%.

Top 4 states contribute 61% of business. Out of these, urban credit penetration in Karnataka, Maharastra, Telengana is high wrt other states, but enough scope exists in Tier 2/3 cities and rural credit where SBFC mainly works.

Karnataka 17%

UP 15%

Telengana 12%

Maharastra 11%

Haryana 6%

4.Operational metrics

Total loanbook of 4415cr, mainly focussed on small business loans secured against owned residential property.

Business loan /LAP 77%

Gold loan 19%

Others 4%

For business loans, SBFC focuses on self- employed section with CIBIL score >700 and monthly income < 1.5 lakhs/ month. They do 100% in-house sourcing of loans through 1900 strong sales team via door-to-door, referrals, and other traditional as well as digital methods.

90% of collections are non-cash de-risking cash management problems.

Average loan to value (LTV) stands at 43% ( norms < 75%).

AUM is growing at 43% CAGR for last 2 years making them one of the fastest growing lenders in the sector.

Coming to financial ratios, since we don't have directly comparable listed peer, ratios have been compared with nearest similar business is of affordable housing finance ( Average ticket size Rs 10lakhs)

NPA levels are higher, but even in covid, NPA levels (F 21 GNPA 3.2%, NNPA 2%) didn't shoot too wide from average that happened for other NBFCs and even PSU banks, which is unusual, so NPA recognition mechanism should be checked for better understanding.

Capital adequacy > 20%

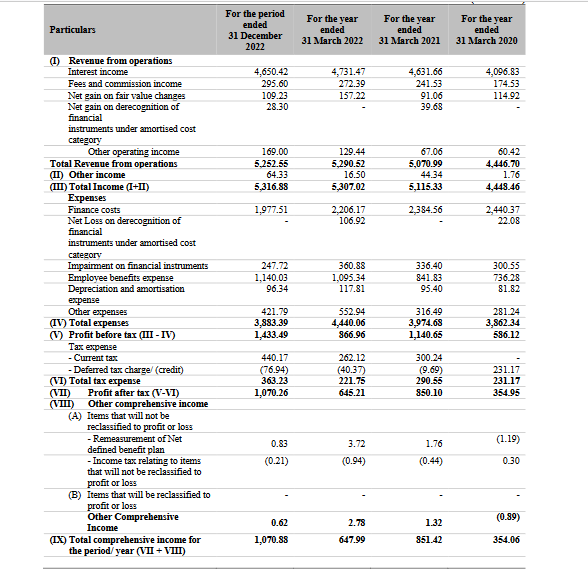

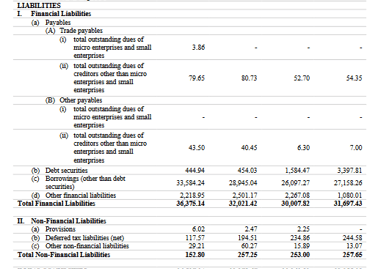

5.Financials

PAT has grown from 35cr in F20 to 150cr in F23, which is very good.

Bad assets recognized in P&L in F20 was 32cr, in F23 it is 24.7cr ( as on Dec22)

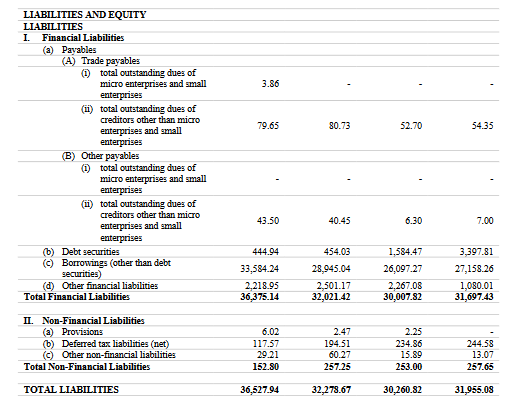

88% of borrowings are term loans ( majority from banks, rest NBFCs)

7.Points to consider

MSME sector is very vulnerable to the economic shocks, they are the first ones to get affected and last ones to get out to recovery mode, so any economic shocks will adversely affect SBFC as it is fully dependent on this sector. ( Though SBFC has started affordable housing finance in Dec '22).

As the access to UPI data gets democratized, they will face stiff competition from SFBs and other NBFCs entering this sector, also competition from PE funded Paytm, Phonepe is also there .

8. Valuation

Listing Valuation P/B ratio ( Price/ Book) of 2.3 whereas other peers trade at P/B of 3.5- 4 .

#sbfcfinanceipo #themoatinvestor #DMoatInvestor #stockanalysis