PB Fintech-Policybazaar

Contents

History & brief of company

Industry overview

Business model

Operating metrics

Financials

New Business

Moat

Points to consider

History & brief of company

PB Fintech started in 2008 as an insurance comparison and insurance education website by Yashish Dahiya, Alok Bansal and Avaneesh Nirjhar. In 2011, they launched their insurance web aggregator site, Policybazaar.

In 2014, they started another platform, Paisabazaar , an online credit comparison website.

In 2015, they launched their Policybazaar app. In 2018, they turned unicorn following Softbank investment. In 2021, they obtained insurance broker license from IRDAI. Finally in Nov 2021, they launched their IPO.

In India, insurance is subject to lot of mis-selling , and mainly driven through agents. Yashish Dahiya started Policybazaar to solve this problem, to bring transparency in insurance purchase.

Currently, Policybazaar has a monopoly in web aggregator insurance model, with 93% of policies sold through their platform. 65% of policies sold digitally are through Policybazaar. ( rest mainly through direct insurance co websites). Their another business Paisabazaar is largest online credit marketplace , with 51% market share. Here they matches borrower and lender. Off late, they have entered UAE market also.

2.Industry overview

Insurance industry

According to IBEF, Life insurance industry is 7,32,000 cr ( F22) in terms of GWP ( Gross Written Premium) and non-life insurance industry ( health, motor, fire, marine, others) is 2,56,000 cr (F22).

Life insurance penetration in India is 3.2% ( Japan 5.8%) and non-life penetration is 1% ( Japan 2.2%).

Distribution mix looks like this

So, individual agents and banks control 77% of distribution in life insurance. LIC, the giant, has 53 % market share in life insurance, followed by SBI life, HDFC Life.

In non- life, individual agents and brokers form main channel of distribution- in health 56%, and in non-life excluding health, 59%. Apart from this, direct selling constitutes 32% in health and 21% in non-life excluding health.

So it is important to understand that these traditional channels won't be disrupted by online aggregators since insurance as a product is a complex one , compared to what is happening in online retail ( apparel, footwear).

In health, govt. players (New india, Oriental, United, National) control 48% of market, then Star health 14%.

In motor, New India 12%, ICICI Lombard 10%, Bajaj finserv 7%, Reliance capital 5.5%, HDFC Ergo 5% are leaders.

Other Insurance web aggregators

Competitors of Policybazaar are Turtlemint, InsuranceDekho, Renewbuy, Coverfox. Policybazaar is atleast 10-12 times bigger in size, so not much threat from these players.

Other significant competitors are Acko ( F 22 revenues Rs 1300cr), who have tied up with Amazon. Paytm is entering the space, having taken insurance broker license recently. Reliance Jio Financial services is entering this space.

IRDAI, the insurance regulatory authority, has been very active in last 2 years, and brought out several policy changes to improve insurance penetration, including raising FDI cap on insurance investment. IRDAI have announced to launch an insurance aggregator portal called BIMA SUGAM, which will list all insurance policies sold in India, and will allow agents/ customers to access and process insurance policies online without traditional documentation ( usually followed in rural). This can be a gamechanger for the industry and may adversely affect Policybazaar's growth.

Credit marketplace industry

Household debt/ GDP in India is 14% ( China 62%, US 66%)

Consumer credit industry is 45 lakh crore ( F21) projected to grow at 13% CAGR. Digital lending industry discussed in detail in analysis of Paytm.

Competition of Paisabazaar are Bankbazaar ( F23 revenues 160cr), other smaller players are Creditmantri, Wishfin.

Paisabazaar controls 51% market share .3.Business model

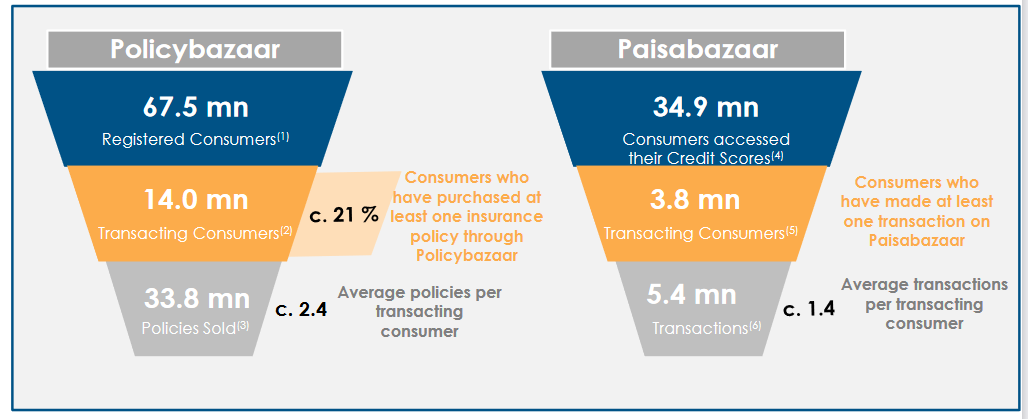

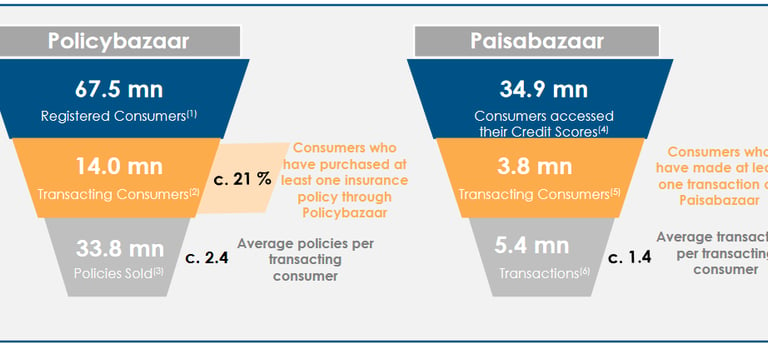

65% of policies sold digitally is through Policybazaar.

But in terms of GWP, out of 9.9 lakh crore industry, Policybazaar GWP 11590cr. So Policybazaar market share is 1.2% of total insurance industry.

So very few policies are sold digitally today.

PB Fintech earns revenues mainly from its 2 main businesses1. Policybazaar platform

2. Paisabazaar platform

1. Policybazaar platformPolicybazaar earns through commissions on insurance sold on its platform. It earns around 5.5% commission overall. ( amounts are different in case of renewals and new policies). More renewals means more profitability for company as cost of acquisition of customer is not there in case of renewal.

For insurance companies, cost of distribution becomes less through online, it is more for other channels like brokers, agents.

Because of this reason ,some of bigger insurance companies are aspiring to develop their own digital channel so that they save on this also.

Policybazaar sells more health insurance policies currently .

For health, they have tieups with leading players Star health ( market leader 14% market share), and Care, Max, Aditya birla - all these players control 23% of health market.

For motor insurance, they have tie ups with leading players like New India ( 12% market share) and others like Reliance capital, SBI general, Sundaram - together these players control 23% of motor market.

For life insurance, they have tied up with all leading players- LIC, HDFC LIFE, ICICI Pru life, SBI life- who together control 82% of the market.

Actually,bancassurance partners have very little incentives for selling one life policy, making it unlucrative unless they sell very high number of policies. That may be the reason why all major players have tied up despite having their own strong distribution channels as mentioned earlier.2. Paisabazaar platform

Paisabazaar gets 20 lakh monthly enquiries.

It has 3.5 crore registered consumers, and credit disbursed to 38 lakhs customers till date.

Paisabazaar has tieups with 4 credit rating bureau, it give customers to get their credit scores (CIBIL) checked for free , instead they use that data pool and forward that to lending NBFCs / banks with whom they have tieups, thus helping generating leads for credit cards, personal loans, business loans, instead earning commissions against successful loan/ credit card disbursal.

They have tie-ups with 54 lending partners ( HDFC, Indiabulls, Homefirst, Rattan india, HDB etc)

66% of loans disbursed through Paisabazaar came to Paisabazaar directly or online brand searches. ( organic traffic)

Revenue breakup

Core commissions income ( Insurance and Credit ) constitutes 37% of revenues. Out of the 27% insurance commission, 60% is generated from new business premium and 40% from renewals . As they add more customers, renewal commissions share will keep increasing ( renewals are high margin business). 80-90% of renewals are happening in health insurance.

Online marketing/ consulting constitutes income from bulk emails, ad banners of different products on the website, and credit score advisory given to credit companies.

Outsourcing services constitute services provided to insurance partners like telemarketing , post sales/ service , account management, and premium collection ( new/ renewal)

Others constitute sales of lead information to banks/ NBFCs.

Rewards are received from insurance partners based on volume targets they achieve.

4. Operating metrics

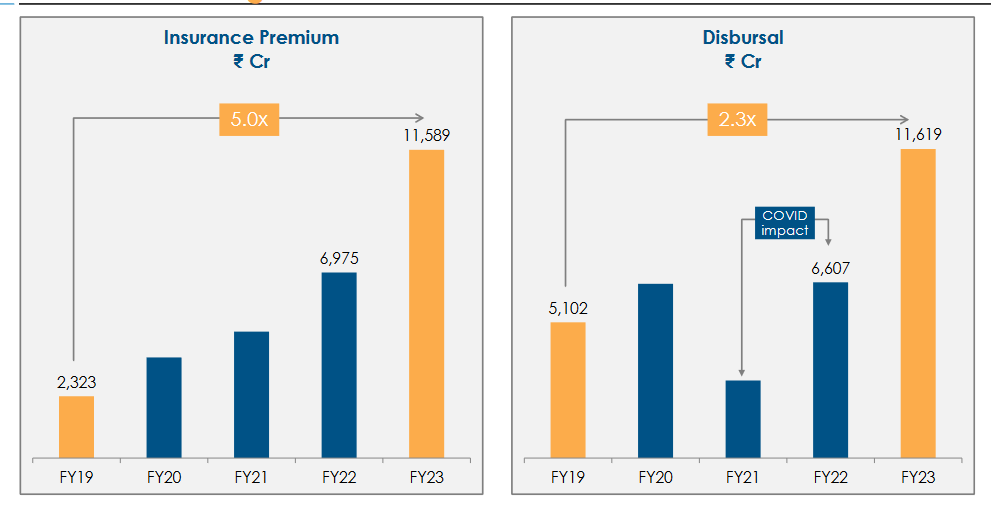

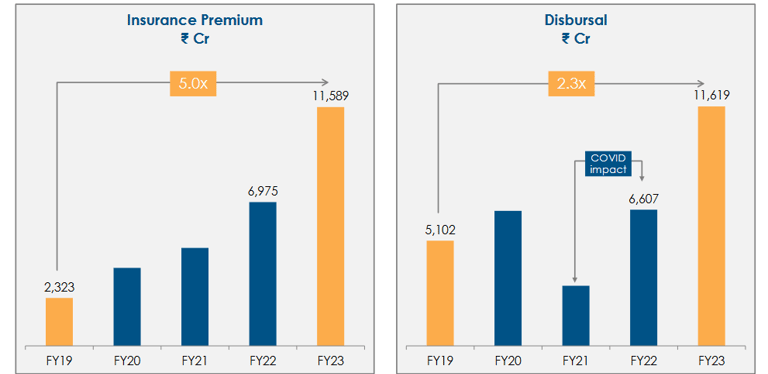

Insurance premium have grown 5 times in 4 years, and credit disbursed have become 2.3 times in 4 years.

80% of motor/ travel insurance happens unassisted, increasing efficiencies.

For others, they have a large telecalling team who assist customers to fill up and make payment of policies over phone, within 15 minutes, leading to better conversion of enquiries. Policybazaar is providing sales support calls in regional languages.

They run TV campaigns in regional languages.

On ground claims support TAT is 30 m.

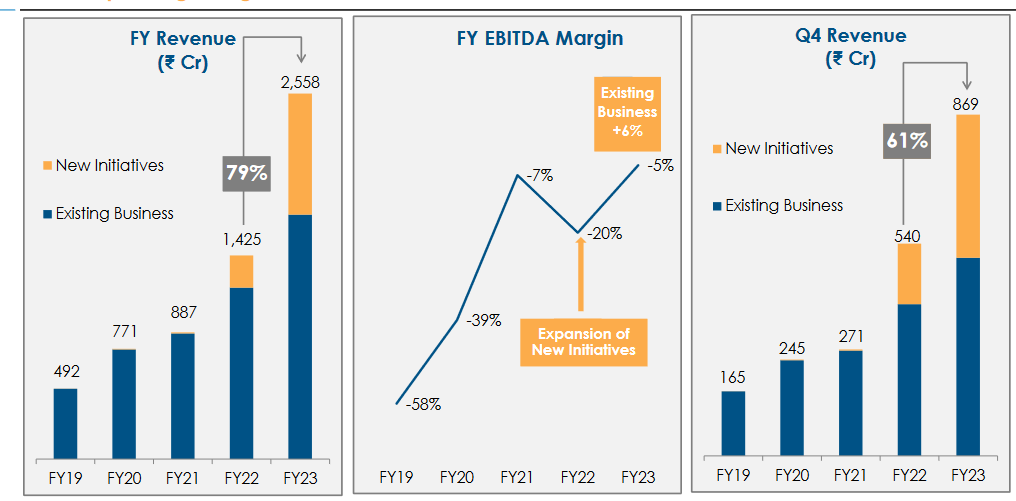

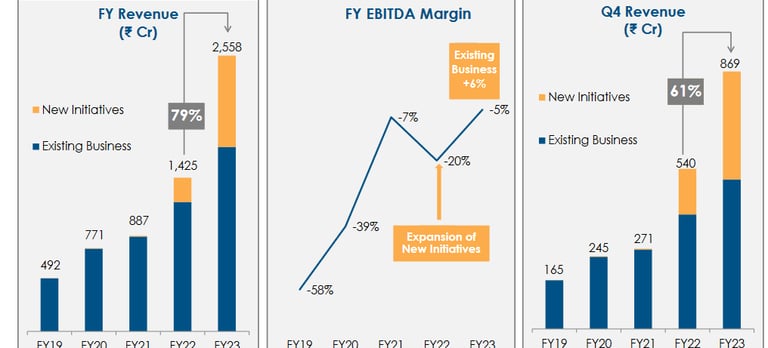

5. Financials

Revenues have grown 5X in 4 years. EBITDA margins have improved.

Existing business revenues are Policybazaar and Paisabazaar.

New business consists of PB Partners- which is a platform for insurance agents where they can generate leads for themselves and manage them.

1 lakh agents are registered on the platform. Tier2/3 cities give 69% of business.

Another wing is PB Corporate, which is for employees, group health policies, property insurance policy.

Contribution margins of existing business has crossed 40% which is healthy.

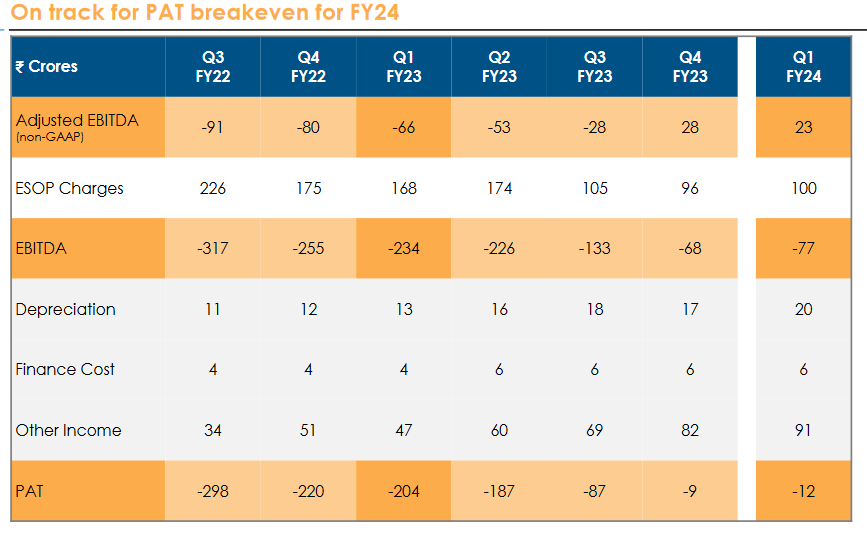

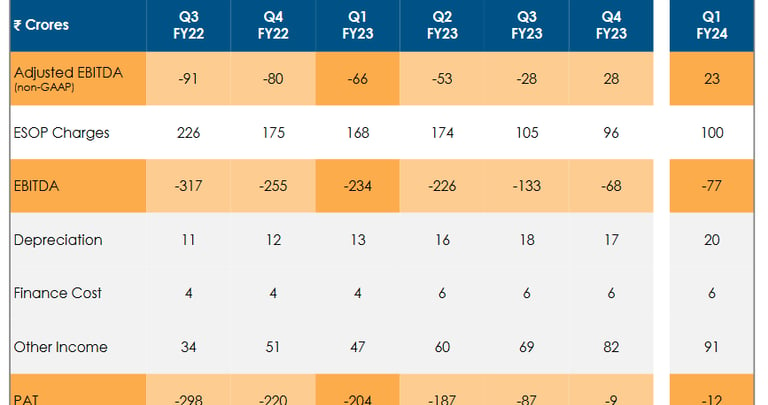

540cr of ESOP cost is a drag on profitability.

Major expense heads

Employee cost 1540cr

Ad expenses 1360cr

Network/ internet 96cr

Other cost 225cr

PAT has almost turned positive in last 2 quarters.

Balance sheet

Trade receivables 677 cr (26% of revenues)

Cash/ bank balance 762 cr

New Business

In F 22, PB Fintech decided to take insurance brokers license and go offline as health and life insurance being complex products, personal touch is important.

They have opened 77 centres in 57 cities and providing on-ground sales support in 125 cities. Their advisors after cold- calling are offering free home visits for insurance plan discussions with potential clients.

Policybazaar is also working on curated motor plans like pay as you drive using based on actual km driven.

They have also expanded their operations to UAE. Premium in Q4 was 111 cr.

Moat

93% market share in insurance marketplace is a moat for them and network effects at play will enable them to sustain this, unless Bima Sugam disrupts this.

Similarly for Paisabazaar, they have 51% market share, can be more stronger if they are able to gain more. It is not monopolistic, has other competitors like Bankbazaar.

Huge customer data on both platforms give them opportunity to cross-sell those to insurance and credit companies, thus generating revenues. As more customers enrol on the platforms, they keep generating more data.

As per company, claim rejection rates for policies issued through Policybazaar are half of the industry rejection rate.

Renewal income is very high , so as Policybazaar adds more customers , and are able to retain them, renewal income forms a majority. This is leverage at play.Points to consider

Launch of BIMA SUGAM can be a big threat to Policybazaar. Overall they earn 5.5% commission on premium. If BIMA SUGAM, launches, supposedly they have announced they will do that at 1/4th of current commission structure , so Policybazaar has to reduce commission too to compete. That will erode margins. Plus Bima Sugam will be direct competition .

Company said it will be profitable in F 24, but opening of offline stores , cost of operating them will be overhang on its profitability. Plus its venture into UAE. High ESOPs cost is another drag.

Insurance sold through Policybazaar is 1.2% of total life+ non life policies sold in india.

Banks, agents, brokers remain dominant distribution channels for insurance and will dominate.

ICICI Lombard is not on Policybazaar platform, if similarly other market leaders prioritize their own digital channels, and seize tie-ups with Policybazaar, they will be negatively impacted.Other posts you may enjoy

How to avoid bad companies like Brightcom (BCG)? Investing red flags

How to do IPO Analysis for listing gainFollow us on twitter

#PBFintech #fintech #stockanalysis #themoatinvestor#policybazaar #DMoatInvestor