Paytm Business Analysis

Contents

1.History & brief of company

2. Industry overview

3. Business model

4. Operating metrics

5. Financials

6.Moat

7.Points to consider

1. History & brief of company

Paytm, started in 2010, by Vijay Shekhar Sharma, as a prepaid mobile & DTH recharge platform, later added payments gateway feature in 2012, and the Paytm Wallet in 2014, which made them a household name. Then in 2015, they introduced utilities like metro payments, electricity bills, gas.

Post widening their user base, in 2016, they entered online ticketing, event booking, and online shopping (Paytm Mall), in order to create a complete ecosystem that keeps their customers engaged in a multi-utility app.

Paytm was late mover in adopting UPI , they joined in 2018 . Recently, in 2020, they entered co-branded credit card business, and in 2021, entered digital lending space (in partnerships with NBFCs) to consumers and merchants.

Today, they look at digital lending as their next lever of hyper-growth. In Nov 2021, Paytm brought IPO and got listed.

Recently, Paytm has entered stockbroking and insurance broking business also.

2. Industry overview

According to a PWC report, the $ 3 trillion digital payments industry of India in 2021 is pegged to grow to $ 10 trillion by 2026 .

According to their data, in 2022, volume of different digital transactions

UPI 63%

Credit /Debit cards 9%

Internet banking/NEFT 15%

UPI market share

Phone Pe 46%

Google pay 34%

Paytm 14%

Others 6%

UPI registered customers of Paytm is crore, whereas that of PhonePe is 38 crore.

Amongst digital payments, highest transactions occur in B2B ( business to person), then B2B, then P2P ( person to person) and then P2B ( person to business).

35-40% of MSME lending is unmet in India, which represents the unorganized business sector .

Digital merchant payments industry is to grow from $ 300-400 bn in 2021 to 2500-2700 bn in 2026 (6-8x) .

Today, 3 crore merchants accept QR code payments ( 75% penetration)

Upcoming govt. reforms like ONDC , OCEN, CBDC are going to further change the industry.

BNPL ( Buy now Pay later) is another emerging trend, which was 1 lakh crore in 2020 is set to increase to 7-8 lakh crore in 2026. In 2021, 20% of BNPL was digital, which will be 40% in 2026.

3.Business model

Paytm earns revenues from 3 heads

1.Payments business ( customers/ merchants )

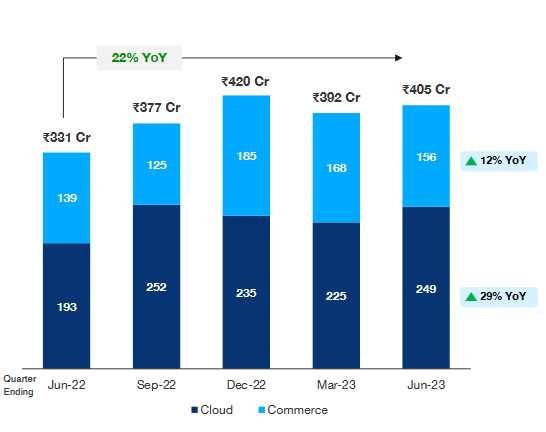

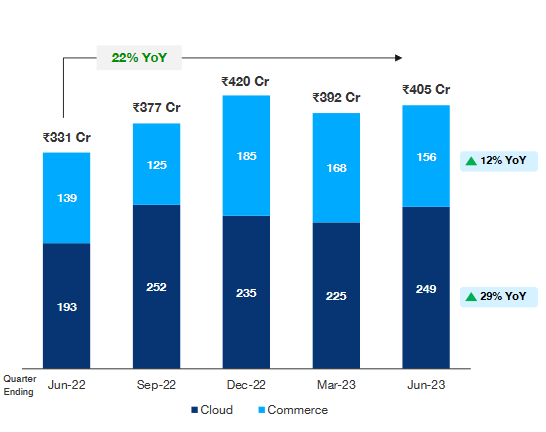

2. Commerce ( earns 5-6% of GMV)

3. Cloud

1.Payments business( customers/ merchants )

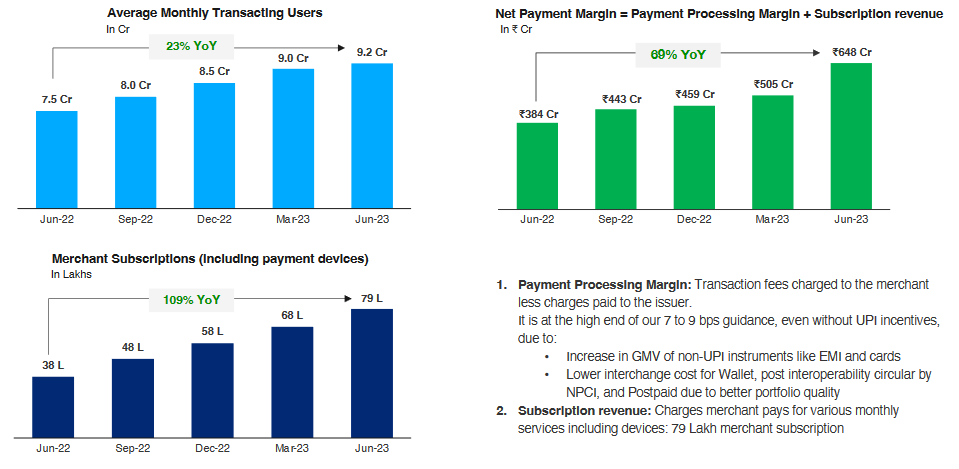

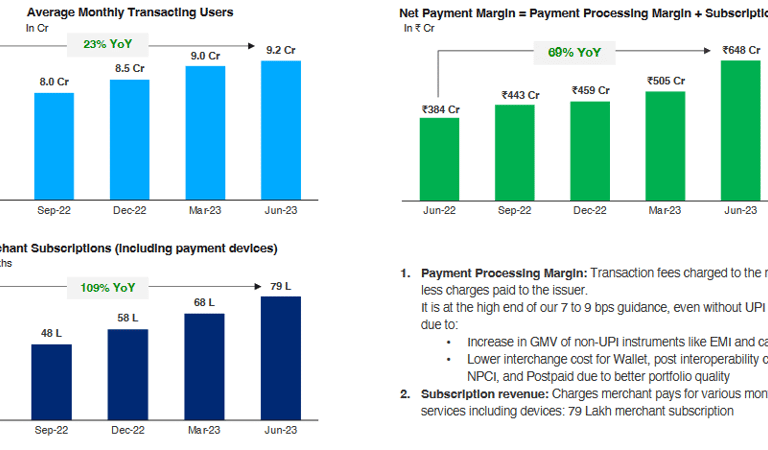

Customer payments - ( total registered customers 9.4 crore) like Utility bill payments, recharges, payment gateway charges

UPI transactions are free as on date, so no scope of monetization in near future . UPI market share of Paytm is 14%

Merchant payments is mostly from soundbox ( all of us must have seen this device in merchant shops which speaks out the payment amount on UPI payment receipt) device subscriptions . They charge Rs 100/ month as rent for the devices.

Total 69 lakhs merchant base (F23) - all of them have this device ( total 1 crore devices in market of all players). Plus they earn on commissions on merchant transactions.

Paytm was the first mover in introducing soundbox in 2020 and implementing them at 100% merchants very fast within a year, before even competitors could understand. Though Paytm introduced it as a Retainer product, but now PhonePe , Bharatpe aggressively offering the same devices at lower cost, PhonePe has already distributed to 20 lakh merchants. So the stickiness for this product is low and switching over may happen as it happens in UPI merchant payments with cashburn all these companies are doing.

Further, PhonePe is settling payments same day vs Paytm doing it next day. It matters a lot for small businesses.

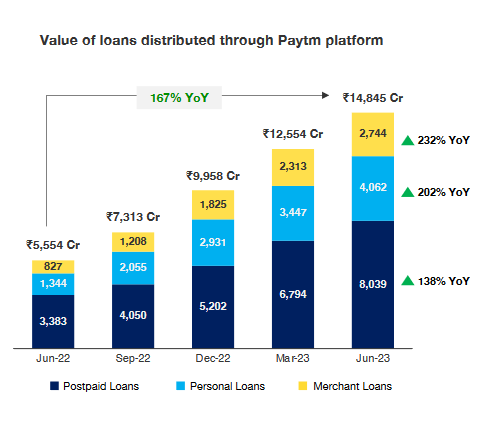

Digital Loans ( tie up with AB capital / Hero fincorp)

Postpaid loans ( BNPL) are given to customers who gets option to convert their purchases to EMIs .

Personal loans like credit card payment, family function, medical expenses are given. Average ticket size ( ATS) of 1.3 lakhs. 40% of personal loans are given to existing postpaid loans customers.

Merchant loans Working capital loans given on basis of cashflows generated on Paytm transactions by merchants , where daily repayments are done.

They are doing loans at breakneck speed . Total loanbook 35000 cr as of F23 which was just 7600 cr in F22.

Paytm earns 3% upfront commission on loans, and 1% of remaining loan value during collections.

2. Commerce ( earns 5-6% of GMV)

Paytm earns 5-6% commissions on transactions in Paytm mall, travel ticketing, movie tickets, events

3. Cloud

Paytm sells co-branded credit card with HDFC Bank and earns distribution revenues upfront and lifetime usage fee. Total activated cards in force 5.9 lakh.

They also earn by providing Ad/ marketing services to different companies which can tailor targeted ads to different segments of 9 crore Paytm users based on their purchasing behaviour data available with Paytm.

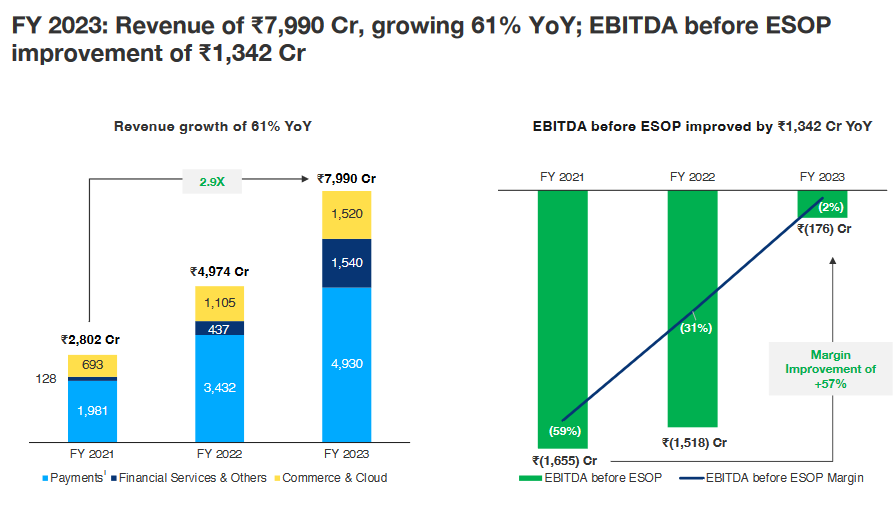

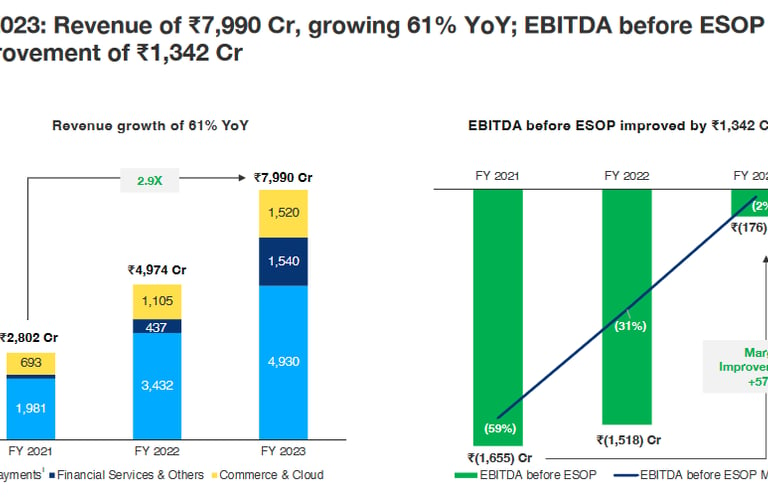

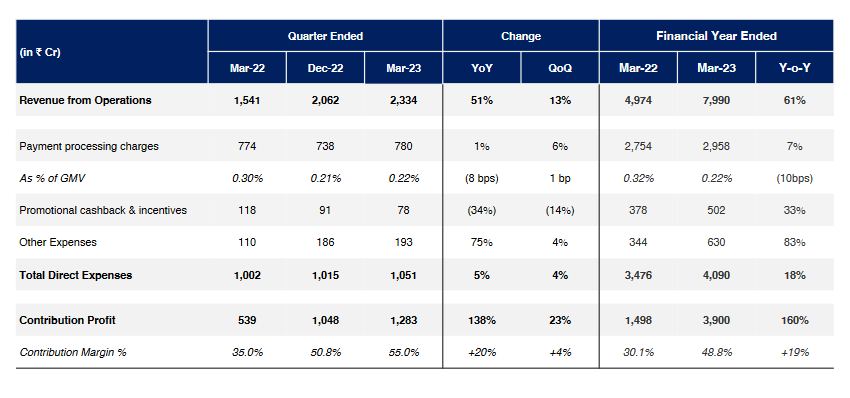

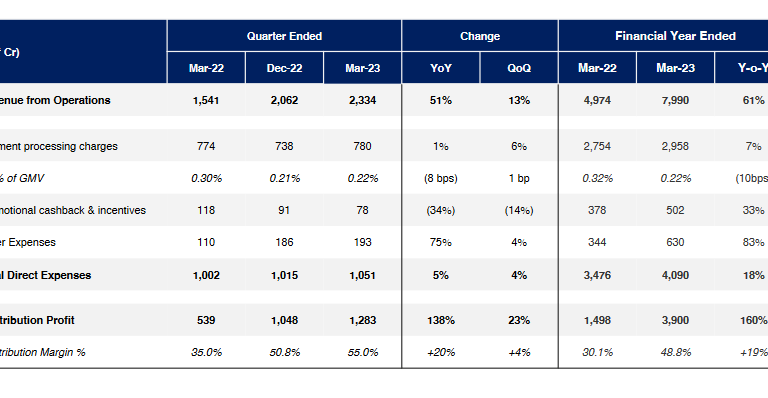

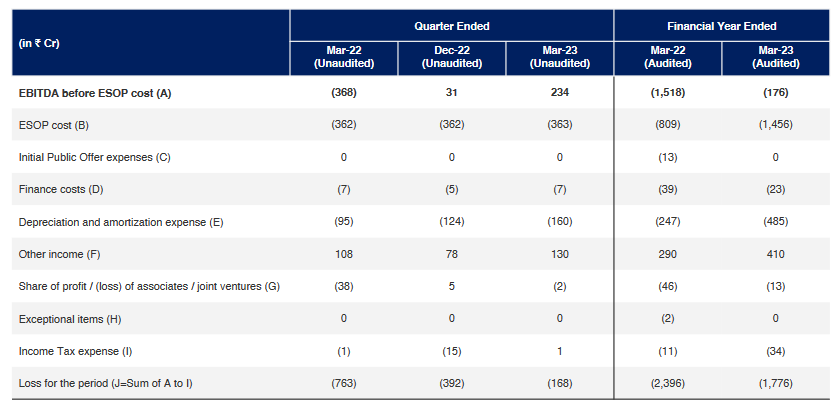

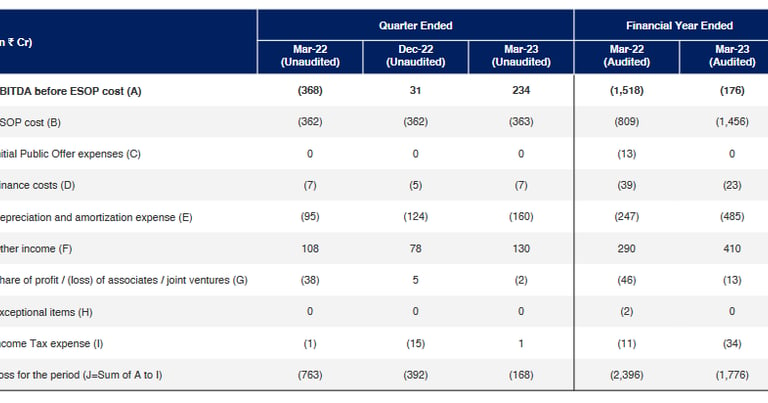

Revenues have become 3X in last 3 years. EBITDA losses before ESOPs (Employee Stock options) have reduced from 1500cr to 176cr.

Payments business revenues grown 40%YOY, Lending business revenue grew 252% Yoy, and commerce / cloud business grew 38% .

For loss making new age tech companies, it becomes important to see the levels of contribution profits / margins, which is revenues - direct costs ( payment processing , promotional cashbacks/ incentives).

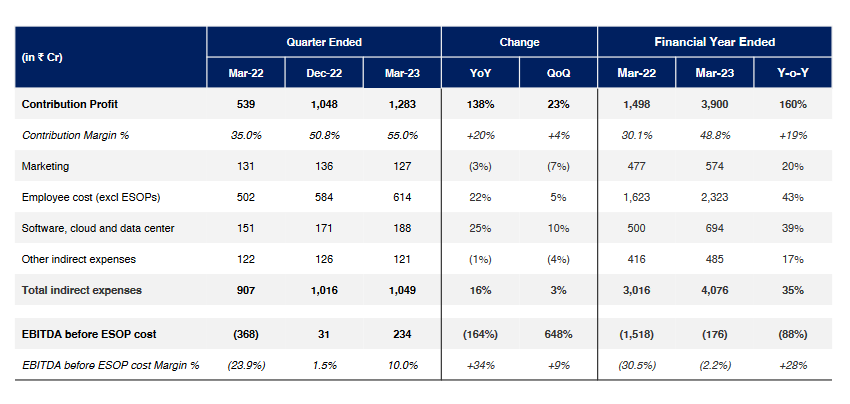

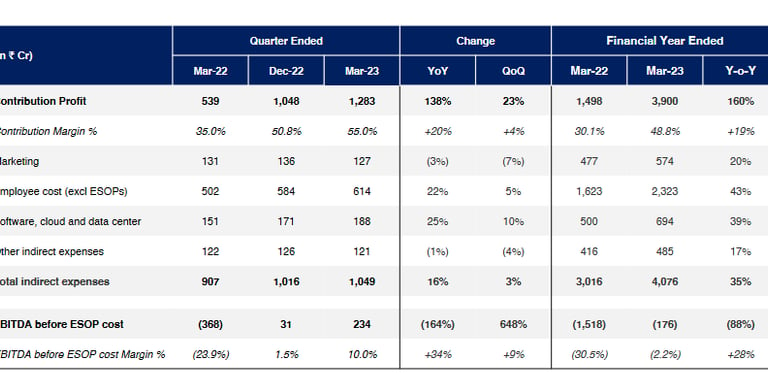

Contribution profits has grown 160% yoy, and contribution margin expanded from 30% to 49%. Note that company has to keep expending 500cr on cashbacks/ incentives.

Total expenses of company is around 8100cr.

If we look at the other expenses, major expense heads are

Employee 2320 cr

Marketing 570 cr

Software/Cloud 700cr

Another major cost head is ESOPs cost 1450cr which drives the net bottomline of the company to 1776cr ( F 22 net loss was 2396cr)

6. Moat

We have heard the term data is the new oil.

Customer data of 9 cr customers and merchant data of 69 lakh merchants is the main moat of Paytm.

Since digital lending is the main focus now, Paytm has access to its daily transactions done in merchants' Paytm app which helps them assess cashflow and process credit based on credit risk analytics, same with customers UPI transaction data, they are able to process consumer loans.

Platform network effects is also a moat.

7.Points to consider

Company has a business model in place , where they are focusing on monetizing 9 cr customer data by providing them loans, focussing on merchants and offering them loans as the primary driver of revenues.

Paytm mall etc are engagement tools to provide the customer a complete ecosystem, and capture more customer behaviour data .

Ad revenues is another byproduct of customer data. They added merchants very fast. One yr back it was 39 lakh, now 68. But UPI leader Phonepe is also offering soundbox at low cost now, so merchant figures may dwindle.

Company has too high ESOPs, unless ESOPs costs reduce, path to profitability is affected.

Paytm has no experience in credit risk analytics , but it is issuing credit at alarming speed. Though they say risk of default is on issuing NBFC, there may be hidden default risks involved. Plus they don't have any on ground collection team to handle any defaults, everything is online.

In credit lending, growing the loanbook fast is not a factor, correct credit underwriting and collections are more important for success.

Plus BNPL loans may be subject to RBI new clause coming in, like some deposit has to be maintained as a fraction of loans issued ( like it happened for Ant financial in China( fintech of Alibaba) ) .

High Chinese ownership ( Alibaba/ Ant Financials) is another risk factor which may see govt axe.

UPI penetration, merchant penetration, digital loans has huge huge potential to grow in coming few years. But how fast Paytm will achieve profitability will be defined by ESOPs, marketing expenses, cash burning that it requires to keep up with Phonepe, Bharatpe and impact of defaults and how they handle defaults.

You may also like the analysis on PB Fintech (Policybazaar)

Other posts you may like

How to avoid companies like Brightcom (BCG) ? Investing red flags

Will Jio Financial disrupt Bajaj Finance business?

Will Vedanta demerger unlock value for retail investors?

Follow us on twitter

#Paytm #fintech #stockanalysis #themoatinvestor #DMoatInvestor

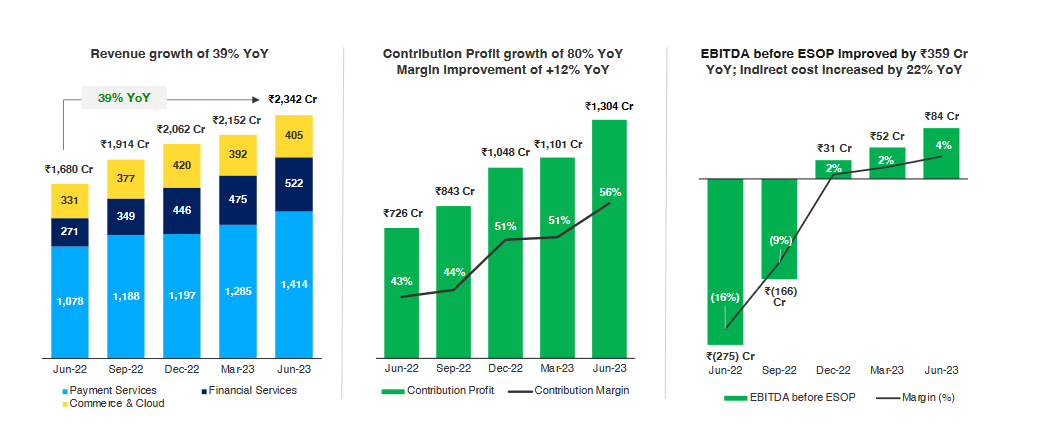

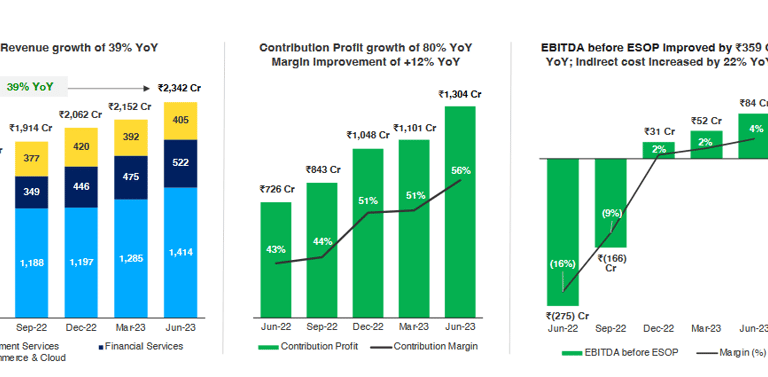

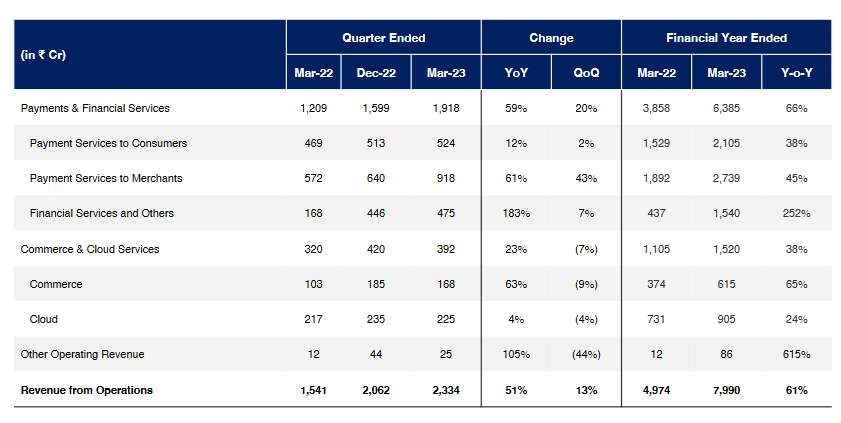

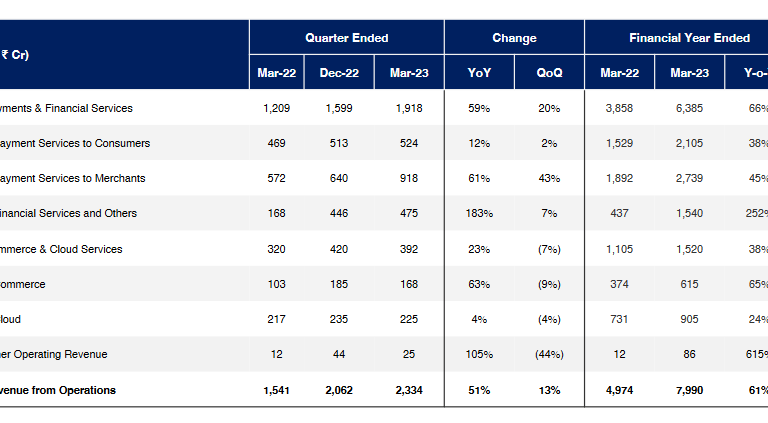

4.Operating metrics

Contribution of commerce and cloud business

Loans business is growing at alarming speed. This is now the main growth lever of the company- digital lending. Paytm has doubled its merchant subscription base in last 1 year.

5. Financials