Will Vedanta demerger unlock value for retail investors?

Sitting on 73500cr debt, out of which 21200cr maturing in FY24/ FY25. S&P Global downgrade to C-. Last 10year dividends paid > profits generated. Debt servicing out of dividends

Brief outlook

Vedanta has announced demerger of its mining conglomerate into 6 individual businesses. Vedanta has 73500cr debt ( Jun '23) on it , with 21200cr debt maturing in FY24 /FY25, which need to be refinanced. With cash in hand depleting, and share price falling fast , 100% of promoter holding being pledged to raise debts, Vedanta is currently living on the edge. Let's find out about the demerger with respect to retail investor's perspective.

There are also myths and perceptions surrounding Vedanta delivering exceptional dividends translating into high long term shareholder returns and wealth creation. Lets get deeper into this.

Piling debt vs Rising Dividends - Do they add up?

All of us know companies distribute part of its profits in the form of dividends to its shareholders. One may be startled to know Vedanta has paid Rs 85000cr dividends in last 10 years (FY14-FY23), whereas 10 years total PAT ( net profits) of the company is Rs 65400cr. So Vedanta has been taking loans to give dividends ( well, not technically). Sounds good for shareholders? Let's find out.

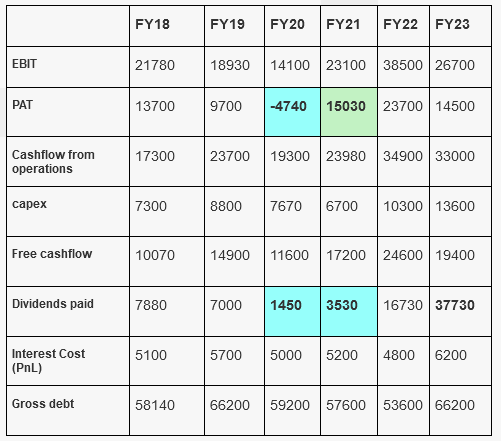

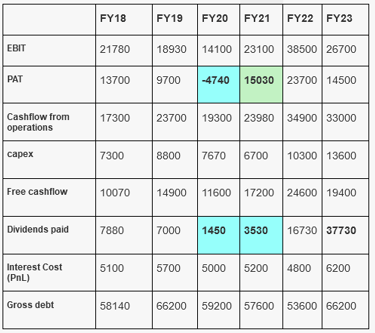

Let's look at the last 6 years picture closely.

Things to note above are

1.Vedanta is generating healthy EBIT ( Earnings before Interest &tax) and Cashflow from operations every year

2. Company is doing > 7000cr capex every year

3. Vedanta is paying > 5000cr/ year interest repayment against debt

4. Despite these, company is not reducing gross debt which remains above 55000cr for most years.

5. Last 6 years total dividends Rs 74320 > 6 years total PAT 71900cr

6. In FY20, company generated losses, despite that paid 1450cr dividends.

7. Dividend payment at all time highest in FY23 at 37730cr

Debt / Equity ratio 2.03 (Mar '23) .

Why do they do that?

The biggest beneficiary of dividends is promoter, as 68.1% (Mar '23) of Vedanta is owned by its London based parent company Vedanta Resources, which too has high debt to the tune of 59860cr ( Mar '23) . In FY 23, Vedanta Resources received Rs 20500cr as dividends from Vedanta Ltd. So this high dividends paid out by Vedanta Ltd is for debt-servicing of parent company Vedanta Resources.

Debt maturity nearing & S&P Global downgrade

As on Jun '23, debt has increased to 73500cr.

Cash equivalents have reduced from 20900cr in Mar '23 to 14300cr in Jun '23.

Further to that, debt maturity of 10900cr in FY24 and 10300cr in FY25 stare at Vedanta, out of which, 8200cr matures in Jan '24. Promoter has pledged 100% of stake to raise debt. Falling share prices add to woes as market value decrease does not help the debt raised on pledge.

Promoter has sold off 4.4% stake ( reduced from 68.1% to 63.7%) in Aug '23 to the tune of Rs 4000cr.

Taking cognizance of the tight liquidity situation, S&P Global has recently downgraded Vedanta's credit rating from BBB to C-,implying costlier debt for Vedanta.

Earlier failed de-listing attempt (2020)

Amidst the covid fall in May 2020 when share prices hit rock bottom, Vedanta announced de-listing at Rs 87/ share to buyout 50% remaining stake. Imagine the plight of long term shareholders holding the stock since 2014 when price used to be 200-240. Book value / share in Mar '23 was 147, implying price announced was 40% discount to even book value. Finally, 90% voting mandate required for de-listing from minority shareholders was not not received, and de-listing attempt failed. But the matter shows the intent towards minority shareholders.

Brief of business & demerged entities

Vedanta operates in exploring, extraction and processing of minerals. Hindustan Zinc is the largest primary zinc producer of India. Vedanta has largest Aluminium installed capacity, with 41% market share. It is also the largest private crude oil producer (Cairn India).

Revenue contribution of different businesses (FY23)

Totals don't add up as figures have been rounded for better readability.

Hindustan Zinc forms major part of the profits.

Vedanta proposes 6 demerged businesses under following heads-

1. Vedanta Ltd ( Hindustan Zinc, Semiconductor, Display, Vedanta Stainless)

2. Vedanta Aluminium ( including 51% stake of BALCO)

3. Oil & Gas (Cairn India)

4. Vedanta Base Metals ( Copper, Zinc)

5. Steel & Ferrous metals

6. Vedanta Power

While focussed businesses of different commodities will attract investors with specific interests, like one investor interested in Oil business may not be interested in other metals, will have now scope to invest in demerged businesses of specific interests. Many investors avoid conglomerate businesses with diversified businesses due to the reason that they may not like all parts of the business for investment, and valuing conglomerate businesses is often a difficult task. Due to these reasons, conglomerate businesses don't often get the actual valuation that they might get if they demerge.

Historical returns to shareholders by Vedanta stock

A company is judged by long term shareholder wealth it creates. We often come across terms like dividend stocks, and Vedanta is known as a dividend stock, known for giving high dividends.

Without considering dividends, Vedanta has given 2% CAGR returns in last 10 years, share price was in 180 range 10 years back ( 2013), current 220.

Vedanta has given Rs 230 dividends in last 10 years, considering that 10 year CAGR returns come as 9.6% ( Nifty 13%). If we consider the 2022 peak of 400, then 13.3% .

These discussions are immaterial considering the sharp spikes in stock prices, acquiring price of normal retail investor in these commodity stocks may vary a lot, as we retail investors usually acquire a stock when it nears its peaks and it is in news everywhere. So someone who would have bought Vedanta in in Jun 2014 at 300 levels, for him CAGR would be 4.6%, less than FD returns.

Yes, its true commodity stocks go through cycles and smart investors who know these commodity cycles can make very good money in short time in these stocks by timing their entries and exits, but we are talking here in terms of retail shareholder's perspective and long term wealth creation by a company which is a hallmark of all good companies.

So Vedanta gives good dividends has not worked well for normal retail investors.

Will demerger unlock value for retail investors?

Usually demerged entities unlock value for shareholders as discussed.

Vedanta maybe doing the demerger out of the emergency arising in terms of nearing debt maturity deadlines , tight liquidity position, falling share price on the face of 100% pledged stake and having to sale stake recently.

Vedanta also announced JV with Foxconn for ambitious semiconductor plan talks of which failed recently after Foxconn announced exit. In the latest release document on demerger, Vedanta announces to go ahead with semiconductors and display investments, but timelines and amount of investments not disclosed. In any case, they have to take more debt to execute the same, which may not be accretive for shareholders in medium term.

But retail investors must consider the past history of Vedanta to decide, as discussed above and summarized below

1. Last 10 year CAGR returns including dividends is on the lower side

2. Failed delisting attempt at offer price of 87 when book value was 147

3. Servicing debt of parent company with dividends seems the primary objective

4. Despite high debt, no debt reduction attempts, though having enough cashflow.

5. Profits of last 10 years Rs 65400, dividends distributed in 10 years Rs 85000 - distributing dividends > net profits is unusual and points at capital allocation priorities of the company.

6. Rs 21200cr debt maturing in FY24, FY25, out of which 8200cr mature in Jan '24 and depleting cash positions.

7. 100% promoter stake pledged

8. S&P Global credit downgrades to C-

9. Dominant position in Zinc, Aluminium, Crude oil production in India & established commodity businesses

Hope these helps you to decide on the Vedanta demerger. Mergers and demergers are a complex process- for large conglomerates, it is more difficult. Valuing them is a task of an expert. If one can do that objectively, perfect for him.

As Warren Buffet says, invest only in businesses you understand.

Purpose is to help take decisions based on available facts and figures rather than getting carried away by news , perceptions and emotions around some stock. When in doubt, always remember the above words of Buffet. Will save you a lot of money and heartburn in the long run.

Consider sharing this to maximum retail investors if you find it useful.

We keep bringing few insightful articles every week.

1. consider subscribing weekly newsletter

2. follow us on twitter for instant updates

3. or may consider to visit our blog every weekend.

Related posts you may enjoy

How to avoid bad companies like Brightcom (BCG)? Investing red flags

Will Jio Financial (JFS) disrupt Bajaj Finance business?

Will Grasim disrupt Paints industry?

Follow us on twitter

#themoatinvestor #dmoatinvestor #Vedanta #demerger #valueunlocking