How to avoid companies like Brightcom (BCG) ? Investing red flags

Contents

Darling of stock market & Media hype - Brightcom/ BCG

SEBI findings of 22nd August '23 against Brightcom

Simple checks that every investor could do

1. Sudden abrupt growth in revenues

2. Standalone vs Consolidate revenues

3. High number of subsidiaries

4. Cashflow from operations (CFO)/ Profit after tax( PAT)

5. Trade receivables / Revenues

6. Promoter holding / Strong hands vs Retail holding

7. Continuously high CWIP wrt Fixed assets

Digging deeper ( March '22 annual report )

1. Repeated firm name change (4 times)

2. Related party transactions 1030cr

3. Contingent liabilities ( previous tax disputes) 230cr

4. Loans given to others 1520cr

5. Indian clients vs Standalone business revenues

6. Sudden jump in promoter holding from 4%to 18%

7. Other liabilities increasing despite huge cash available

Dumping of shares to public ( increasing retail holding)

Darling of stock market & Media hype - Brightcom / BCG

Brightcom used to be darling of stock market and media in 2021. Because in 8 months time, stock rose from Rs 4 to Rs 120, that is 30X or 3000% in 8 months.

Have you heard of any other stock with such returns in such short time?

It became a part of NSE500 and even the prestigious MSCI emerging market index ( benchmark index based on which many FIIs re-balance their emerging market portfolios) !

Instead of being skeptical and being wary , retail investors kept buying the stock. As latest as Apr '23 , even when the stock corrected 92% to Rs 9 from its peak, people started buying again, and it became 2.6X in matter of 2 months (June '23).

Such is the force of GREED ( hope of making quick money) in stock market.

SEBI findings of 22nd August '23 against Brightcom

SEBI had released an investigation report on Brightcom/ BCG on 22nd Aug, '23 . Brightcom/ BCG has raised funds in FY 21 and FY 22 worth Rs 867cr via preferential warrant allotments to 82 people.

So once preferential warrants are issued to investors, allottees ( investors) are supposed to pay that amount decided to Brightcom/ BCG.

SEBI investigated fund flows of 245cr worth of warrants issued, and found that against 245cr, Brightcom/ BCG has received only 52cr in their books of accounts.

SEBI concludes that rest amount has been routed back to the allottees' ( investors) accounts via complex transactions.

Earlier Brightcom/ BCG has reported to SEBI disclosures that money against warrant has been received and they had submitted their bank account statements to support that. SEBI verified those bank account statements with respective banks, who have confirmed that they were fabricated, money was not received in those bank accounts.

Apart from this, SEBI started investigating Brightcom/ BCG since Sep '21. In Apr '23, there were SEBI reports of alleged accounting fraud and further in Jun '23, SEBI fined Rs 40 lakh to Brightcom/ BCG for insider trading.

Simple checks that every investor could do

Checks listed below are something every investor could do to stay away from such companies. Post has been written such that people without any accounting background can absorb most part.

We are sure that accounting experts/ CAs can uncover many more discrepancies in books of Brightcom/ BCG.

1.Sudden abrupt growth in revenues

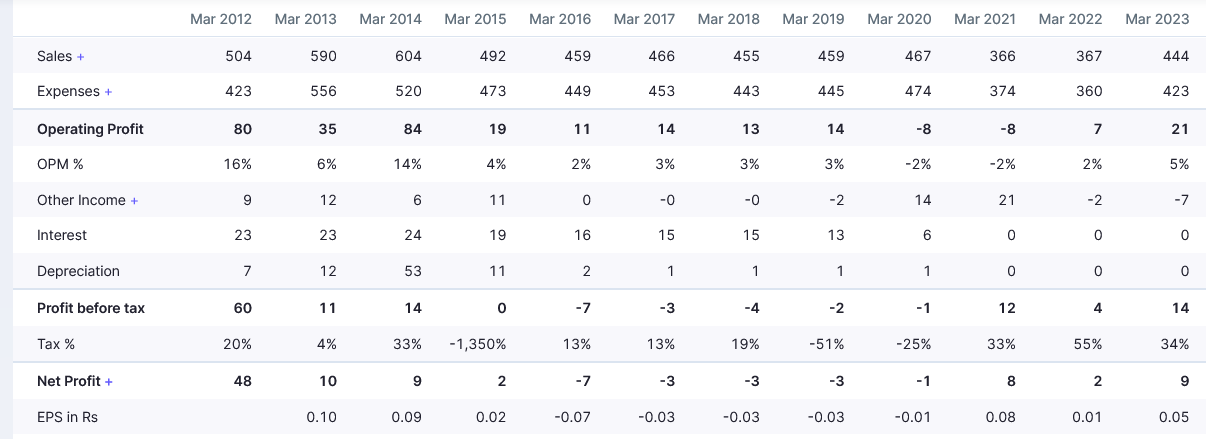

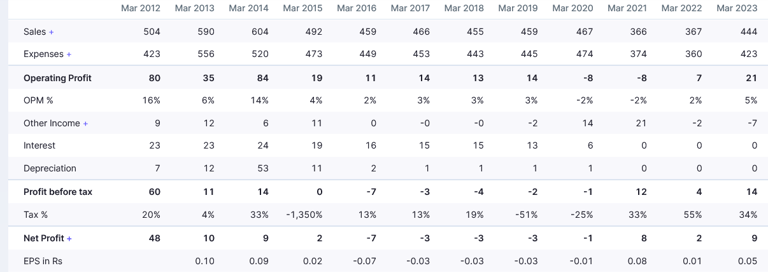

Cashflow from operations ( CFO) /PAT or CFO/ EBITDA ratio is often a good indicator of cash conversion- what amount of profits are actually being converted to cashflows .

CFO/ PAT > 80% is good unless entire industry is such where payments remain stuck for high amount of duration, very high working capital provisions are required sometimes.

Since there may be some years when enough cashflow ( notice first row in the pic) not being generated which is absolutely normal, we look at 5 year CFO/PAT, which is only 56% ( CF0 - 2050cr against PAT 3640cr), way behind the acceptable mark. If we look at peer Affle India, generating CFO/PAT > 80% consistently.

So this is another red flag.

5. Trade receivables/ Revenues

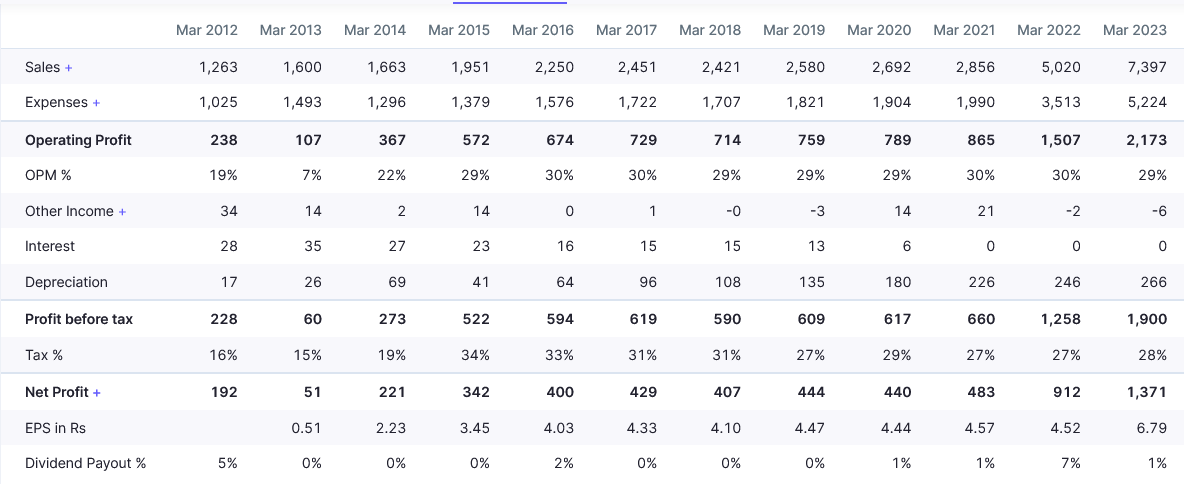

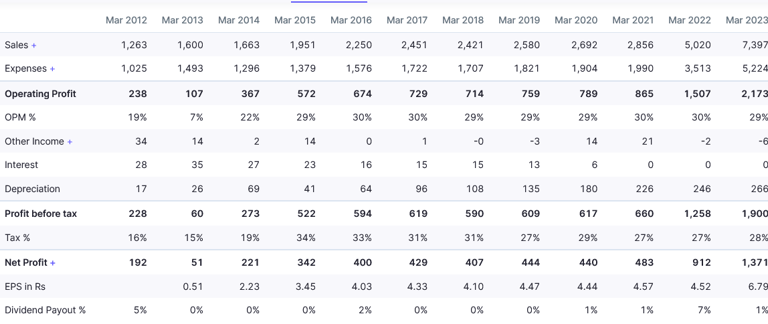

If we see, for 6 years since Mar '16 to Mar '21 , revenues grew at 5% CAGR , suddenly in Mar '22, it jumped 76% . While there might be triggers in some companies

( acquisition of other sizeable company, sudden change in industry, sudden big orders etc) to grow revenues at such high rate in 1 year, but this obviously calls for more scrutiny and skepticism how the business generated such huge growth in 1 year rather than being jubilant over the fact.

2. Standalone vs Consolidate revenues

2 things that is instantly glaring to see are-

Standalone business revenues are only 370cr ( Mar '22) which is only 7% of consolidated revenues. It is very unusual for a company generating such low portion of revenues from standalone company. It's a red flag.

2nd is there is no growth in standalone revenues in Mar '22, entire growth came from subsidiaries. In such cases, it is imperative to look at the subsidiaries in details.

3. High number of subsidiaries

If we check, there are 16 subsidiary companies of Brightcom /BCG across the world in different countries where they operate.

It is always better for retail investors to avoid companies with high number of subsidiaries and complex organization structure.

Because often, required disclosures with respect to the subsidiaries (individual P& L, Balance sheets, details of related party transactions) are absent in companies with high number of subsidiaries. Companies resorting to accounting frauds often take help of high number of subsidiaries and high number of transactions between these subsidiaries( we will see this as you read more) for siphoning money off the accounting books.

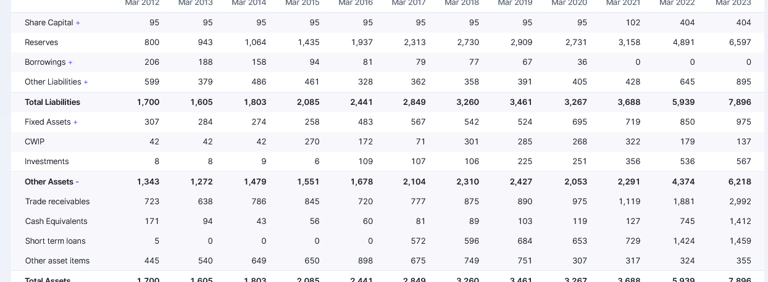

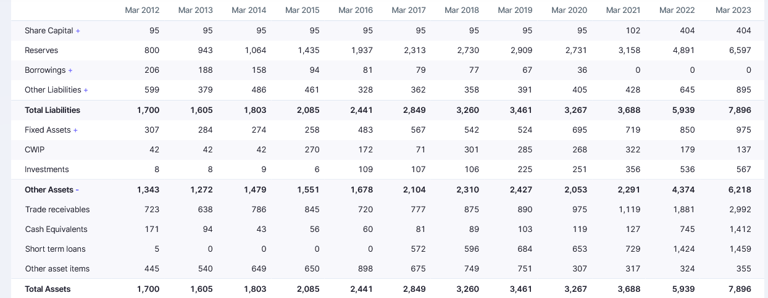

4. Cashflow from operations (CFO)/ Profit after tax( PAT)

Trade receivables are revenues recognized in P & L but payments are yet to be received from customers. Some industries typically B2B businesses have high trade receivables ( 20-30%) , but in case of Brightcom/BCG it is exceptionally high at 37% ( Mar 22 which has further increased to 40% in Mar '23.

If we check for Affle india, it is much lesser.

Constantly high trade receivables is a red flag questioning whether revenue recognition mechanism by the company is too aggressive.

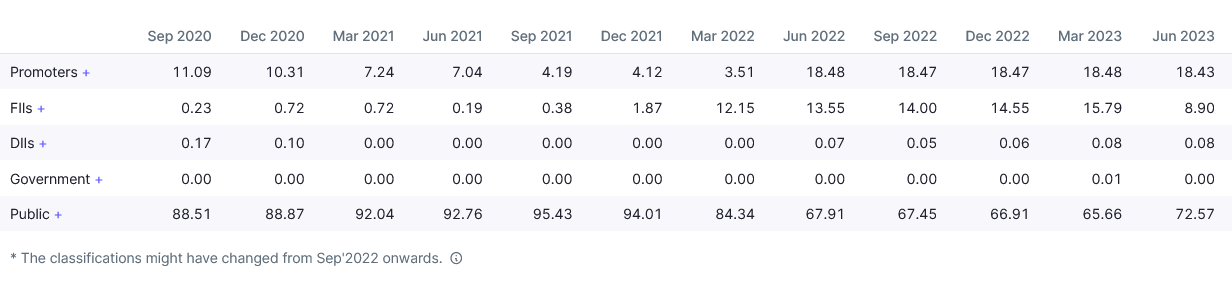

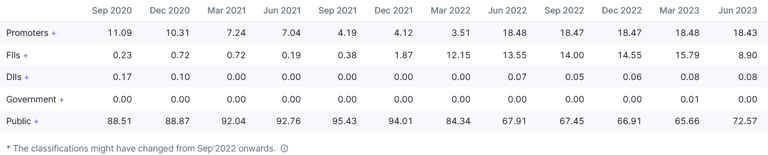

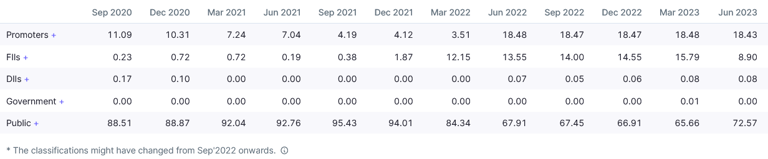

6. Promoter holding/ Strong hands vs Retail holding

Stocks with too low promoter holding or overall strong hands holding and too high retail holding are recipe for disaster, and are candidates for rejection without any further consideration of any other business parameters, however attractive those may be.

In case of Brightcom/ BCG , we find promoter holding was only 4% ( which later increased to 18% - we will discuss more on this as you read on) .

18% promoter holding , 50% retail holding (Dec '21 when stock price was at peak), so effective strong hands holding was 50%.

Stocks with > 30% retail holding are usually subject to more speculation, as retail investors are not informed investors, most of them act on news, media hype and emotions, and not on facts and figures.

Current retail holding ( Jun '23) is 61% ( exceptionally high) even after this huge fall, and even after recent reports of Apr '23 and June '23 by SEBI. From this, you may be able to gauge the retail exuberance and enthusiasm for Brightcom /BCG.

7. Continuously high CWIP wrt Fixed assets

CWIP ( Capital work in progress) is the assets for new projects under development, which are not generating revenues currently. Companies constantly doing capex for future will have high CWIP, but usually that is reflected in increased revenues within next 1-2 years.

In case of Brightcom/ BCG , we see very high CWIP ( as a proportion of fixed assets) from as early as Mar '15 which is a red flag and quite fishy, since these are not reflecting in terms of substantial increase of revenues in subsequent years.

Some of these factors are covered in this earlier article

10 Important factors & ratios to consider as stock filtering criteria

Digging deeper (Mar '22 Annual report)

Investors may not have time to look into annual reports of every company they invest in, but in case there is any serious allegation against the company they are already invested into, by SEBI/bank or any other important body, that calls for delving deeper into the annual reports, based on which he/ she can decide whether to hold or exit.

1. Repeated firm name change ( 5 times)

Repeated firm name change by a company has to looked into seriously, whether the purpose is rebranding, changing the entire direction of business, or due so requirement of merger etc.

Brightcom/ BCG existed as 5 different names since its inception. It started as USA greetings in 1996, then changed to Ybrant Technology in 2000, then changed to Ybrant Digital in 2004, then changed to Lycos Internet in 2014, and finally adopted the name Brightcom in 2018.

One can correlate this with another point discussed later.

Companies don't usually change names so much as all the efforts and money put in for establishing brand equity goes for a toss.

2. Related party transactions ( 1030cr)

If we check annual report ( page 108),

Unsecured loans FROM related party 109cr

Investment in subsidiary ( 13 nos) 673cr

Unsecured loans TO related party 248cr

(Ybrant, LGSL, LIL, Yreach)

Such high amount of related party transactions calls for further disclosures which are not available in balance sheet. Unsecured loans in shady companies to related parties may go bad in future and increases the possibility accounting frauds.

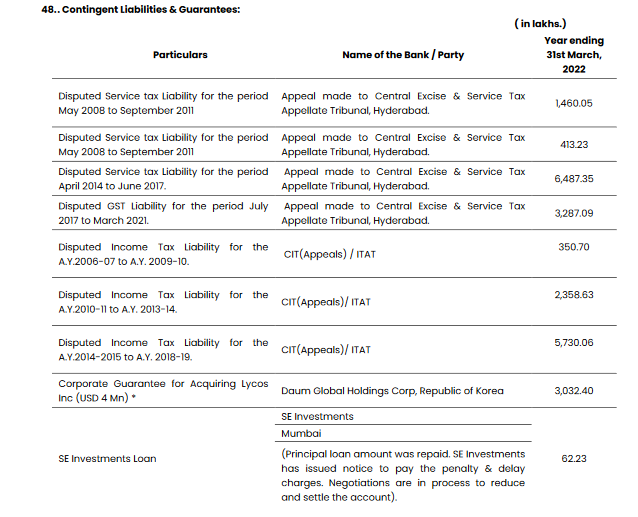

3. Contingent liabilities ( previous tax disputes 230cr )

Contingent liabilities ( page 116) constituting previous tax disputes with Income tax dept/ GST dept since 2011 worth 230cr are unsettled does not show a good picture of the company and another red flag & indication of possibility of fraud. Some firms change names repeatedly change names just to evade taxes, can't say whether Brightcom/ BCG is one of those.

4. Loans given to others 1520 cr

In the consolidated balance sheet section ( page 127),long term loans given is 1420cr and short term loans given in 100cr, totaling loans given to others at 1520cr, with no further disclosures about to whom such high amounts have been given.

This, again is another red flag and opens another suspected scope of accounting fraud.

5. Indian clients vs Standalone business revenues

In the investor presentations, Brightcom/ BCG mentions domestic clients as Maruti Suzuki, ITC, ICICI Bank, Airtel, LIC . But the meager numbers of standalone business revenues are not able to justify that. Read in some news some such prominent Indian firms, when contacted, denied being clients of Brightcom, didn't verify the source though.

6. Sudden jump in promoter holding from 4% to 18%

If you remember, Brightcom/ BCG issued warrants worth 876cr from July '21 to Feb '22. Among others, warrants were issued to these 4 following entities

Aradhana Commosole 5.16%

Sarita Commosoles 5.16%

Kalpana Commosoles 2.58%

Shalini Sales 2.06%

Later, promoter of Brightcom, Suresh Reddy became partner in these 4 firms, and acquired them under Brightcom group, so 15% owned by these 4 firms were added to promoter stake taking the total promoter stake to 18.5% in Jun '22 Quarter ( which was 3.5% in Mar '22 Quarter)

This also does not clearly sound good.

7. Other liabilities increasing despite huge cash available

Other liabilities section in Mar '22 increased to 645cr, despite cash equivalent of 745 cr already available on balance sheet. Its a pertinent question that why the company is increasing other liabilities despite sitting on huge cash.

Dumping of shares to public ( increasing retail holding)

Here Dec '21 quarter holdings have been taken as Dec '21 was the time when stock price peaked. If we observe, despite stock correcting 92% from peak, we find retail participation in the stock increasing , especially retail people who invested less than 2 lakhs in Brightcom/ BCG , constituted 20% in Dec '21, owns now 33% of the stock.

Remember, we talked about high retail exuberance in such penny stocks, so called multibaggers.

And the holdings of body corporates reduced from 32% to 17% ( 2%+ 15% of the 4 entities who were earlier body corporates and inducted as promoter). This is what usually happens in all such hype stocks, retail people get stuck and strong hands exit selling their holdings to retail people.

So eventually retailers are the biggest losers in this game of fraud.

As you can see, such will be the temptation to buy such stocks from the continuous mainstream media hype, it becomes difficult for retail investors to ignore these unless we have a written investing framework in place.

To make decision-making further difficult for retail investors, renowned investor Shankar Sharma is also invested in this stock ( one of the allottees of preferential warrants). So taking buying decision based on whether star investors also invested in some stock does not help, because after all the risk appetite, portfolio size, % of portfolio for one stock, horizon to hold(1 year or 20 years), their buying price- all these will not match with us.

Another point, if we observe the charts, stock continuously moved in upper circuit during its upmove and then during the fall continuous lower circuits, indicating operator's play or too much greed/ fear at play .

Such stocks are better avoided just by observing this on charts.

So eventually retailers are the biggest losers in this game of fraud.

Better to have an investing framework in place. That is the way we avoid these traps.

Request to share this article to maximum investors you know so that retail investors don't get trapped in these bad stocks.

More on

Insights

12 Things to consider before starting stock investing

IPO analysis for listing gain

May follow us on twitter

Disclaimer : Everything written in the article and all other posts has been done purely with the analyzing a stock only with motive of investor education and there is no intention to defame Brightcom or any other company whatsoever.

#themoatinvestor #dmoatinvestor #fraud #brightcom #bcg