Utkarsh Small Finance Bank Business Analysis

Contents

History of company

Industry overview

Geographical presence

Operating metrics

Financials

IPO Size & utilization of funds

Moat

Points to consider

Valuation

1.History

Utkarsh Small Finance Bank founded by Govind Singh started its journey as an MFI ( Microfinance Institution) in 2010 in Varanasi with 4 branches and 8000 clients, expanded to Bihar, Uttarakhand ,UP and MP in next 3 years. They started banking operations in 2017 after RBI granted them small finance bank license. Utkarsh SFB is focussed on unsecured small ticket individual / group loans with Bihar and UP as their primary territory.

2.Industry overview

Small finance bank scenario is dominated by 3 prominent players, AU Small Finance Bank, Equitas Small Finance Bank and Ujjivan Small Finance Bank, whereas AU has shifted itself from unsecured loans portfolio that is usually done by small finance banks and microfinance institutions.

Utkarsh' s loan book of 13000cr is almost half the size of its bigger listed peers Ujjivan/ Equitas SFB.

Rural India has immense scope in terms of banking sector. 47% of India's GDP comes from rural India, but rural contributes only 8% of total credit sector. With the series of banking reforms like Jan Dhan Accounts, launch of UPI, increasing smartphone penetration and cheaper mobile internet, high speed broadband connectivity to rural- all these combined is going to increase penetration of credit to rural India. Since large and mid sized traditional banks do not have that much presence amongst the currently unbanked section of the society in rural india, microfinance institutions and small finance banks ( all erstwhile MFI) are best placed to capitalize on this growth story.

Microfinance sector had been hit from loan defaults due to covid, but most players have recovered from . Usually, despite doing unsecured loans and lending to the unbanked section of the society, good microfinance institutions or SFBs (small finance banks) maintain NPA (non-performing assets) levels comparable to the best traditional banks catering to the upper, middle class or corporates.

3.Geographical presence

56% of loanbook concentrated in UP and Bihar. Since they started in 2010 as MFI and UP/ Bihar has been their base so they know the territory well, which is very tough market in terms of credit recovery. Despite that, they have industry best NNPA of 0.4%. ( covid years 1.3% , 2.3% ). Also, Bihar and UP are still the most underpenetrated credit markets of India, leaving a lot of scope of growth in those markets.

Total 830 banking outlets ( includes branches) , out of which 44% are in Metro/ Tier I cities.

But there is a geographical concentration risk in terms of natural calamities affecting UP and Bihar, NPA levels can increase.

Operational metrics

Out of its total business, unsecured microbanking loans ( small ticket group loans and individual loans) is 66% of the total loanbook, they are strategically reducing unsecured loanbook. ( used to be 82% 2 years back.)

Utkarsh has grown its loan book by 3 times in 4 yrs, faster than its peers ( since it has smaller base ). Growth is coming from the other sections- affordable housing, retail, wholesale, tractor and commercial vehicle loans. The depend on DSAs for sourcing loans. Loan book grew even during covid .Deposits has grown at same pace.

CASA ratio 22% is less, since raising CASA is challenge for microloan majority banks owing to them catering bottom section of society ( majority book microfinance) who have meagre amounts in savings accounts

NIM (Net Interest Margin) 9.6%

cost of funds 7% ( peers 5.5- 6%) are comparable to peers.

PCR ( Provision coverage ratio) is high.

Capital adequacy > 20% , ROA ( Return on Assets) 2.1% , ROE (Return on Equity) 22%, credit spread 13% , all are good as per standards.

Credit lending rates are lower than peers.

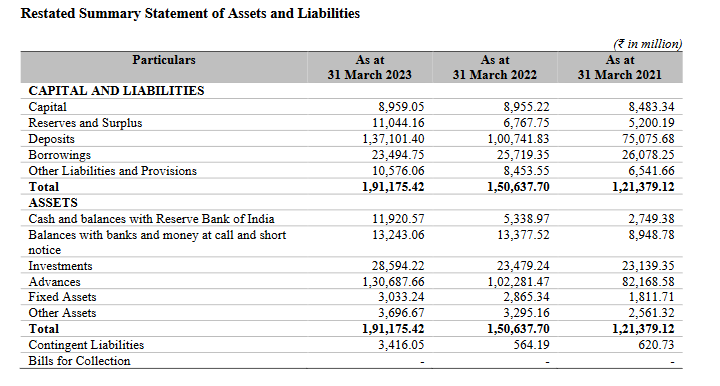

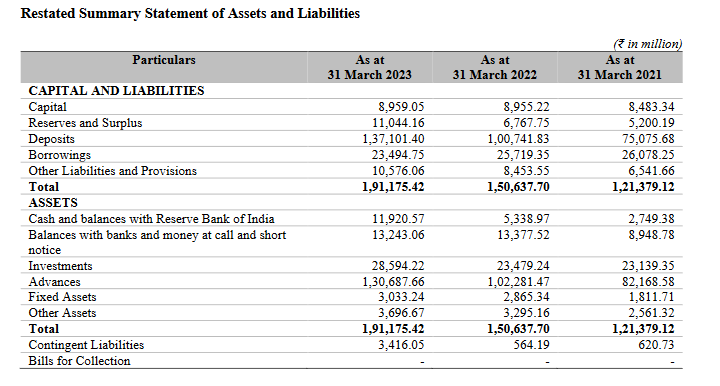

Financials

Net Profits became 4 times from F 21 as loanbook grew by 65% as well as NIM expanded and cost of funds reduced since F 21. Going forward, NIM would stabilize ( expanded from 8.2% to 9.6% since F 21 owing to rising interest rates) as interest rates are going to reduce.

6.Moat

Expertise and deep rural presence in UP and Bihar ( grossly underpenetrated in terms of credit ) is their moat as other microfinance institutions keep their exposure low to these states.

Additionally, as SFB, better placed to cater credit to lower strata of the society vs traditional banking channel.

Points to consider

Overexposure to 2 states can bring stress to loanbook if natural calamities like floods affect these states.

Very fast growth ( > 30% ) of loanbook was possible as it was < 10000cr. With loanbook crossed Rs 13000cr now, growth rate may taper as was seen in other peers.

Valuation

Listing Valuation wise cheap at P/B ratio ( Price/ Book) of 1.1 whereas other peers trade at 2.5 .

#utkarshsfbipo #themoatinvestor #DMoatInvestor #stockanalysis