Mamaearth Business Analysis

BPC Categories

Hair Care 27%

Bath /Body 23%

Face care 18%

Oral Care 12%

Make up 10%

Fragrance 6%

Wellness 4%

Most of the top categories are expected to grow at double digits.Online penetration is maximum in makeup 31% and face care 25%

FMCG giants with significant presence in BPC category are are Hindustan Unilever, Marico, Godrej, Patanjali, Proctor & Gamble, Dabur, Emami, Johnson & Johnson. Nykaa is also a prominent name in online BPC.

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Moat

Valuation

Business

Mamaearth, promoted by Honasa Consumer, launched in 2017 by Varun Alagh (CEO) and Ghazal Alagh. Most popular brand under Honasa is Mamaearth. Products focus on natural, toxin free beauty products. Other five newer brands are The Derma Co., Aqualogica, Ayuga, BBlunt and Dr. Sheth’s. Honasa product range caters baby care, face care, body care, hair care, color cosmetics and fragrances.

Strategy

Products are produced through contract manufacturing- they have tie-ups with 37 contract manufacturers. Mamaearth does consumer centric product innovation, with in-house social listening and tracking platform.

Mamaearth has a strategy of digital-first omnichannel- primary sales channel being marketplaces like Amazon /Flipkart. Their target segment is millennials who are increasingly getting conscious about hair care, make-up and believes in brands with purpose behind it.

Like Nykaa, Mamaearth also significant uses influencer marketing. In FY23, they worked with 4025 influencers. Mamaearth works through content creators including bloggers. Being sponsor at Big Boss, and Ghazal Alagh a judge at Shark Tank gave a lot of visibility to Mamaearth. They had roped in Shilpa Shetty as ambassador, who has picked up stake in the company and selling stake in OFS.

Brands

1. Mamaearth

Toxin-free beauty products made with natural ingredients, with products across baby care, hair care, face care, body care, color cosmetics, and fragrances.

2.The Derma Co

Acquired in 2020- this skin and hair brand offers a range of products that help resolve diverse concerns like active acne, acne marks, pigmentation, hair loss, dandruff, etc.

3. Aqualogica

Launched in November 2021, Aqualogica is specialized skin care brand that leverages the science of hydration to introduce products suited to Indian skin-types.

4. BBlunt

Acquired in March 2022, BBlunt is chain of hair& styling salons in Bangalore, Kolkata, Delhi

5.Dr Sheth-

Acquired stake in Apr 2022,DR Sheth works in bio-actives based skincare developed by three generations of skin specialists

Offline Channel

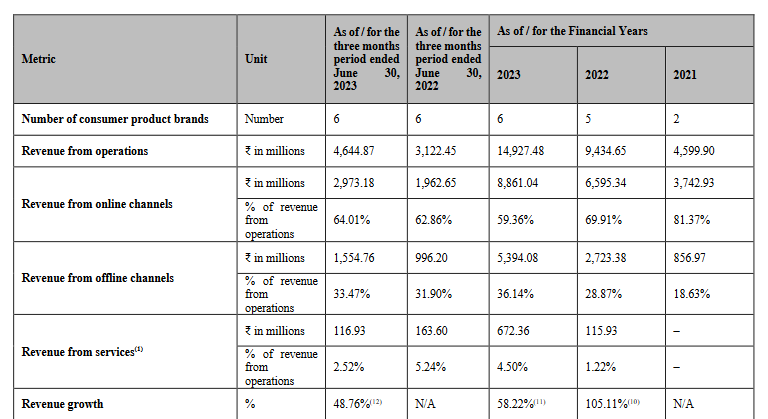

While Mamaearth is a digital first brand ,59% of sales being done through online channel, they have has 85 EBOs (exclusive brand outlets). Apart from that, 541 distrbutors/ stockist/ sub-stockist. A total of 1269 beauty advisors work to promote their products in these channels. Their current reach is around 154447 retail outlets. 13 warehouses across India cater to their inventory.

Future plans

Mamaearth places itself as a House of Brands, so it will keep launching own / acquiring new brands that supplements their core brands in BPC. It will keep adding EBOs to improve brand presence - no guidance with respect to number of EBOs.

Mamaearth had a market share ( GMV) of 5.4% of the online BPC market ( DTC and e-commerce) in CY 2022, 1.5% market share of total BPC market in CY22.

Industry overview

Beauty and Personal Care in India is Rs 1,64,000cr market ( 2022), and expected to grow at 11% for next 5 years. The online BPC market is Rs 24.600cr. 42% of BPC industry is organized, projected to increase to 65% by 2027. As per reports, BPC is among one of the private consumption items which will have faster online adoption - from 16% penetration as of 2022 to 34% by 2027. Drivers of growth for online BPC are millenials/ Gen Z, and increased participation of women in the labour force.

Offline ( Unorg) 57%

Offline (Org)27%

Online 16%

The online marketplaces channel is expected to grow at around 25% , DTC ( Direct- to consumer) is expected to grow at 45%

Online penetration (BPC)

USA 20-25%

China 35-40%

India 16%

Operating metrics

Revenue mix

Total sales FY 23 1490cr, out of which

Mamaearth 1170cr ( Online/ Offline 650cr/ 510cr)

Other 5 brands 253cr ( Online/ Offline 23cr/250cr )

Ad expenses for Mamaearth is 370cr ( 31%of sales)

Ad expenses for other brands is 160cr ( 62% of sales) which is way higher.

Total ad expenses Rs 570cr ( 35% of revenues)

To put in perspective, Nykaa BPC spends 12% of revenues as ad spends, Hindustan Unilever 9%, Marico 12%

Revenue channels- Online/ Offline

Online 59% ( 81% in FY21)

Offline 36%

Services 4.5%

Marketplaces ( Amazon/Flipkart) forms 34% of total sales, DTC 25%.

Commisions to market places stand at 34%, sharp increase from 28% in FY22

New SKUs launched in FY23 forms 57% of revenues

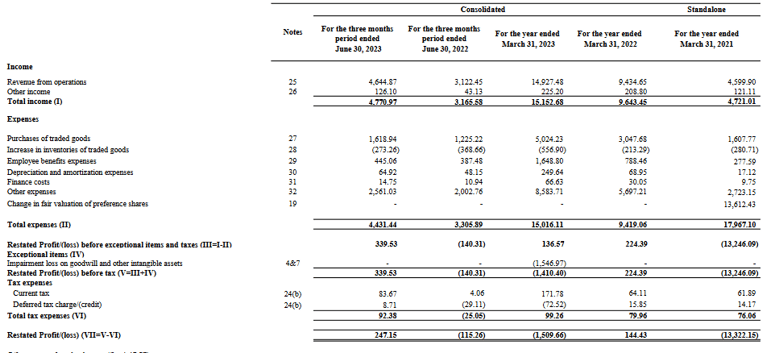

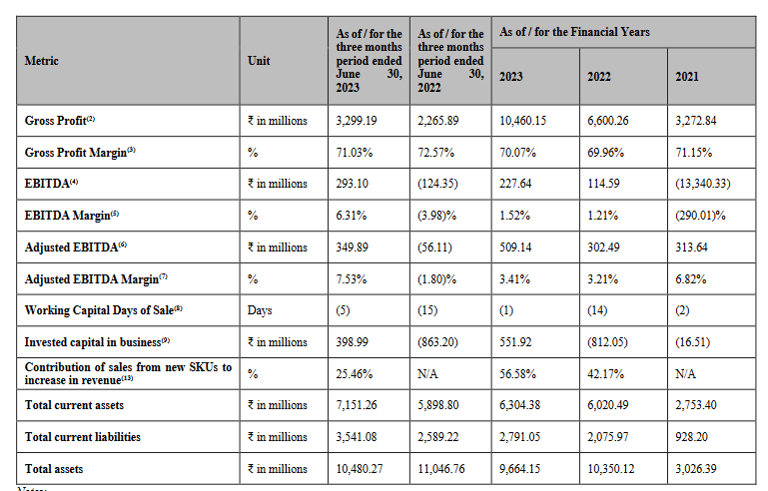

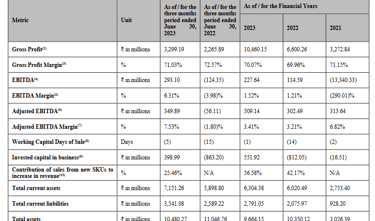

Financials

Annual revenues of Mamaearth is 1490cr. PAT -150cr ( loss)

Revenues CAGR of 80% in last 2 years ( FY21 revenues Rs 460cr)

Gross margins of 70%( Nykaa BPC 44%, HUL(cons.) 50%)

EBITDA margin of 1.6% ( HUL 26%)

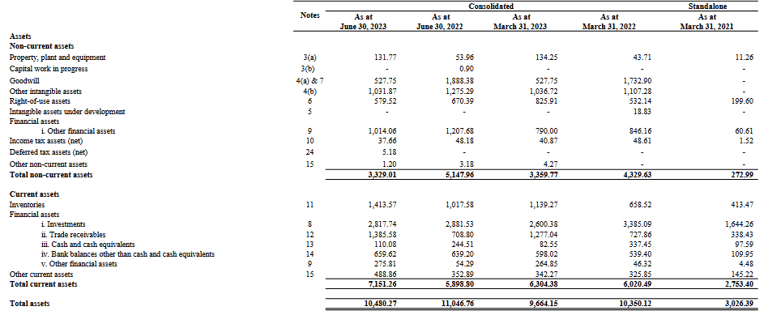

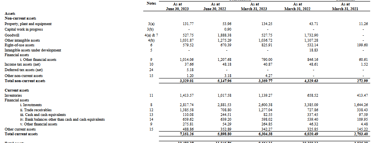

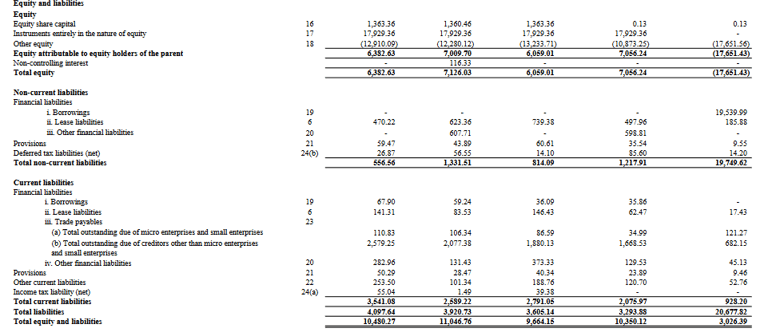

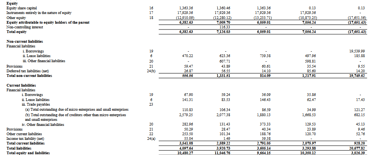

Balance sheet ( amount above in Rs millions)

Borrowings ( including lease liabilities) at 77 cr ( Debt/ Equity 0.13)

Cashflow from operations -50cr ( negative)

Cash & cash equivalents 4.6cr

Trade receivables at 130cr(low)

Inventory 113cr

Points to consider

While Mamaearth has positioned itself as digital first brand, dependence of e-commerce marketplaces (34% of sales) can affect margins in case marketplace decides to increase commissions.

Though placing themselves as digital first brand, metrics of their website ( customer visits/ average spends/ user) are yet to to disclosed. Neither any plans to increase direct sales through their own site sales disclosed yet.

FMCG being a distribution led model, strong offline presence is important for a brand to attain significant scale and sustain against established giants in the long run.

Bulk of Sales comes from Mamaearth brand ( 79%),ad spends 31% of sales for Mamaearth. But ad spends on rest 5 brands is 162cr ( 62% of sales), with sales of 260cr. And still they mentioned they will keep adding brands, acquiring new brands, instead of achieving scale in these brands. Points to capital allocation priorities of company.

New SKUs launched in FY23 contributed 57% of sales- which puts a question on the traction of earlier vintage SKUs amongst customer mindspace. If vintage products are not generating repeat sales, leads to a cause of concern.

Giants like Marico also entering digital first space through acquisitions, own brands- so competition from established players has to be considered.

Fresh issue being only 365cr ( ad spend of FY23 was 530cr, cash balance is 4cr), will not serve any significant purpose for growth of the company.

Valuation

Mamaearth is valued at Price/ Sales of 7 . Nykaa trades at similar valuation of P/S of 8 ( PAT of 20cr), though Nykaa has achieved a scale of 4000cr in BPC, and has significant traction in its own website and much deeper content marketing/ influencer marketing presence.

Follow us on twitter

You may be interested in

Paytm Business Analysis

Will Jio Financial disrupt Bajaj Finance

Will Vedanta demerger unlock value for retail investor

How to avoid companies like Brightcom/ BCG ? Investing red flag

#themoatinvestor #dmoatinvestor #mamaearthipo #listinggain