IRM Energy IPO Analysis

Natural gas forms 70-80% of the cost for urea production. Ammonia is produced from natural gas.

Demand drivers in CGD

1. expanding geographical coverage

2. improving cost competitiveness of gas

3. Assured domestic gas supply

4. Regulatory restrictions

5. Growing awareness of cleaner fuel are expected to aid in fuel conversion in industrial segment

Out of total 34 MMSCMD CGD demand,

CNG demand 19

domestic PNG 3

industrial & commercial PNG 12

The CGD market comprises of 10-15 players. Top five players hold 136 GAs ( 46%) of the total 295 GAs allotted. Adani Total Gas is the largest standalone CGD player ( presence in 33 GAs), IOCL ( presence in 28 GAs).

India’s total proven reserves of natural gas estimated at 1,139 billion cubic meters (FY22), with 53% located in offshore gas fields.LNG imports stand at 74 MMSCMD which shot up to 93 two years back. Imports projected to grow at 19-20% CAGR, with share of LNG imports in total natural gas demand to increase from current 44% to 56% in FY30.

Contents

IPO Size/ Promoter holding/ Market cap

Purpose of IPO

Business

Industry overview

Operating metrics

Financials

Points to consider

Moat

Valuation

IPO size /Promoter holding/ Market cap

Total offer ~ 545cr

Fresh issue 545cr

QIB- 50%

NII 15%

Retail 35%

Post listing promoter group holding 50%

Price band- 480-505

Market cap post listing ~ 2070 cr

Purpose of IPO

Debt repayment 135cr

Capex (Trichi/ Namakkal) 307cr

Business

IRM Energy,promoted by Cadilla Pharmaceuticals , started in 2016, is engaged in natural gas( CNG & PNG) distribution system including setting up network of pipelines and CNG stations ,with operations at Banaskantha (Gujarat)(mainly CNG), Fatehgarh Sahib (Punjab)(mainly PNG), Diu & Gir Somnath (UT of Daman and Diu) (mainly CNG), and Namakkal & Tiruchirappalli (Tamil Nadu)(awarded 2022). They operate through network of 61 CNG stations and 238 CNG dispensing points.

Customers

They cater to industrial, commercial, domestic and automobile customers through CNG and PNG( piped natural gas).

CNG is used as auto-fuel.

CNG customers include operators of taxis, auto-rickshaws, and private cars, buses, LCV HCV.

CNG Network types

CNG filling stations classified as ( Total 66 stations)

COCO Stations - owned and operated by the Company

DODO Stations - owned and operated by the dealers

OMC Stations - owned and operated by oil marketing companies

Number of stations ( FY23)

COCO -2 (2%)

DODO- 36 ( 73%)

OMC -28

Opening COCO/ DODO means more savings wrt OMC stations , plus they can have their own branding in COCO/DODO.

PNG customers are-

1. industrial PNG- MSME & large industries

2. commercial PNG - hotels, restaurants, bakeries, hostels

3. domestic PNG - cooking gas customers ( households)

Cost reduction

IRM Energy has strategically acquired GAs with connectivity to cross-country natural gas pipelines within the GA boundary, which reduces the cost of transportation

IRM Energy operates under mid to long-term gas sale and purchase agreements with gas suppliers such as GAIL, RIL helps in cost savings. They meet their short term requirements from Indian Gas Exchange.

Company has been granted network exclusivity rights of 25 years for infrastructure creation for all our GAs.

Tech Enablers

They have implemented RFID writing, detection, for identifying hydrotesting due date of CNG cylinders in order to prevent accidents.

They have developed a web-app for capturing geo-tagged points and gas assets.

For marketing, they conduct meetings with CNG kit retrofitters,provide them free CNG and discount on CNG kit fitting to encourage them to set up more CNG kit retrofitting centers, collaborates with OEMs to conduct promotional campaigns for increasing sales of new CNG vehicles.

Future plans

For the PNG domestic segment, IRM Energy will install pre-paid meters -impact will be cost savings- marketing cost of billing /collection, reduce risk of default, improve cash flow.

For the PNG commercial segment, they will install Automated Meter Reading system for monitoring consumption pattern , reduce billing efforts.

For the PNG industrial segment, already installed AMR system for all customers.

They target to add 24,000 PNG domestic connections, 62 PNG commercial connections, 10 PNG industrial connections, 63 CNG retail outlets in 3 years. Main competitors are Adani Total Gas, Indraprastha Gas, Mahanagar Gas, Gujarat Gas. Adani Total Gas is the largest standalone CGD player ( presence in 33 GAs),

Industry overview

Natural gas demand is 164 MMSCMD in FY23( domestic production 92, LNG imports 72), which has not increased much since last 7 years.The fertilizer (33%), CGD and power sectors contributes 67% of the total gas consumption. CRISIL expects demand for natural gas to increase at 11-12%CAGR till 2030.

Sector wise demand FY23

Points to consider

Around 45% of natural gas requirements of India is sourced from imports. Sharp fluctuations in natural gas prices ( owing to geopolitical supply disruption caused at producer countries) can severely dent the margins of gas distribution players like IRM Energy, similar to what happened in FY23.

Govt push to shift to cleaner fuels coupled with intiatives of companies to CNG conversion will aid usage of CNG in commercial vehicles. But cost competitiveness of CNG as auto-fuel as private cars ( assuming mostly sedans are sold) are not very significant for most users ( 1000km/ month usage) who user cars occasionally on weekends.

CGD sector is seeing huge investments of 1.2 lakh crores in coming years owing to increased urbanization and further improvement in penetration. Adani Total Gas alone has announced Rs 20000cr investment by 2030 in CGD. Further investments of these companies are in EV charging stations, biofuels.

Though other bigger peers are diversifying in bio fuels, waste management, EV charging stations- one has to look into closely whether bio fuels, waste management investment at this stage when company is running on debt and still small in size compared to peers its core business makes sense or not.

EV charging stations can be a natural value addition at CNG filling stations.

Valuation

IRM Enegy is valued at P/E of 33, whereas comparable peer Gujarat Gas at 21, Mahanagar Gas at 11, Indraprastha at 20, Adani Total Gas at 117

Follow us on twitter

You may be interested in

Manoj Vaibhav Gems IPO Analysis

Will Jio Financial disrupt Bajaj Finance

Will Vedanta demerger unlock value for retail investor

How to avoid companies like Brightcom/ BCG ? Investing red flag

#themoatinvestor #dmoatinvestor #irmenergyipo #listinggain

Operating metrics

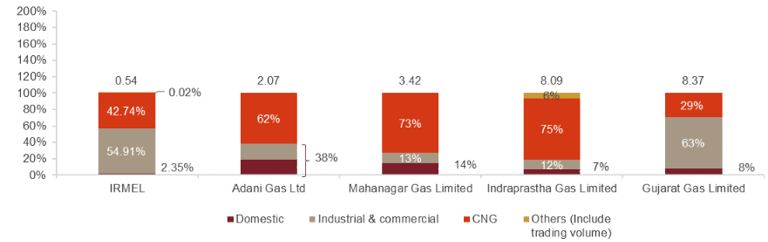

Revenue mix

PNG 57% ( was 24% in FY21)

CNG 42%

CNG mix is quite higher ( >60%) in case of competitors Adani, Indraprastha, Mahanagar.

Revenue mix- PNG ( based on customer type)/ No of customers

Industrial 54% / 186

Commercial 0.52% / 125

Domestic 2.35% / 48177

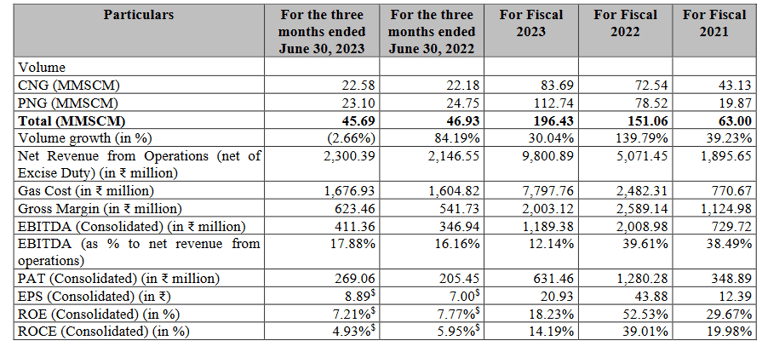

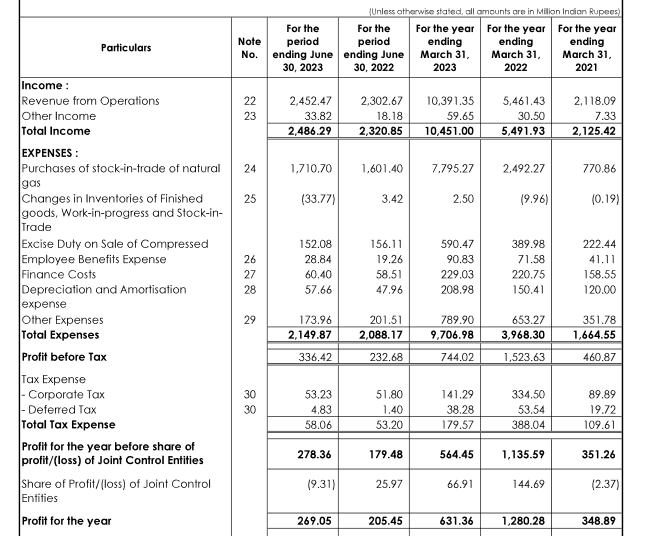

Financials

Annual revenues of IRM Energy is 1040cr. PAT 60cr.

Revenues became 5X in last 2 years, PAT > 2X in 2 years.

PAT not increased proportionately owing to abnormal natural gas prices last year - H1 FY23, due to Ukraine-Russia war ( natural gas long term average price 2.8USD/MMBtu, which shot above 8 USD/MMBtu Apr-'Sep23)

Margins of all players drastically reduced in FY23 due to sharp spike in gas prices. Raw material cost which used to be 36% of revenues in FY21, shot up to 79.6% of revenues in FY23.

EBITDA margins 12% (peers at 20%, comparable Gujarat Gas 15%)

PAT margins 6.1% ( peers 12%, comparable Gujarat Gas 9.1% )

ROCE at 18% ( peers > 23%)

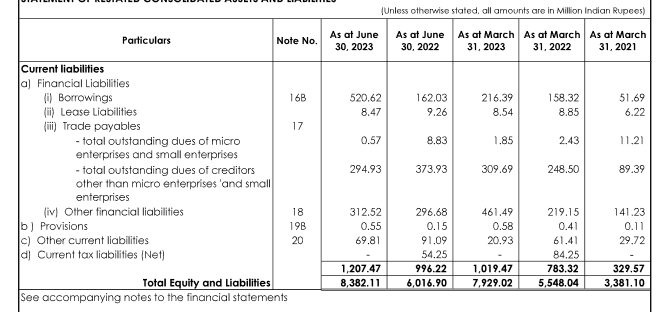

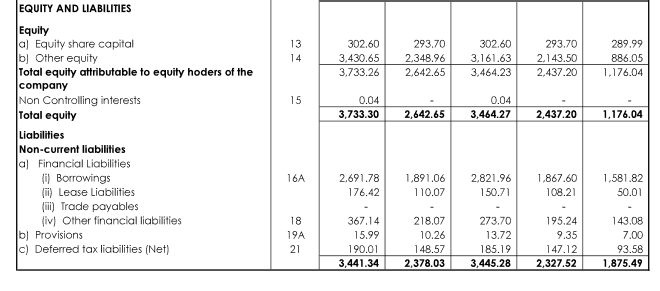

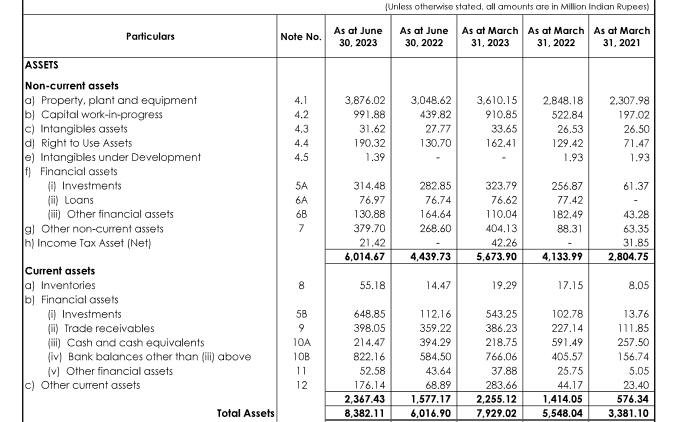

Balance sheet ( amount above in Rs millions)

Borrowing at 303 cr

Debt/ equity ratio at 0.87 ( peers have little debt, all < 0.4

Cashflow from operations 46cr ( adequate for last 3 years)

Cash & cash equivalents 22cr