Manoj Vaibhav Gems N Jewellers Business Analysis

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

Manoj Vaibhav Gems, started in 1994, by late Manoj Kumar Grandhi based out of Vizag , currently led by Bharata Mallika Ratna Kumari Grandhi along with her daughter Grandhi Sai Keerthana is a leading jewellery regional jewellery brand in Andhra Pradesh and Telengana. They were one of the first movers in the organised jewellery retail industry of Andhra Pradesh. Their main focus is tapping the high growth untapped regions within the micro-markets of Andhra Pradesh & Telangana. 77% of stores are in Tier 2/Tier 3 cities.

Manoj Vaibhav Gems operates through store network of 13 stores ( 2 franchisees) spread across Andhra Pradesh, Telangana across 10 towns. They follow a hub and spoke model with smaller showrooms in tier 2/ 3 towns surrounding a bigger one in main city.

Their flagship showroom V Square spanning 29,946 sqft is one of the largest in Visakhapatnam.

Store location distributed as follows

Tier 2/Tier 3 77%

Hyderabad 15%

Vizag 8%

Since jewellery sale is about deeper trust building, Manoj Vaibhav Jewellers undertake several activities to foster customer connect as they follow go-to-market strategy

1. focused group discussions

2.exhibitions to showcase new collections

3. village campaigns

4. door-to-door activities for direct selling

Manoj Vaibhav Gems has a market share of 4% of the overall Andhra Pradesh and Telangana jewellery market and 10% of the organized jewellery market of Andhra & Telengana.

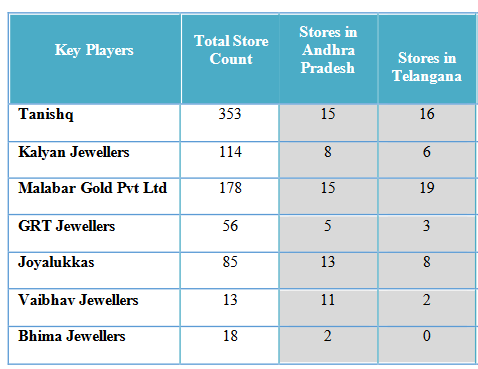

Main competitors are Titan, Kalyan Jewellers, Malabar Gold, Joyalukkas.

Industry overview

The Indian jewellery market size Rs 5,74,000cr in FY23, expected to grow at 15.3% CAGR for next 4 years. 68% of industry is unorganized, 32% organized, mostly brick & mortar with limited online sale.

Gold demand in rural India

Rural India forms 58% of gold jewellery demand. Gold jewellery buying for rural customers are not for luxury, but an investment for any future needs when they can sell off , pledge the jewellery to take loans. 60-70% of the rural demand for jewellery is driven by weddings followed by the need for investment post -harvest. Rural market in the state of Andhra Pradesh and Telangana contributes 50-52% of the total jewellery market.

Breakup of gold demand as per use

Bridal wear 55%

Daily wear 35%

Fashion wear 10%

Key trends shaping the industry are

1. GST and mandatory hallmarking creating challenge for unorganized players

2. Unorganized to organized shift in industry continues

3. Gold jewellery has different regional preferences

Geography wise gold demand

South 40%

West 25%

North 20%

East 15%

Andhra & Telengana market size is Rs 50000cr expected to grow at 18% CAGR.

Manoj Vaibhav Gems has a market share of 10% in organized jewellery in Andhra & Telengana.

Major competitors having strong presence in these 2 states are Titan,Joyalukkas, Malabar Gold and Kalyan Jewellers.

Points to consider

10% share of organized jewellery market is significant,considering 4 other prominent players are present in those states including leader Titan. But bigger players Titan and Kalyan are expanding network very fast with access to much higher capital base. Along with that, Joylukkas and Malabar gold also have significant presence in Andhra. So significant competition is there, and jewellery business favours larger organized players as lot of capital is required to expand fast in jewellery owing to huge inventory cost of gold, considering capex is done through franchisee mode.

65% of revenues comes from Vizag only, so there is significant dependence on single town.

Contingent liabilities of 8cr ( income tax demand under dispute). Related party transactions are high 374cr (19% of revenues), owing to customer gold scheme advances were being taken under HUF GMB Ratna Kumari, which has been discontinued since June 22. Company itself has started its new customer advance scheme for gold buying which all leading jewellers do.

Revenue/ sqft are more than 2x of even Titan. Other metrics are comparable to Thangamail and Kalyan.

Valuation

Manoj Vaibhav Jewellers is valued at P/E of 14.5, whereas comparable peer Thangamail trades at P/E of 27, Titan trades at 90, Kalyan 45. Recently, Senco Gold brought IPO valued at P/E of 15.

You may be interested in

Senco Gold IPO Analysis

How to do IPO analysis for listing gain

How to avoid companies like Brightcom/ BCG ? Investing red flags

Will Jio Financial disrupt Bajaj Finance

Follow us on twitter

#themoatinvestor #dmoatinvestor #manojvaibhavgemsipo #listinggain

Operating metrics

Manoj Vaibhav Gems has significant presence only in Andhra, 11 stores. Tanishq and Malabar Gold have 15 stores each in Andhra.

Average revenue / sqft is Rs 54750 (Titan Rs 21950),despite most of their stores are in Tier 2/Tier 3 towns.

Average revenue/ store is Rs 150cr ( Titan Rs 90cr, Kalyan 77cr)

Segment wise revenues (Total revenues 2030cr)

Gold 89%

Others (Platinum, Diamond, Silver) 11%

Revenue contribution region wise

Vizag 65%

Hyderabad 6%

Tier 2/ Tier 3 29%

8 new stores that will come up in 2 years.

Comparable regional peer is Thangamail jewellers, net margins of Manoj Vaibhav Gems better than Thangamail, and similar to Kalyan.

Financials

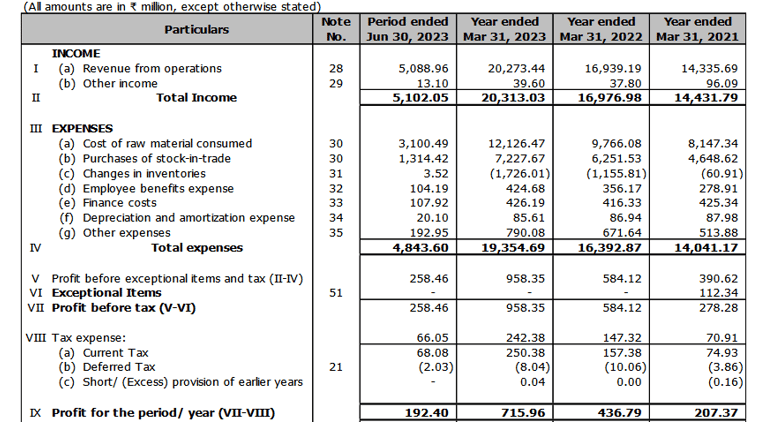

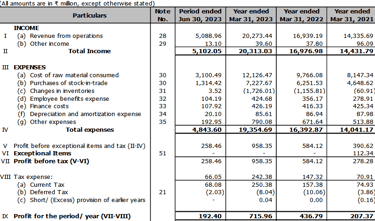

Annual revenues of Manoj Vaibhav Gems is 2030cr. PAT 70cr.

Last 18 year revenue CAGR since 2005 is 22.7%

EBITDA margins 7.3%%

PAT margins 3.5%

ROCE at 17.7%

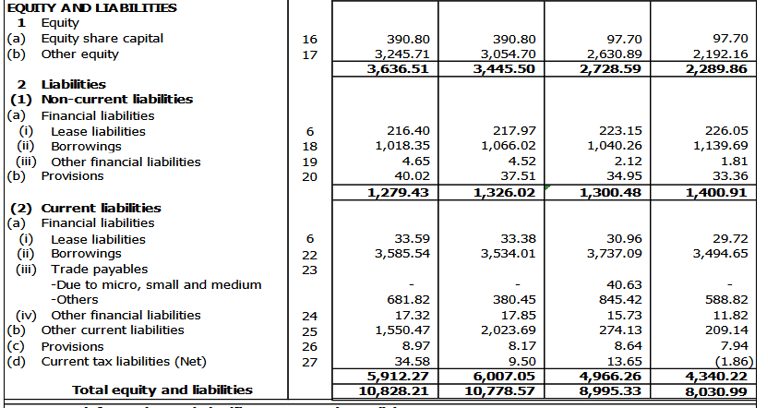

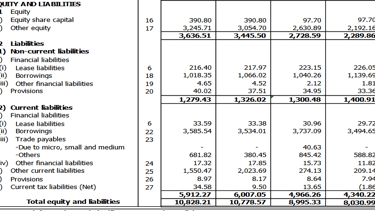

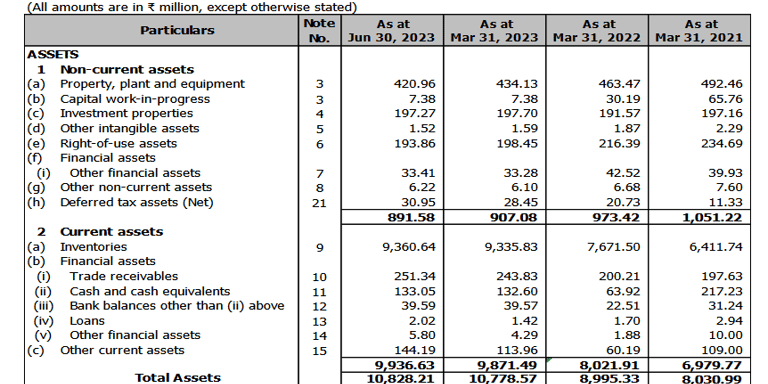

Balance sheet ( amount above in Rs millions)

Borrowing at 460cr

Current debt/ equity ratio at 1.41

Cashflow from operations 70cr

Inventory is 930cr ( inventory turns 2.2),for Kalyan 2, Thangamail 3.2

Ad spends 0.44% of revenues ( Thangamail 0.88%)