Senco Gold IPO analysis

Content

1.History & brief of company

2.Industry overview

3.Geographical presence

4.Operating metrics

5.Financials

6.IPO Size & utilization of funds

7.Moat

8.Points to consider

9.Valuation

History & brief of company

Gold is a discretionary consumption item (8% of total consumption spends by Indian households are gold purchases, mostly in the form of jewellery). Majority of sales is driven through seasonal occasional purchases ( wedding jewellery).

Senco gold is a gold jewellery retail chain operating mainly in Eastern India.

Senco gold started its operations in 1994 in Kolkata by Sankar Sen, currently run by his son Suvankar Sen. It is a promoter run company with presence of PE investors.

In 2000, it launched its 1st store in franchisee model in Durgapur ( WB). In 2004, Senco opened its 8000 sq ft showroom in heart of Kolkata, Moulali. In 2010-12, it expanded in Assam, Jharkhand through its franchisees. Between 2013-15, PE investor SAIF fund invested 80 crores. They had 50 stores by now. In 2016-18, they expanded to South. By 2020, they had 100 stores. In 2022, Senco received 75 cr equity infusion by OIJF.

2. Industry overview

Gold jewellery is the one of the largest consumers spends after food & grocery. Indians spend 7.6% of private retail consumption spends in gold. Gold demand is primarily fuelled by wedding demand ( compulsory purchase) and rest by festive demand, occasional purchases.

Total industry of 5,74,000 crore, out of which 66% is gold jewellery, 34% is gold bars/coins.

Share of organised players is only 32-36%, rest unorganized.

Industry CAGR is 14%, organized players CAGR is 20% ( F16-22)

Gold is purchased on the basis of TRUST, so it takes a long time to build trust, and once it is built, people visit the same jeweller for generations. In India, that's the reason,most jewellers are regional players. Only Titan has emerged as national player after so many years of hard work and earning trust of customers, also being the first mover with large scale operations across India.

3. Geographical presence

So Senco is 3rd largest jewellery retail company in India, and largest in Eastern India.

Nearest comparable competitor is Kalyan jewellers.

Average store size 3000 sq ft. Stores evenly distributed among metro/ tier 1/ tier 2/ others.

70% of stores in west bengal.

Out of 136 stores, 75 COCO (Company owned company operated), 61 franchisee owned ( franchisee experience since 2000) , whereas Kalyan started giving franchisees in 2022 only.

Revenue contribution city wise

Metro 35%

Tier 1 33%

Tier 2/3 29%

WB contributes 70% of revenues, rest of East/ North 12%, ROI 15%

4. Operating metrics

Senco operates in hub and spoke model. They open an own store (COCO) in a city, and surrounding that, opens a number of franchisees in smaller towns.

Average store size 3000 sq ft. They operate in a low capex model with 25/ 75 revenue sharing with franchisees.

Capex/ store for setting up new store is 13cr.

Revenue mix

Gold jewellery 90%

Diamond/ Semi precious 7%

Silver / platinum 3%

They are looking to increase contribution of diamond.

Kalyan has 65% gold , rest studded jewellery which is a higher margin business.

They have brands like Everlite for fashion jewellery ( emerging trend of light weight lower cost jewellery for office wear, casual wear among working women) costing 29000.

Average ticket size is Rs 60-70000, catering middle- upper middle class.

65-70% of purchases are of Rs 50000.

They charge making charges 1-2% higher than peers showing pricing power.

Senco has installed XRF- Gold testing machine in all showrooms for trust.

Bengal is known for gold karigars ( even Titan sources their Karigars from Bengal).

Senco has 170 karigars in and around Kolkata, bound by Karigar agreement with them. Karigars take 10-30 days to prepare a design.

Similar to all gold jewellers, Senco runs a loyalty scheme under which 7 lakh customers are enrolled.

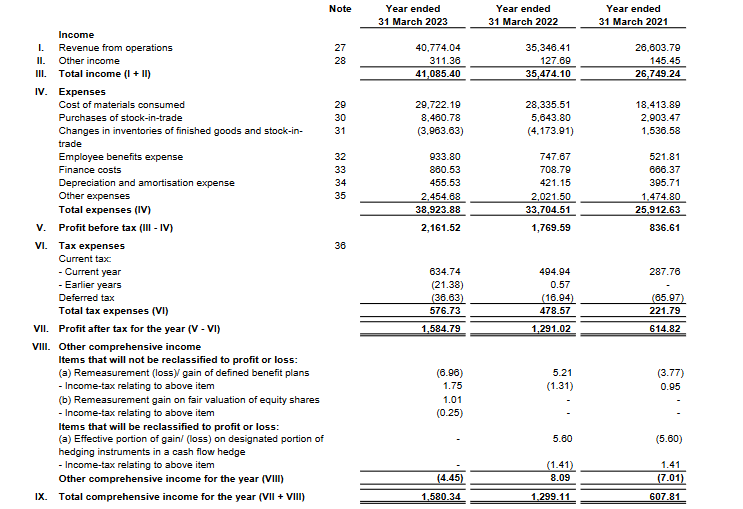

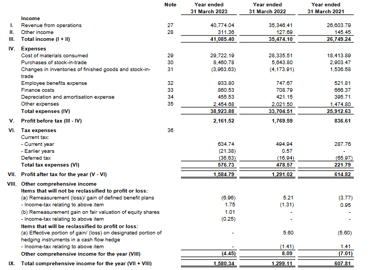

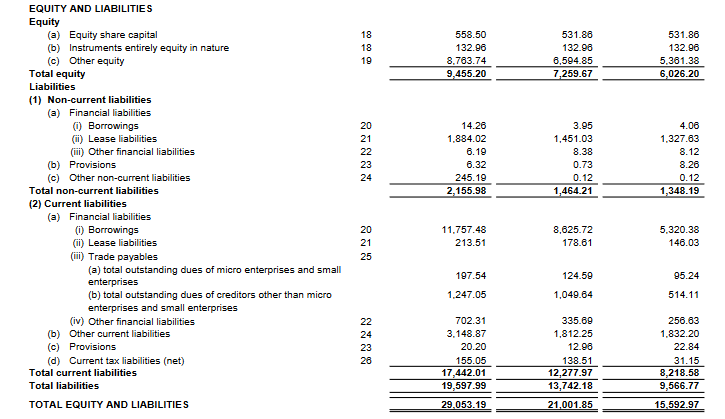

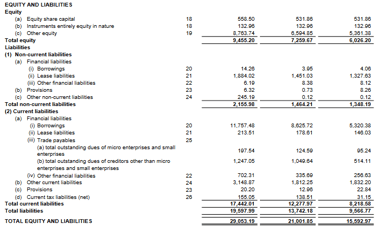

5. Financials

Figures in Rs millions.

4 year revenue CAGR for Senco 24%

EBITDA margins of 7.8% ( same as Kalyan).

In terms of consistency in profits, Senco is more stable than Kalyan.

Marketing spend 2% of revenues similar to Kalyan ( Kiara, Sourav Ganguly , Vidya Balan have been ambassadors).

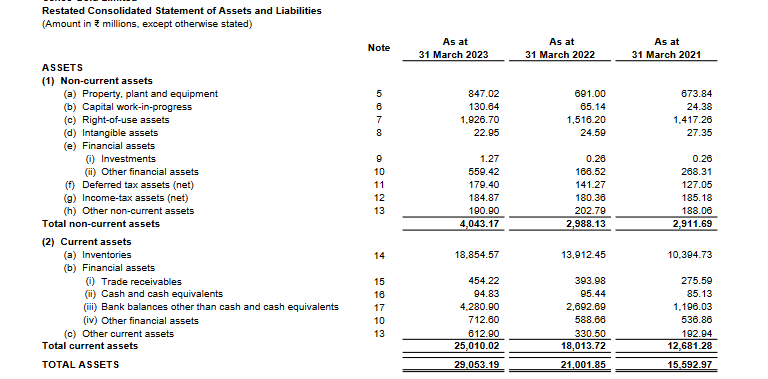

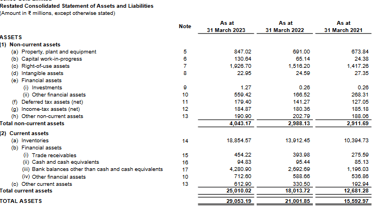

Balance sheet

Inventory turns 2.4 times, inventory days 169

Debt 1180 cr ( short term in nature, gold metal loan and working capital loan)

Inventory 1885 cr( finished goods 1200cr)

Debt/ equity 1.2

Cashflow negative for F22 and F23.

7. Moat

Deep demand side moat in West Bengal through network ( 70% of revenue) , earned trust through years of operations. In gold business, trust towards the jeweller is an important moat which is developed through years of relationship with the customer, often continued through generations. Gold jewellery buying is still dominated by regional players who have earned this trust from the customers through years of operations in the region. Senco is one such player in West Bengal, and since Kolkata is the hub of Eastern India, this has a rub off effect across East as brands popular in Kolkata enjoys a rub off effect in Eastern India.

Also, most of gold karigars of India are from West Bengal ( even in Titan ) , so no supply side disruption or delay. Cheaper job work charges. This is another moat.

Senco charges 1-2% premium on making charges than other players indicating they have pricing power.

7.Points to consider

Senco will deepen its presence further in East and expand in North to leverage its existing position.

Senco operates in asset light model- no company cost involved in setting up franchisees.

While future growth plans not revealed in detail ( opened 24 stores from F21 to F23 despite covid) out of which 15 COCO, 9 franchisee .

With cash & bank balance of 440cr, and PAT of 158 cr, Senco can grow own stores with own capital ( 1.3 cr capex/ store )

Senco has significant room to increase Sales/ store which is 30cr / yr ( kalyan 77 cr )

8.Valuation

Listing PE of 15 at price 300 at significant discount to its peers ( Kalyan 33, Thangamail 28 )

#sencogoldipo #stockanalysis #titan #themoatinvestor #DMoatInvestor