IRCTC Business Analysis

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Business

IRCTC ( Indian Railway Catering & Tourism Corp) started in1999, is a PSU owned by govt, subsidiary of Indian Railways, a Mini Ratna PSU. IRCTC is a govt. regulated monopoly with 82% market share of railway tickets booked. All tickets booked online are routed through IRCTC ( even tickets booked on other aggregator sites like Makemytrip, Paytm etc).

The e-Ticketing System was replaced with Next Generation E-Ticketing (NGeT) System from Apr 2014 and the capacity of per minute ticket booking was increased progressively. The NGeT system is supported by high capacity servers which has got a capacity to book more than 26,000 tickets per minute. It had witnessed a record booking of 28,434 tickets in a minute on 12th November 2022.

Convenience charges at IRCTC site (~2%) being lower than others, makes customers book tickets directly from IRCTC site. Charges on IRCTC site is less than half that of other aggregator sites.

IRCTC launched IRCTC HDFC Bank co-branded Credit Card on RuPay platform on Mar-23. Substantial booking through AskDisha Chatbot- total tickets booked was 5.78 Lakhs and total revenue earned is Rs 85cr.

Revenue Streams

1. Ticketing 34%

2. Catering 42%

3. Rail Neer 9%

4. Tourism 15%

1. Ticketing (34% of revenues)

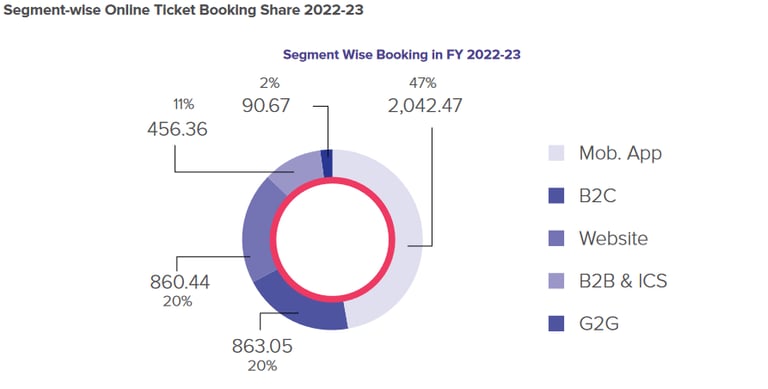

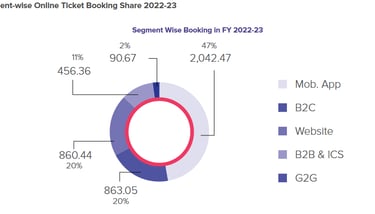

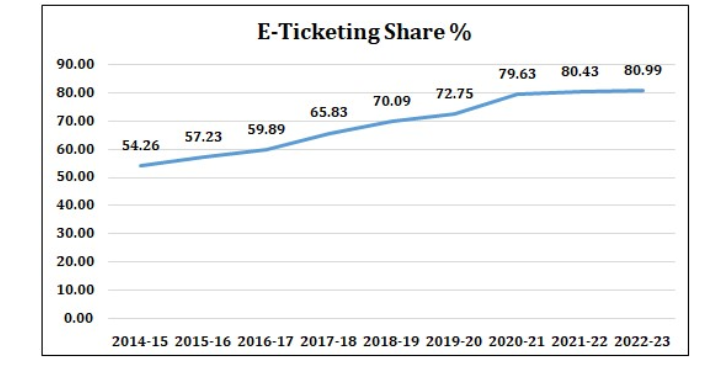

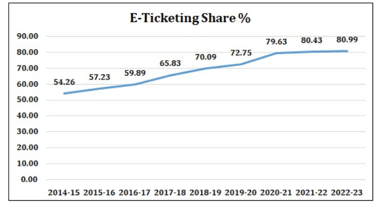

Under ticketing , IRCTC earns from service charges of ticket booking ( main source) , and also agent annual fees and running ads to captive customer base who keeps revisiting for ticket booking. 82% of rail tickets booked in FY23 were online booking.

Out of 1200cr ticketing revenues,

ticket booking 800cr ( 67%)

Fees from agents/ Ad rev 400cr

2. Catering (42% of revenues)

Static catering - Running the food centres at stations - Food Plaza, Jan Aahaar, cell kitchens, food courts and refreshment.

Mobile catering- Running the pantry cars/ base kitchens in around 400 Express trains including Rajdhani / Shatabdi / Duronto, Gatiman / Tejas / Vande Bharat

E-catering- this is the newer service where customers can order foods from partner restaurants like Dominos, Haldirams, Subway, KFC . 17,865 average meals served per day across 200+ stations in FY22.

Industry overview

OTA (Online Travel Agency) industry in terms of net revenues is 11000cr, expected to grow at 14-15%.

Breakup of the travel industry

Airline ticketing 52%

Hotel booking 30%

Rail ticketing 18%

All railway tickets are booked via IRCTC , even those through other OTAs like Makemytrip, Yatra.

Growth Drivers

1. Continuous expansion of India Railways Network and focus on making India Railways Future-ready by 2030. Railway budget for FY24 is 2,60,000 cr, up from 1,90,270cr in FY22. Modernisation of railways with introduction of new AC coaches, Vande bharat like trains with improved speed, wider tracks- will foster growth of railway passenger traffic across India.

2.Per capita income growth

With per capita income growth, discretionary spends on travel to increase, leading to growth in OTA industry, along with further increase in share of online booking will drive the growth.

2. Growth of internet users in India by 2025

As per a report published by Internet and Mobile Association of India (IAMAI) titled ‘Internet in India’, at present there are around 69.2cr internet users in India which is estimated to become 90cr by 2025. At present, 34.6 cr Indian users are already engaged in making online transactions including digital payments. This coupled with the fact that IRCTC has 8 crore registered active users for online reserved rail tickets as on 31st March, 2022 presents IRCTC a great opportunity to establish e-commerce services through its digital asset.

3. Growth in Digital Payments:

In past five years, India’s digital payment volume has seen an average annual growth of about 50 percent. Growth for individual digital payment users is set to triple in five years to 75cr. The digital payments industry will more than triple to $10 trillion by 2026 from existing $3 trillion today. Non-cash payments in India will constitute nearly 65 per cent of all payments by 2026, up from 40 per cent today, and almost 75 per cent of people will use India’s unified payment interface (UPI) in the next five years, up from the existing 35%. The Indian travel industry was estimated at Rs 2,83,000cr in FY23, expected to grow at CAGR of 9-11% Online penetration is 66-68% which is expected to go to 73-75% in FY27.

3. Rail Neer (Packaged drinking water) (9% of revenues)

Manufacturing and bottling of packaged drinking water under brand Rail neer, 15 plants run under PP model. Rail Neer is a considered reputed brand similar to Kinley, Bisleri, Aquafina. IRCTC is planning to serve bottled water outside railway premises under PPP model. Capacity utilization of Rail Neer is 75% and the capacity is around 18 lakh bottles/ day.

4. Tourism ( 15% of revenues)

Non rail based tourism

Tour packages, hotel bookings, car rentals, air ticketing, educational tours, medical tourism. IRCTC aggregates around 6,900 hotels across 435 cities with most hotel not charging any money if booking is cancelled atleast 24 hrs ahead of the check-in. All bookings facilitated through https://www.irctctourism.com

Rail based tourism

Special tourist trains like Buddhist Circuit, Bharat Darshan

Luxury trains like Maharaja Express and Golden Chariot, State special tourist trains

Operating metrics

Passenger traffic

F20 767cr

F23 586cr

Railway passenger traffic has decreased 24% from pre-covid levels.

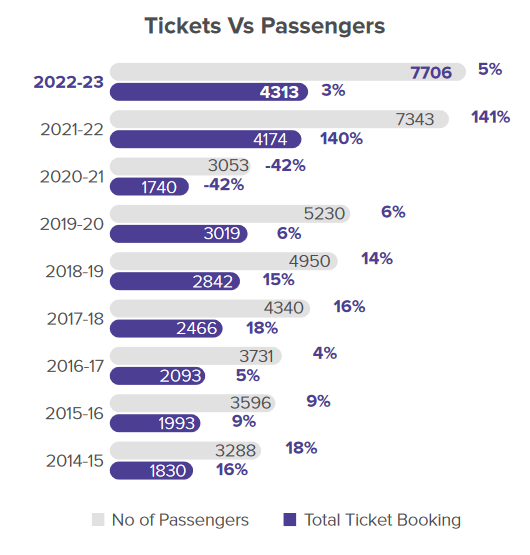

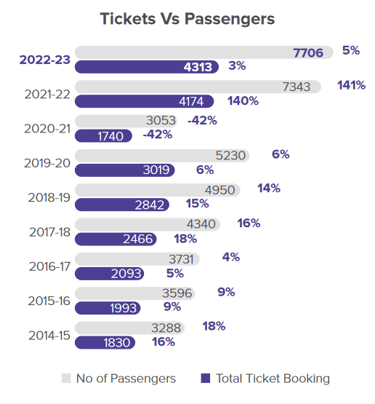

Tickets booked/day

F23 11.57 lakh

F20 8 lakh

% tickets booked online 81%

Total tickets booked

Q1 F24 10.42cr

Q1 F23 11.56cr

Q1 F24 vs Q1 F23

AC tickets 4.84cr vs 4.04cr

non AC 5.58cr vs 7.54cr

Growth is coming from more AC ticket bookings, where convenience fees for ticket booking are higher. Non-AC tickets booked have decreased quite a lot YOY.

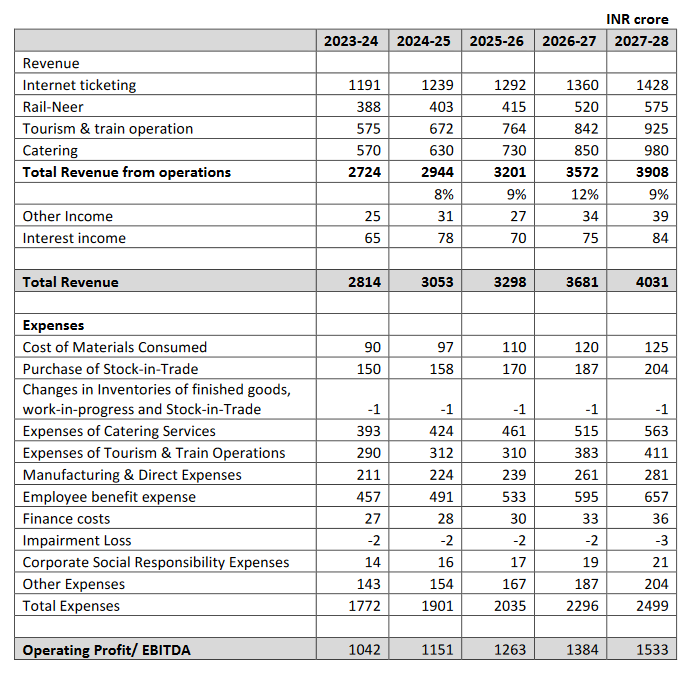

Financials

Revenues FY23 3550cr. PAT 1000cr.

Revenue CAGR last 4 years( pre covid) is 11.6%

PAT CAGR last 4 years 18.3%

EBIT (PBIT) 1270cr vs 700cr (21.7% CAGR)

EBIT share- segment wise ( total EBIT 1354cr)

1.Ticketing 1020 ( 75%)

2.Catering 170 ( 12.5%)

3.Railneer 36

4. Tourism 45

Interest & dividends 83cr

Overall EBIT margin 35% ( vs F20 EBIT margin 31%)

As we see, ticketing business is the main profit earning business ( 75% of profits come from ticketing).

Catering business earning 42% of revenues make up only 12.5% of profits. Entire growth of company depends on how ticketing business performs.

ROCE 60%

IRCTC is a debt free company.

The total revenue of IRCTC supposed to grow at a CAGR of 9.4% between FY 24 to FY 28 , operating profit should grow at a CAGR of 10% between the same period. ( as per corporate plan document of IRCTC)

Points to consider

Railway Passenger traffic still didn't return to pre-covid levels is a concern , shortfall of 180 cr cannot be justified by increase in air traffic. Sleeper passenger trend reducing from pre-covid levels has led Indian Railways to reduce sleeper coaches and increase 3AC coaches in passenger trains.

More premiumisation (AC tickets) will drive more revenues , hope IRCTC and Railways does enough in terms of requirement of putting additional AC coaches in peak travel seasons , thus not losing important revenue source for both Railways and IRCTC. Rail minister has said that waiting list will be over by FY30.

Despite passenger volumes dropped 24% from pre-covid , due to increasing % of tickets booked online and increase in AC tickets, revenues and profits have increased.

IRCTC is focussing on increasing non-ticketing revenues like agent fees/ ad revenues ( 400cr) and lot others happening in catering front also, but margins are thin there.

Being a regulated monopoly, it is a safe business with very strong moat, only changes in govt policy like opening ticketing to private players will end the monopoly.

Changes in policies regarding catering contracts of Railways to IRCTC may hamper growth.

Govt deciding to modernize Railways with introducing high speed trains, high speed railway corridors will mean further growth for IRCTC

Detailed analysis of Yatra Online ( recent IPO)

Follow us on twitter

You may be interested in

Tata Technologies business analysis

Mamaearth business analysis

Will Grasim disrupt Paints industry?

#themoatinvestor #dmoatinvestor #irctcbusinessanalysis