Yatra Online Business Analysis

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

Yatra Online, started in 2006, based out of Gurgaon, is the 3rd largest OTA( Online Travel Agent), largest in terms of number of corporate clients. B2B travels or Corporate OTA segment is the main focus Yatra Online.

Product segments

1. Airline ticketing

Yatra earns commissions and incentives from airlines for tickets booked by customers, along with revenue from convenience fee, cancellation service charges, rescheduling charges and advertisement revenue.

2. Hotels and holiday packages

Hotels

Revenue from Hotels and Packages business includes commissions and markups earned from standalone hotel rooms and packages. Revenue from packages ( which combines hotel and airline tickets sold as a package) is accounted for on gross basis.

Holiday packages

Holiday packages include travel, including flights, hotels, sightseeing, transport, visa and insurance, all taken care of together. Yatra also allows their platform to third-party holiday packages sellers, thereby increasing choices for customers.

3. Other services- consists of rail tickets, bus tickets, taxi rentals

Yatra Freight - new business

By leveraging Yatra Online’s robust relationship with air-carriers, large corporate and SME customers, Yatra has started technology-enabled digital freight forwarding platform covering ocean freight, surface logistics and air cargo in 2020.

Yatra Online has 813 corporate accounts and 49800 SME customers.

Yatra has a market share of 5.2% in terms of OTA industry revenues.

Industry overview

The Indian travel industry was estimated at Rs 2,83,000cr in FY23, expected to grow at CAGR of 9-11%

Online penetration is 66-68% which is expected to go to 73-75% in FY27.

OTA (Online Travel Agency) industry in terms of net revenues is 11000cr, expected to grow at 14-15%

B2B OTA is at 4500cr(expected CAGR 14-15%)

Breakup of the travel industry

Airline ticketing 52%

Hotel booking 30%

Rail ticketing 18%

Growth drivers

With per capita income growth, discretionary spends on travel to increase, leading to growth in OTA industry, along with further increase in share of online booking will drive the growth.

Market leader is MakeMyTrip with 24% market share, and other players are Easemytrip, Cleartrip, Ixigo. In B2B travel segment, competitor is Thomas Cook.

Points to consider

Market leader Makemytrip is still loss making, despite having 24% market share and 12 times revenues of Yatra Online, indicating there is significant cash burn involved in terms of customer inducement/ customer acquisition cost which is 39% of revenues for Makemytrip.

Hotel & package booking is higher margin business, but leading hotels are trying hard to get direct bookings from customers through their own online channel/ customer relations, which may affect premium segment. Plus there are competition from hotel aggregators like Oyo, homestay aggregator like Airbnb in the mass segment.

75% reserved for QIB, 451cr, out of which 348 cr already raised from anchor investors gives a signal that professionals are interested in the business.

Valuation

Yatra online is valued at P/E of 286, and P/S of 5.9x, whereas similar sized listed peer Easemytrip is at P/E of 48, P/S of 15x, with much better profitability and operating metrics.

You may be interested in

How to do IPO analysis for listing gain

How to avoid companies like Brightcom/ BCG ? Investing red flags

Will Jio Financial disrupt Bajaj Finance

Zaggle Prepaid IPO Analysis

Follow us on twitter

#themoatinvestor #dmoatinvestor #yatraonlineipo #listinggain

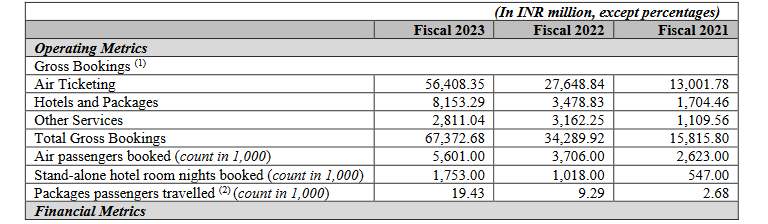

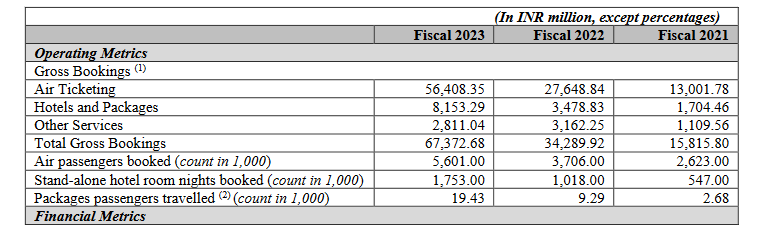

Operating metrics

Gross booking revenues is Rs 6740cr (Makemytrip Rs 53790cr). Gross booking revenues is total ticketing or hotel booking values.

Total air passengers served in FY23 is 56 lakhs.

Total standalone hotel room nights count at 17.53 lakhs (Makemytrip 253 lakhs)

Comparison of metrics vs FY22, FY21 will not yield correct picture as travel was highly reduced due to covid during those years.

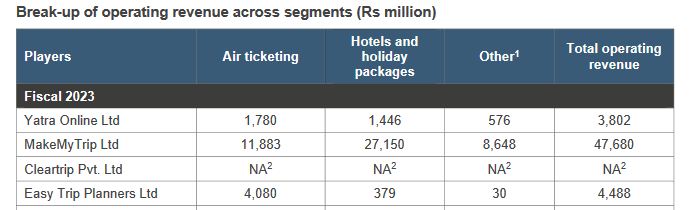

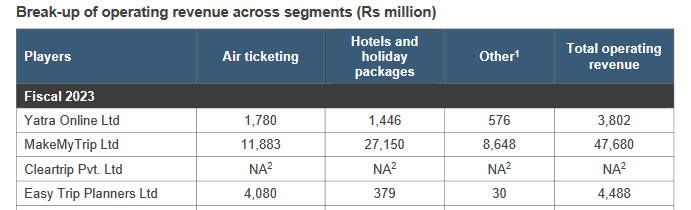

Segment wise revenues (Total revenues 380cr)

Airline ticketing 47%

Hotel & package 38%

Other(rail/ bus) 5%

Total corporate clients under Yatra Online is 843 (Makemytrip 249), SME clients 49800 (Makemytrip 45000).

Total domestic hotel tie-ups at 105600 hotels ( Makemytrip 60000), and travel agent roped are 29800 (Makemytrip 36000)

90% traffic to Yatra Online is organic. Yatra operates through single platform Yatra unlike Makemytrip which has Makemytrip, GoIbibo, Redbus ( bus tickets), and mybiz subdomain for corporate travels.

Market share of Yatra Online is 5.3% where leader Makemytrip has 24% market share.

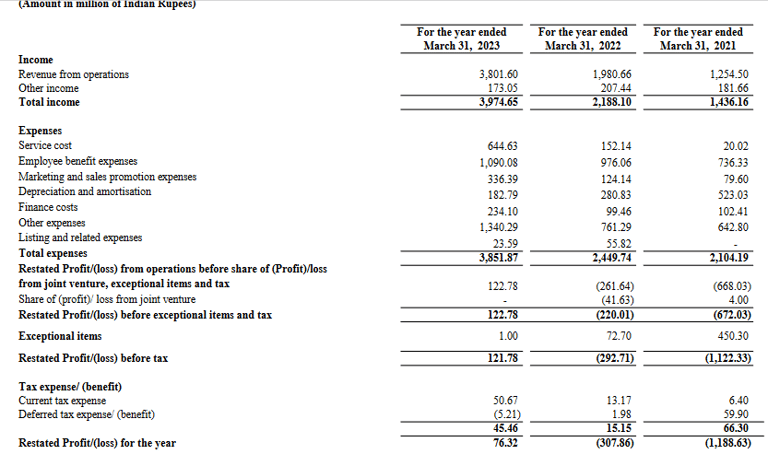

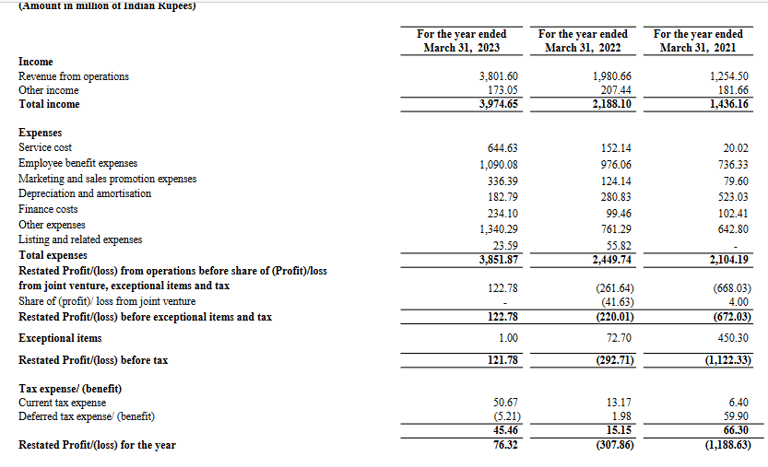

Financials

Annual revenues of Yatra Online is 380cr. PAT 7.6cr. ( though PAT as per SEC filings at Nasdaq ( Yatra is listed in Nasdaq)) is Rs 29cr loss, may be due to different revenue recognition policy for US, forex losses wrt rupee depreciation etc)

Take rates ( Operating revenues/ Gross booking revenues) of Yatra Online is 5.7% ( Malemytrip 9.1%, Easemytrip 6%)

Adjusted margins- segment wise

Airlines 7.7%

Hotel 13%

Others 6.3%

EBITDA margins 17.6%( Makemytrip 10.2%)

PAT margins 2% ( Makemytrip is loss making Rs 90cr loss)

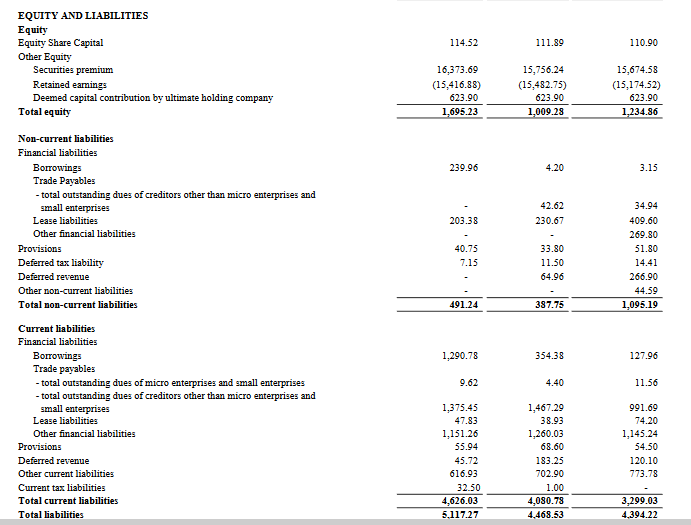

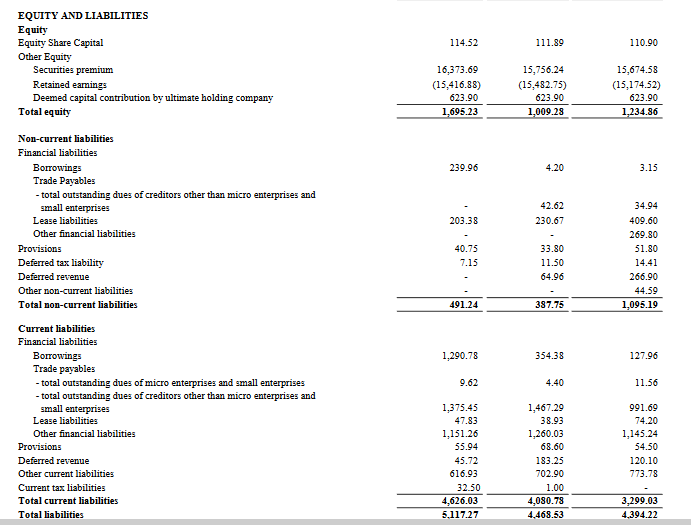

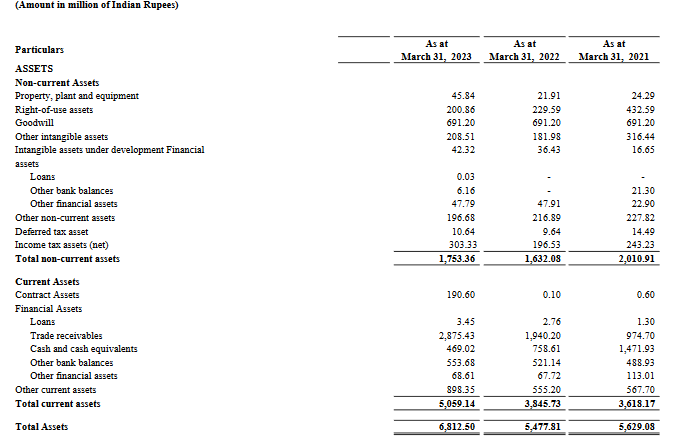

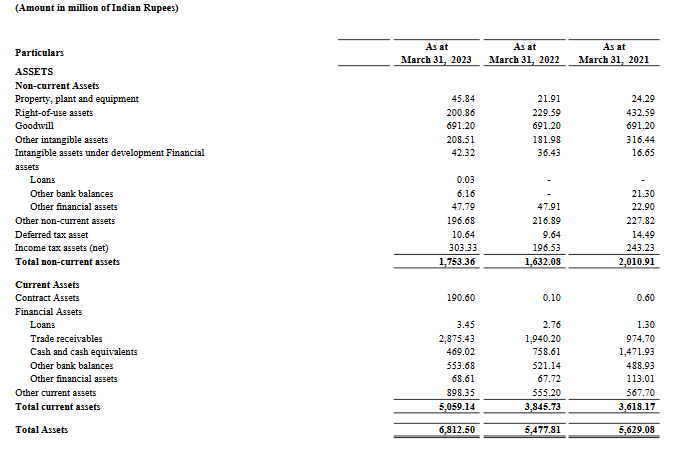

Balance sheet ( amount above in Rs millions)

Borrowing at 153cr

Current debt/ equity ratio at 0.9

Trade receivables 287 cr. ( quite high for 380cr revenues)

Cash equivalent of 47 cr.

Cashflow from operations negative -153cr.

Provisions for doubtful debts 33cr total for last 3 years.