EMS Ltd Business analysis

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

EMS Ltd, started in 2012, by Ramveer Singh, based out of Ghaziabad, is a Class A contractor with operations in Sewerage solution , Water Supply System, Water and Waste Treatment Plants (WTP/ETP) and operation and maintenance of Wastewater Scheme.

100% business occurs through tendering process in all govt bodies like CPWD, State govt, Local Municipal bodies.

EMS has in-house team for designing, engineering and construction engineers - total of 61 engineers. EMS is involved in design and engineering of the projects, procurement of raw materials, execution at site with overall project management up to the commissioning of projects a well as post commissioning, operations and maintenance. Currently, EMS is operating 18 projects and 5 O&M projects in 5 states.

All of the projects are world bank funded through local state government bodies, leading to less chances of payment defaults.

Major areas of work done by EMS are

1. Sewage treatment plants and Sewage Schemes

Involves collection of the domestic wastewater from each household through pipelines, and intermediate pumping stations, to take it to a common facility which is called a Sewage Treatment Plant where this sewage water is treated for reuse

2. Common Effluent Treatment Plants (CETPs)

Recycling and reuse of contaminated wastewater produced by different industries- which is a mandatory requirement of many industries today for clearing environmental clearance.3. Water Treatment Plants and Water Supply Schemes

Scope of work includes Raw water pre-treatment , clarification ( so that solid settles), filtration plants through filters, disinfection through chlorination and UV treatment

Industry overview

Rapid urbanization requires planning of sewerage, clean and affordable water. It is expected that by 2050, about 1450 km3 of water will be required. Because of growing urbanization, the need for drinking water will be a critical factor. River contamination by release of urban wastewater has raised serious challenges for urban wastewater management, planning and treatment.

Government Initiatives

• Jawaharlal Nehru National Urban Renewal Mission

• Namami Gange programme

• Atal Mission for Rejuvenation and Urban Transformation (AMRUT)

• Swachh Bharat Mission (Urban)

• Jal Jeevan Mission

Wastewater generation is expected to be 33,212 MLD in FY 23. Existing capacity of sewage treatment is only 6,190 MLD, indicating a 22,939 MLD ( 79%) capacity gap between sewage generation and existing sewage treatment capacity.

They key drivers of water supply are govt's increasing focus on improving water availability, rejuvenation of water bodies,wastewater processing, agri and industrial water reuse.

Comparable listed peer is VA Tech Wabag.

Points to consider

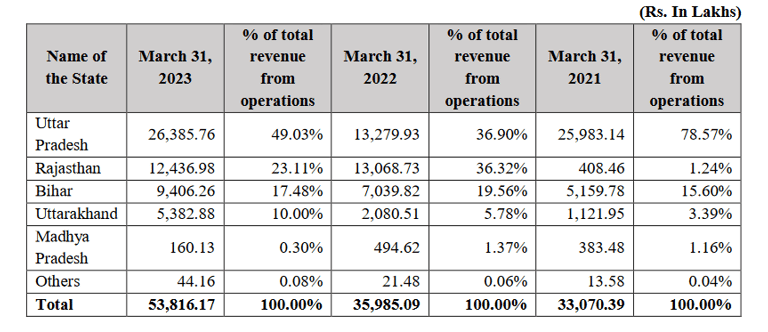

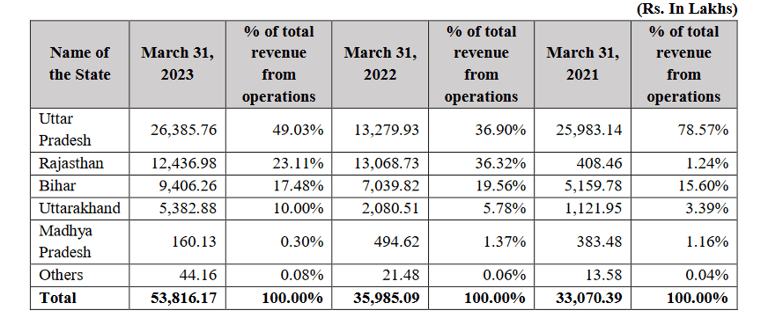

49% of revenues come from UP, significant geography concentration is there.

Most of the projects are backed by World bank funding, so very less chances of payments defaults.

EMS has robust order book of 1745cr ( > 3X of annual revenues)

Business is working capital intensive in nature, working capital is 53% of revenues for FY 23. Delay in payment of high value projects may affect liquidity. Though EMS is favourably placed post- IPO in terms of working capital funded, and company has no significant debt.

As mentioned, there is significant gap between waste water generation and waste water treatment in India.

Valuation

EMS Ltd valued at P/E of 10.8

Bigger size comparable peer Va Tech Wabag trade at P/E of 10-14.

You may be interested in

Vishnu Prakash IPO Analysis ( recent IPO govt projects delivering company)

Jupiter Hospitals IPO Analysis

How to do IPO analysis for listing gain

How to avoid companies like Brightcom/ BCG ? Investing red flags

Follow us on twitter

#themoatinvestor #dmoatinvestor #emsltdipo #listinggain

Operating metrics

EMS operates in 5 states, UP, Rajasthan, Bihar, Uttarakhand, MP. They will expand to South and North East in future.

49% of revenues come from UP, another 41% from Rajasthan and Bihar.

Total order book as on July '23 is of 1745cr ( > 3x of annual revenues)

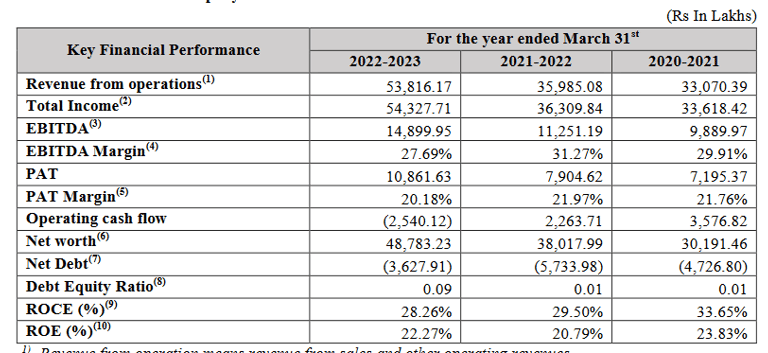

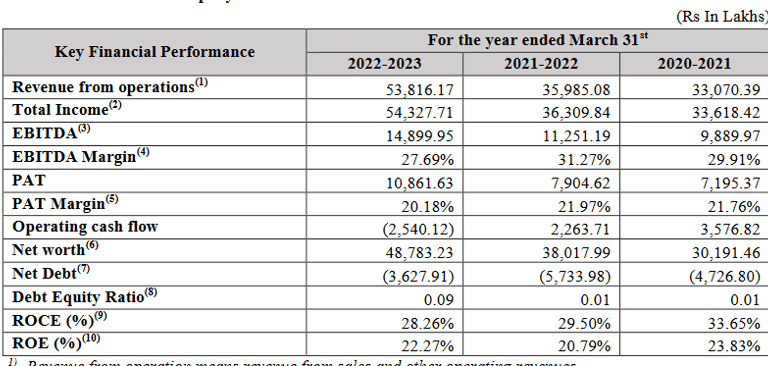

Financials

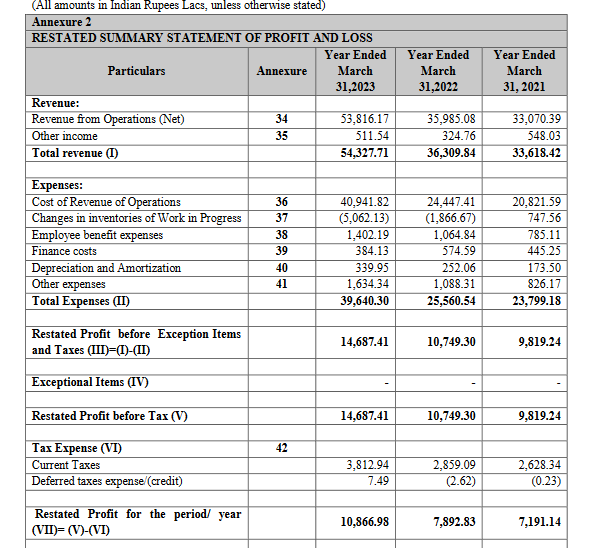

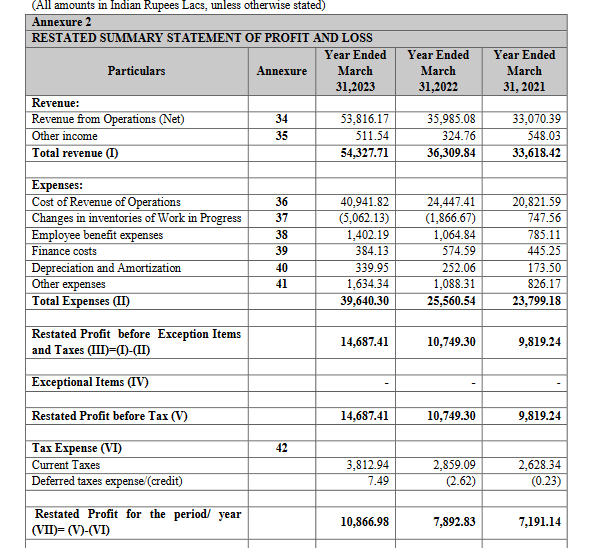

Annual revenues of EMS Ltd is 543cr. PAT 108cr.

Revenues increased at CAGR of 27% and PAT CAGR of 23% for the last 2 years.

76% of expenses is cost of purchase of goods for executing projects.

EBITDA margins 27.7%

PAT margins 20.2% ( VA Tech 4.4% FY 22)

ROCE at 28% ( VA Tech 19.4%)

Revenues/ PAT of bigger sized peer VA Tech Wabag is 2280cr/ 132cr (F22 taken as there is exceptional loss in FY23)

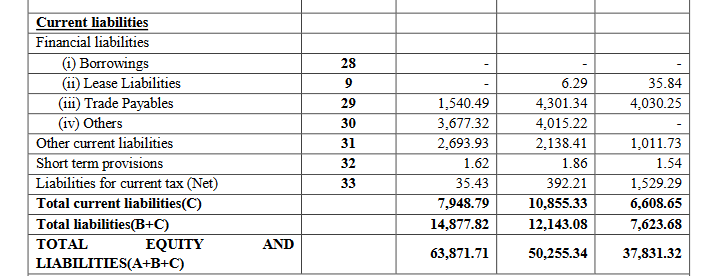

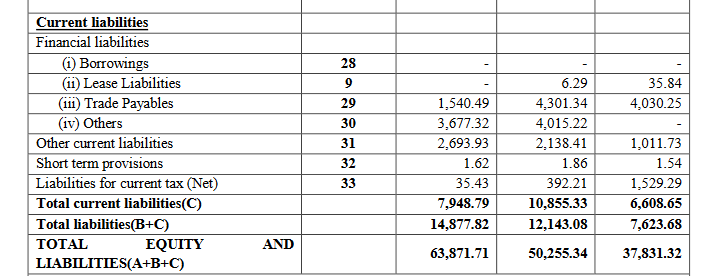

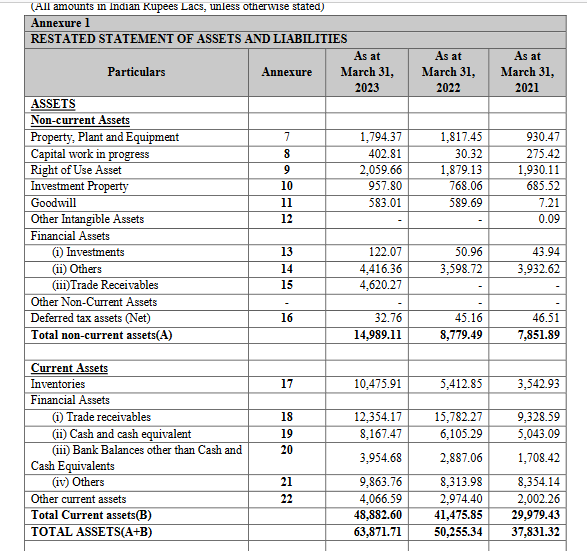

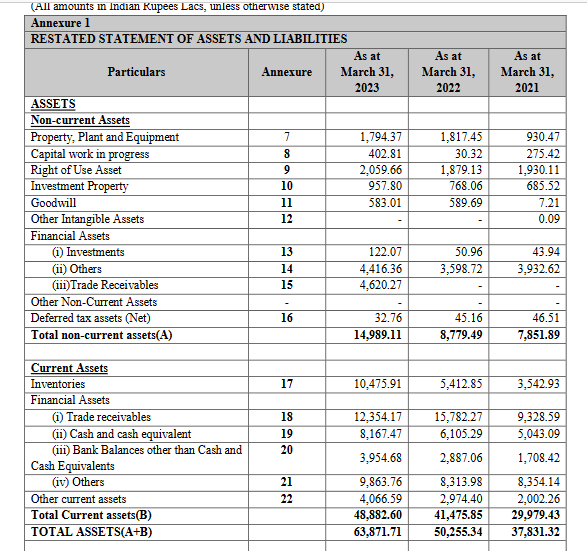

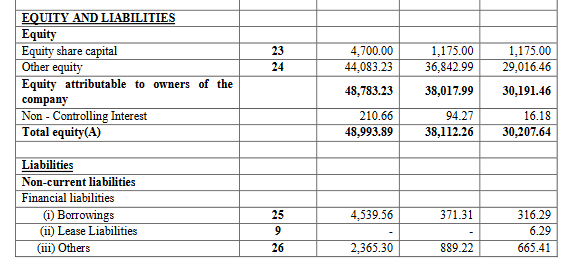

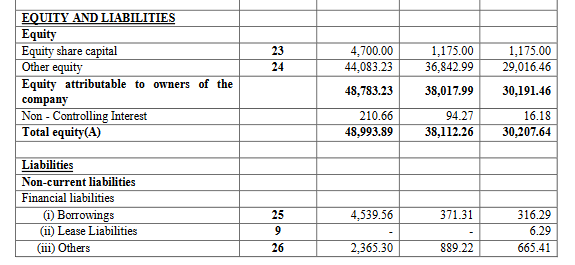

Balance sheet ( amount above in Rs lakhs)

Borrowing at 49cr

Current debt/ equity ratio at 0.09

Trade receivables 123cr (23% of revenues). It was 44% in FY 22, 28% in FY 21, indicating lumpy nature of payment cycle. Usual payment cycle is 90-120 days.

Cash equivalent of 82cr.

Cashflow from operations negative in FY 23, but was positive for previous 2 years.

Contingent liabilities of 252 cr is quite high.