Jupiter Life Line Hospitals Business analysis

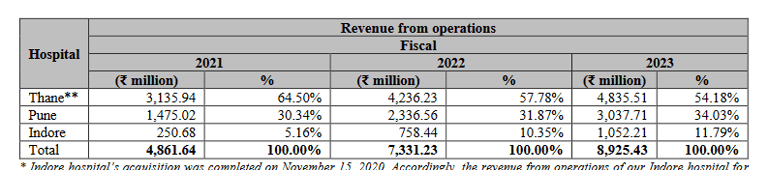

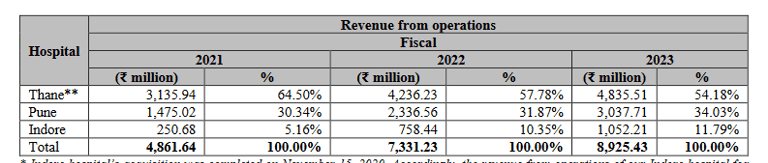

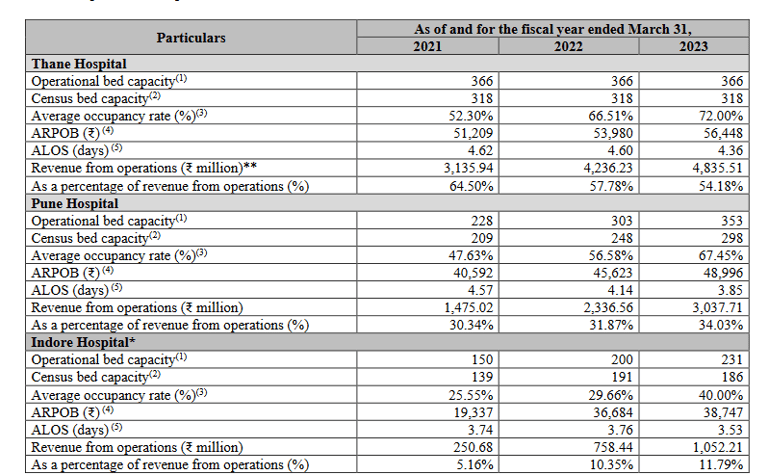

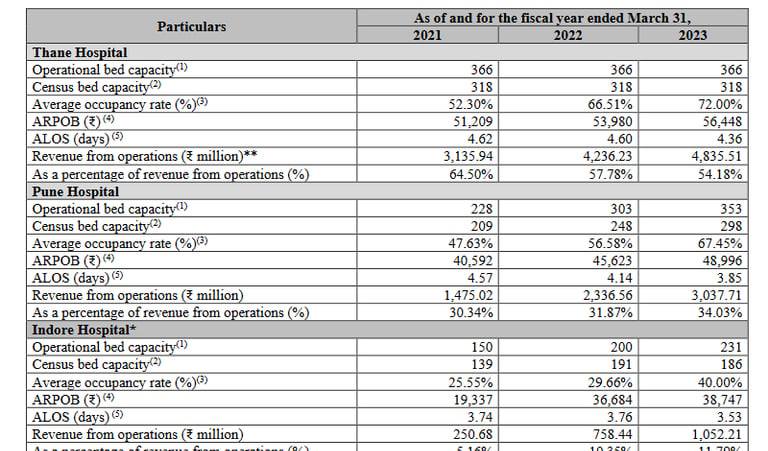

Indore hospital contributes 12% of revenues, with occupancy of 40%, and ARPOB of 39k. Lot of scope of growth exists from this hospital as it matures.

Occupancy rates of 2 mature hospitals > 65% indicates good demand and efficient operations of Jupiter.

Attrition rate of doctors ( in-house consultants) are less than 5%.

Revenues wrt Payor mix , with payments made through

1.self-payers 45%

2. Insurance/TPA 53%

3. Govt schemes 2%

Very low dependence of govt schemes patients ( vs peers) is a boost to revenues as govt schemes as govt schemes rates are usually revised after longer period of intervals and working capitals required is also less.

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

Jupiter Life Line Hospitals, started in 2002, by Dr Ajay Thakkar, is a multi-specialty hospital chain operating in Western India, with a total capacity of 1194 beds. They started with one hospital in Thane in 2007 to 3 hospitals now, completing 15 years of operations.

Dr Ajay Thakker is founder Chairman & MD , associated with the field of medicine for last 31 years.

Jupiter operates 3 hospitals in Thane, Pune and Indore with 950 operational beds, with a total of 1306 doctors. Thane hospital was the first one, set up in 2007, followed by Pune hospital in 2017, and Indore hospital was acquired in 2020. Land of all 3 hospitals are owned, not on lease.

They have started building a new multispeciality hospital of 550 beds capacity in Dombivli, Greater Mumbai in Apr '23.

Further to this, Jupiter seeks to expand to a total capacity of 2500 beds by establishing more new hospitals in near future.

Key specialties addressed are organ transplant, oncology, orthopaedics, cardiology, paediatrics, neurology and neurosurgery- a total of 30 specialties are treated.

According to CRISIL Report, their Thane and Indore hospitals are amongst the few hospitals in the western region of India to provide neuro-rehabilitation services through a dedicated robotic and computer-assisted neuro-rehabilitation centre. Additionally, our Company operates one of the few multi-organ transplant centres in Thane.

All 3 Jupiter hospitals have 3T MRI, 128 slice CT scanners, radiation therapy facility for cancer, cardiac cath labs.

Jupiter also focuses on academics and training, conducts courses and degrees including the DNB Post Graduate and DNB Super Specialty in various branches of medicine and surgery.

Industry overview

Healthcare delivery industry is estimated to be at Rs 5,70,000 crore in FY 23, slated to grow at 11.3% CAGR for next 4 years.

Healthcare private consumption expenditure is at Rs 4,13,500cr, grew at 8.6% CAGR for last 10 years. Healthcare expenditure of India as a % of GDP stands at 3% ( > 10% in US, EU).

Per capita healthcare spend of India is at $56, whereas for China, it is $583, for US, it is $11700. Out of pocket healthcare expenditure of India stands at 50.6% ( < 20% for developed countries)

Hospital beds/ 10000 population at India stands at very low 15 only ( China 43, US 29).

Physicians / 10000 population in India stands at 7 ( China 24 , US 36).

Nurses/ 10000 population in India stands at 17 ( China 33, US 15).

There is shortage of doctors, most critical resource of a hospital.

Disease profile has been shifting from communicable diseases to Non communicable (NCDs) or lifestyle diseases, which accounted for 66% of total deaths in 2019.

WHO projects an increasing trend in NCDs by 2030, following which CRISIL forecasts demand for services related to lifestyle-related diseases such as cardiac ailments, cancer and diabetes to rise. Another emerging market is orthopaedics.

West has higher insurance penetration and higher GDP/ capita. Also, percentage of govt. hospitals are lower in Maharashtra, and in Western India ( at 30% govt beds share, national average is 40%)

Jupiter Life Line is well placed to benefit from this.

The key players in western India include Aditya Birla Health , Ruby Hall , Sahyadri Hospitals and key pan-India players include Apollo, Fortis, Manipal.

Points to consider

Opening hospitals in the same cluster( Greater Mumbai- Thane, Dombivli ( upcoming), Pune) gives good brand recall in that area.

Availability of land bank in critical towns is an advantage for a hospital business as land constitutes major part of the capex cost. All hospitals of Jupiter are on owned land, including upcoming Dombivli one.

Improving occupancy and ARPOB at Indore hospital will drive growth in coming years. Dombivli hospital will contribute to growth after 3-4 years ( time to construct

Valuation

Jupiter Hospitals is valued at P/E of 66.

Most other bigger size hospitals trade at P/E of 40-50.

You may be interested in

Yatharth Hospitals IPO Analysis

How to do IPO analysis for listing gain

How to avoid bad companies like Brightcom/ BCG ? Investing red flags

Follow us on twitter

#themoatinvestor #dmoatinvestor #jupiterhospitalsipo #listinggain

Operating metrics

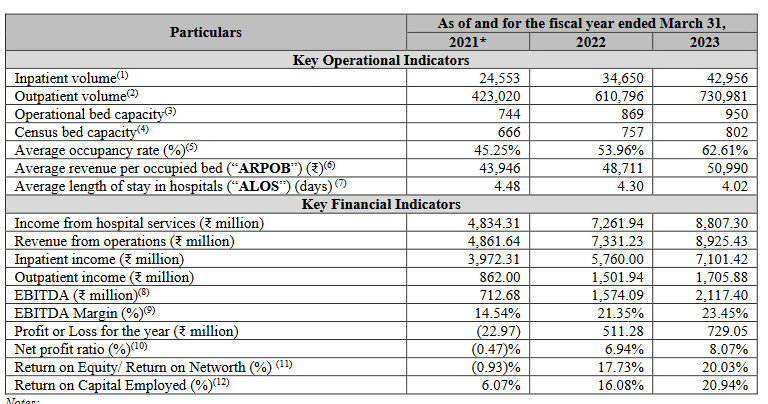

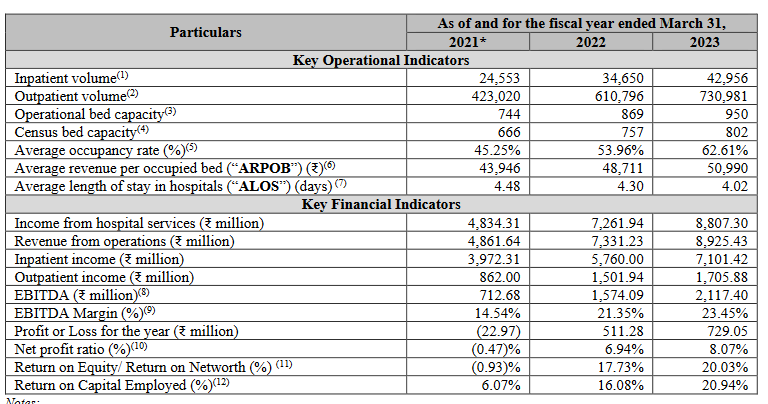

Total occupancy rates stand at 62% ( well operated large peers 65-70%).

Average revenue per operating bed (ARPOB) is at Rs 50990 ( most large peers >Rs 50k ).

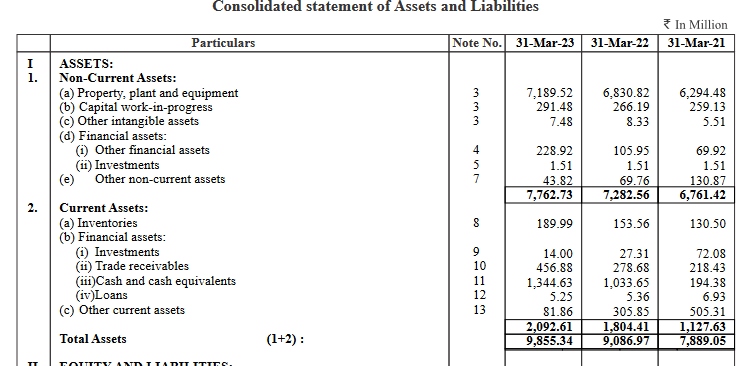

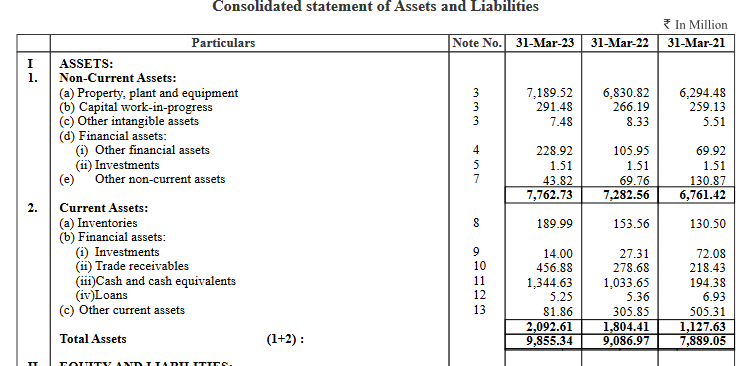

Financials

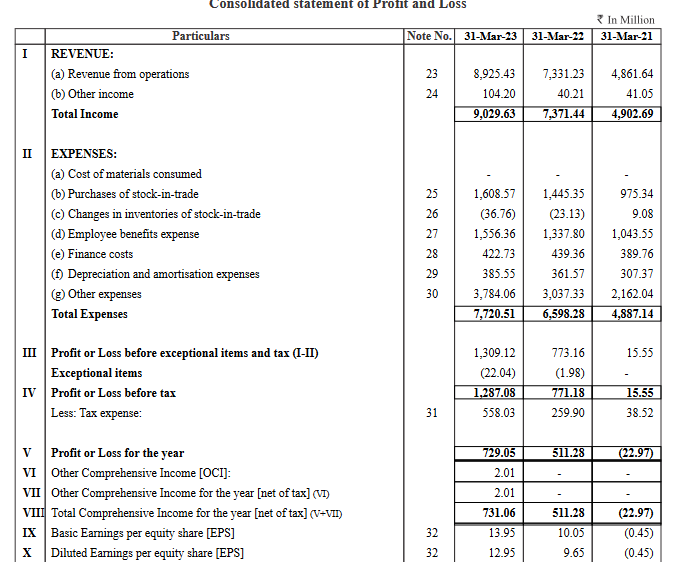

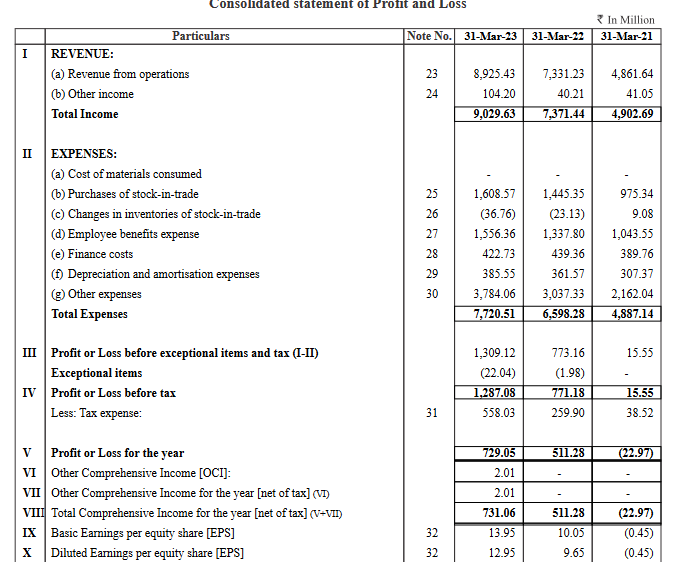

Annual revenues of Jupiter hospitals is 903cr. PAT 73cr.

Revenue from operations increased at CAGR of 35% for the last 2 years, driven by increase in occupancy rate in Indore hospital, increasing ARPOB at all hospitals.

Company has turned profitable from loss making in 2021.

Other expenses are appearing high as doctors salaries are included in this, not included in employees salaries.

EBITDA margins 23% which is among the better ones ( best hospitals have 25-27%)

PAT margins 8% can improve much if debt is reduced.

ROCE at 21% can improve further, but amongst the better ones.

Revenues/ EBITDA margin/ PAT margins of peers

Apollo ~ 16500cr / 12% / 5%

Max ~ 5900cr/ 27% / 22%

Narayana ~ 4500cr / 21% / 13%

Yatharth ~ 500cr/ 25.7% / 12.6%

Similar sized peer is Yatharth Hospitals ( 3 hospitals- 1400 beds).

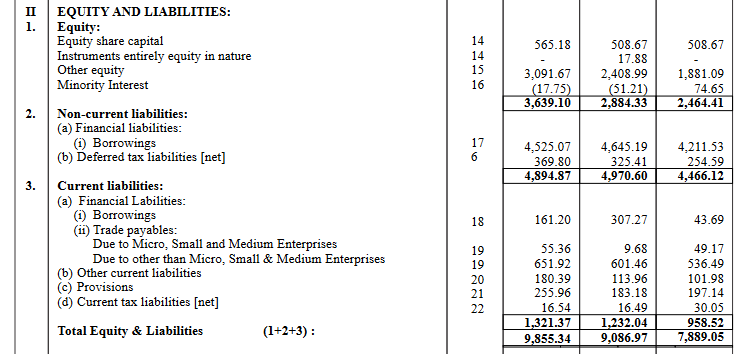

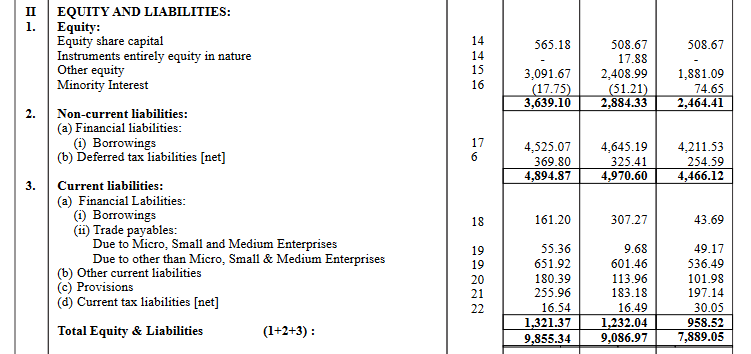

Balance sheet

Total debt 469cr ( entire debt will be paid off from IPO proceeds)

Current debt/ equity ratio at 1.29

Trade receivables negligible, since govt scheme contribution is almost nil.

Cash equivalent of 134cr.

Cashflow from operations positive for last 3 years.