Yatharth Hospitals Business Analysis

Contents

History of company

Industry overview

Geographical presence

Operating metrics

Financials

Future plans

Points to consider

Valuation

History of company

Yatharth hospitals started in 2008 as a clinic, developed into a hospital in Noida since 2010, and now has 3 hospitals, in Noida, Greater Noida and Noida extension , started by 2 doctors, Dr Ajay Kumar Tyagi and Dr Kapil Kumar, who are the 2 promoters of the company.

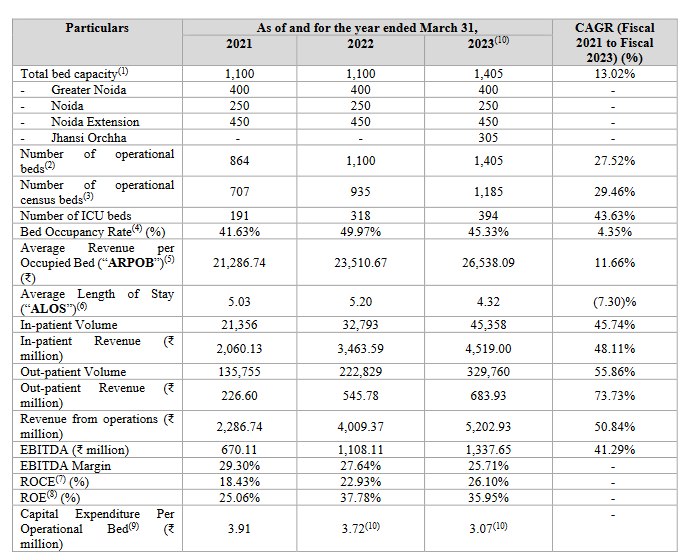

Total capacity of these 3 hospitals is 1100 beds. In April 2022, they have acquired a 300 bed hospital near Jhansi, UP, taking their total capacity to 1400 beds.Industry overview

Hospitals industry size is 5,70,000 cr.

Healthcare inflation has been increasing faster than the inflation in general, and in India, still 63% of the healthcare spends are out-of-pocket spends . But rising medical insurance penetration amongst urban customers, rise in lifestyle diseases, rising affordability of upper/middle class, and India emerging as an affordable medical tourism destination- all these combined projects the growth of healthcare industry at 11.3% CAGR .

More than half of the beds in India are private hospital beds.

Today, beds/ 10000 persons in India is 15, whereas in China, this is 43.

Tier 2/ Tier 3 towns are much more under penetrated.

Also, due to high quality treatment at costs much lower than other countries offering medical treatment, medical tourism sector is growing fast in India.

Delhi -NCR gets 40% of footfall of total medical tourists of India.Geographical presence

Yatharth mainly operates in Noida/ Noida extension area which has been a burgeoning with development in last few years. Neighbouring states of UP, Haryana naturally become their catchment area from where patients visit.Operating metrics

37% of revenues come from Govt employee tie-up schemes ( CGHS, state govt employee scheme) which usually has a fixed rates, lesser than market rates. Usually 15-20% is good mix.Bed occupancy rates are 45% ( low wrt industry standards (> 60-65 % is good) as new hospitals have low occupancy )

2 older hospitals have good occupancy rates, one that opened in 2022 at 31% , another acquired in 2023 is at 8%.

So growth will come from these 2 hospitals.Average revenues per operating bed (ARPOB) Rs 26000 ( low due to new hospitals having very low efficiency, Max, Apollo at Rs 55-60k, Narayana at 30k with high occupancy)

In patient volumes grown 26% YOY in 2 mature hospitals , which is good growth.

Revenues distributed from all categories, cardio,neuro, gastro etc . No specific segment contributing high indicating patients are not visiting for special reasons , like Narayana is known for cardio.

Current trend is big hospitals is targeting to develop 1 or 2 specialised branches of treatments ( like cardio, cancer care) as their forte according to their strengths and focussing on rebranding themselves in those lines to capture a niche in patient mindspace.They are using 1.5T MRI scan machines while some good hospitals use 3T. Other high end capabilities seems are there. Even doing organ transplants in Noida hospital and looking to start the same at Noida extension hospital.

Total 609 doctors ( 267 full time, 234 visiting docs, rest RMOs) .

Higher number of full time docs leads to higher efficiency since turnaround time decreases, utilization of doctors increase for hospitals who are already operating with high patient load and high occupancy. But increases fixed costs too.

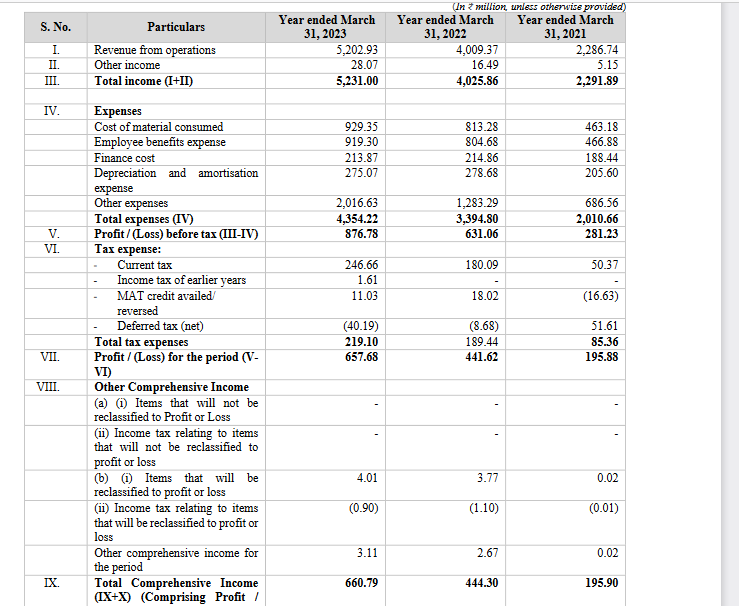

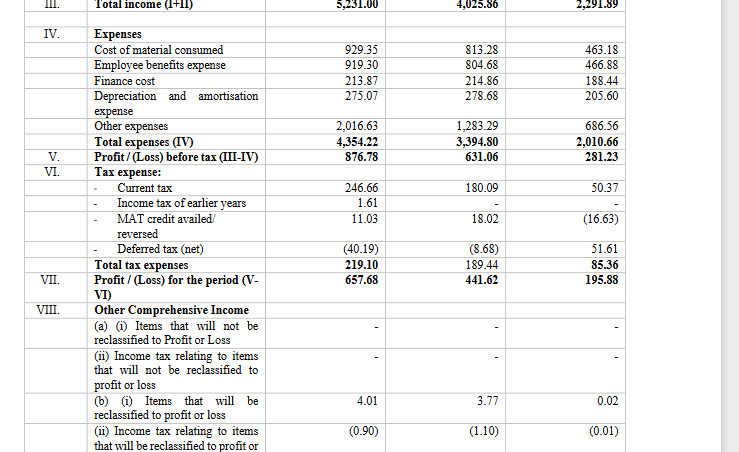

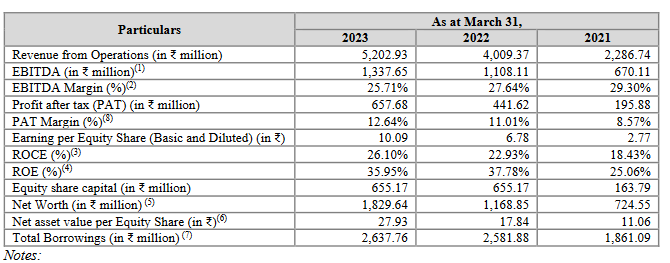

Financials

Competitors ( Revenue / EBITDA margin/ PAT Margin)

Apollo 16500cr / 12% / 5%

Max 5900cr/ 27% / 22%

Narayana 4500cr / 21% / 13%

Yatharth 500cr/ 25.7% / 12.6%

Margins are good.

Debt equity is 1.44 . ROCE at 26% and is increasing.

71% of revenues come from 2 older hospitals.

Future plans

In greater Noida , adjacent to existing hospital, they have acquired lease on one land, one more land under talks . They will expand capacity on these places. Plus, they are also looking at acquisitions through inorganic route.

2 hospitals in Noida area since long gives them brand recall in local area. Should give advantage to the newly opened Noida extension hospital to achieve better occupancy rates.

They intend to extend and develop Oncology segment at all the hospitals, and extend organ transplant at Noida extension hospital.

They also intend to develop Medical tourism segment, given the strategic affordability advantage of Indian hospitals amongst other countries ( since they are located near the Noida airport and Delhi-NCR sees the most footfalls in the country for Medical tourism)

Points to consider

New hospital near Jhansi border being away from their core operation area, and being located in the rural area , it may take time to increase the occupancy rates ( 8% now).

Availability of land bank for future expansions is a critical resource of a hospital, which is available to Yatharth.Valuation

Other hospitals trade at 40-50. Apollo trades at 80.

Listing price is 285-300. Listing PE is 40.

#yatharthhospitalsipo #themoatinvestor #stockanalysis #DMoatInvestor