Vishnu Prakash R Punglia Business analysis

Business

Vishnu Prakash R Punglia, started in 1986, is an engineering, procurement and construction(EPC) company is based out of Rajasthan and involved in design and execution of infrastructure projects of government & private players.Under EPC, they undertake engineering design of the project, procurement of key raw materials, execution of the project, project management and finally commissioning of these projects. If contract permits, they also do O & M (Operation and maintenance)

They undertake 4 types of projects primarily

1. Water supply projects

2.Railway projects

3. Road projects

4. Irrigation network projects

They are class AA contractors with several govt. departments in different state govts like health, water resources, PWD departments etc.

Vishnu Prakash's works across 9 states of India ,across West and North, and North east also, though majority of projects are in Rajasthan.

Water supply projects entail supply, laying & testing of pipelines, construction of water tanks, reservoirs, overhead tanks, raw water reservoirs, water treatment plants, pumping stations, providing functional house hold tap connections.

Railway works include laying of railway tracks, construction of platforms, major bridges, rail-over-bridges, rail-under-bridges, foot-over-bridges, station buildings, staff quarters, signals.

Road projects include construction of roads, highways on EPC mode, including bridges, culverts.

Irrigation projects include EPC of irrigation network including construction of tunnels, canals, construction of sewerage treatment plants, sewerage pipelines, sewer tank, drains.

Equipment and commercial vehicles required for executing work are owned by the company, and they operated in integrated model with in-house design, procurement, project, engineering, quality teams.

Some of the projects are operated under JV with other companies.

Industry overviewInfra development is one of the key drivers of a developing economy. In budget 2023, govt. increased allocation to infra budget by 33% YOY to Rs 10 lakh crore ( 3x the budget of 2019). Govt. has launched National Infra Pipeline ( NIP) , PLI scheme to boost infra developments. Financial assistance of Rs1,30,000cr interest free loans for 50 years has been allocated to states for infra push.

Water supply

India is home to 18% of world's population and 4% of fresh water reserves. In 2022, 17% of households are reported to have access to tap water connections. Govt. has launched Jal Jeevan Mission to bridge this gap, with total project outlay of Rs 3,60,000cr. FY 24 budgetary allocation is Rs 70000cr.

Waste water treatment is another scope of work. 72% of waste water is left untreated currently. Govt is pushing for waste water treatment, agricultural water re-use, industrial water re-use, River Ganga treatment.

Rail infra

The Government has proposed a 70% YOY increase in budgetary allocation of Rs 2,40,000 to Railways in Budget FY 24. Govt is aiming for 45% share of rail in freight transport by 2030 ( current 27%), for that they are initiating different projects under PPP model. Govt. is looking for 100% electrification of railways and introducing automation across operations.

Road Infra

In budget FY24, Govt allocated Rs 2,70,000 towards road construction ( Rs1,99,000cr in FY23).

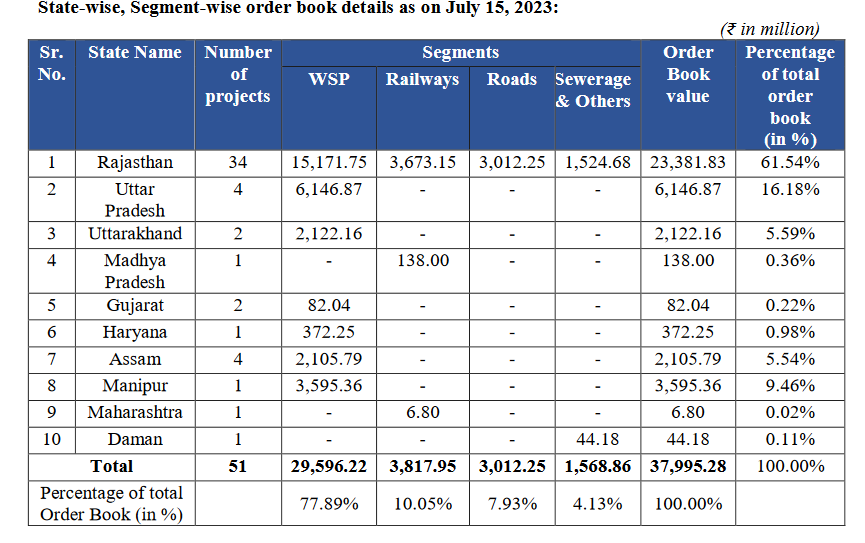

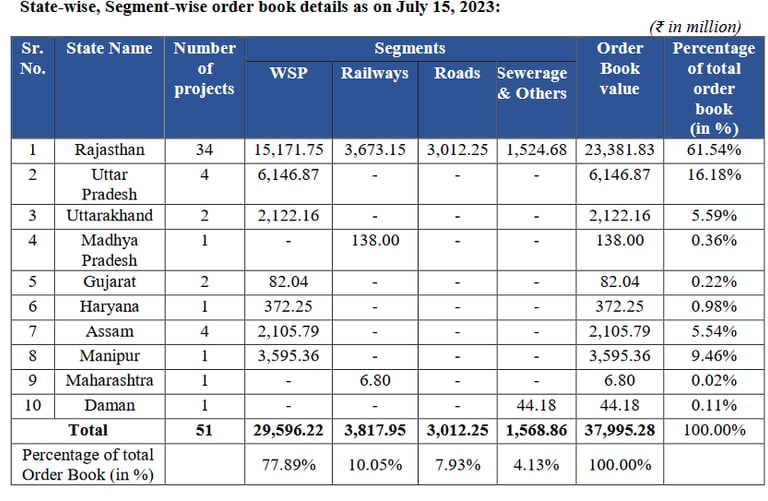

Order book

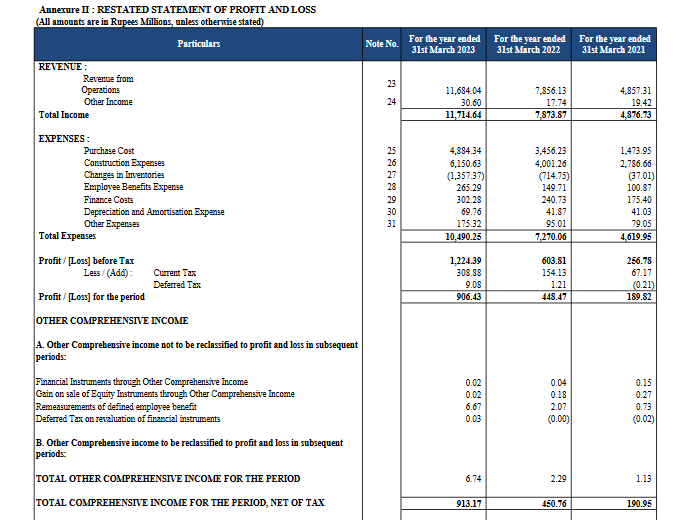

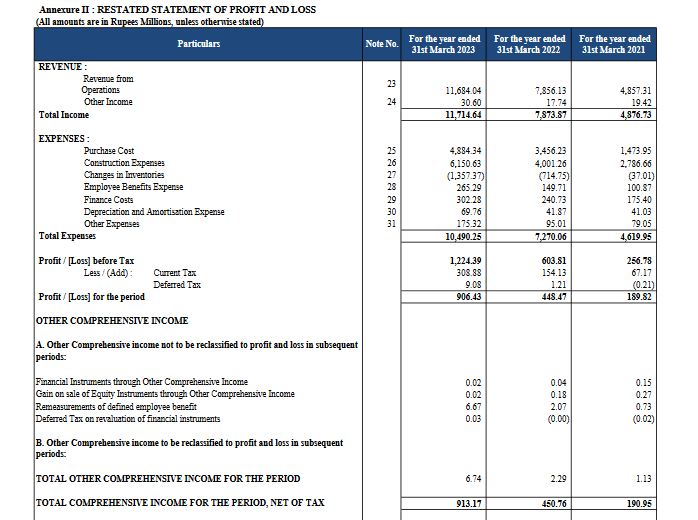

Annual revenues of Vishnu Prakash is 1170cr. PAT 90cr.

67% of revenue came from Rajasthan projects.

Revenue from operations increased at CAGR of 55%, PAT increased at CAGR of 118% from FY 21 to FY 23.

Profits have become 5X in last 2 years.

EBITDA margins expanded from 9.7% to13.5% in 2 years. ( peers PNC Infra, HG Infra at 19-21%, NCC , RVNL at 10%)

PAT margins have expanded from 3.9% to 7.7%

ROCE at healthy 33%, increased a lot in 2 years.

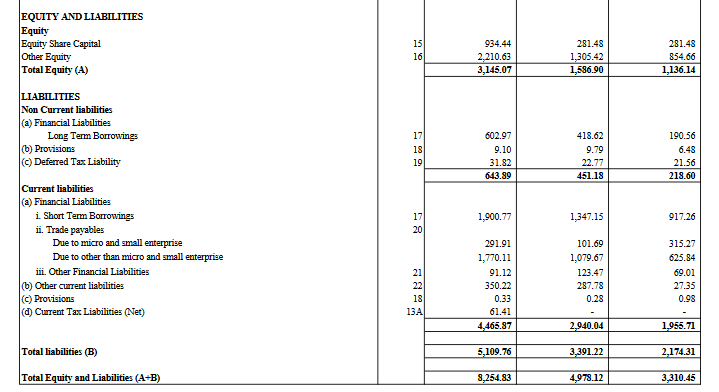

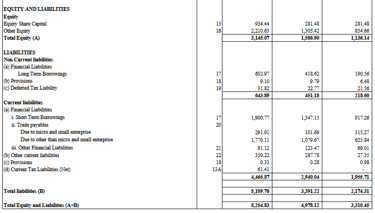

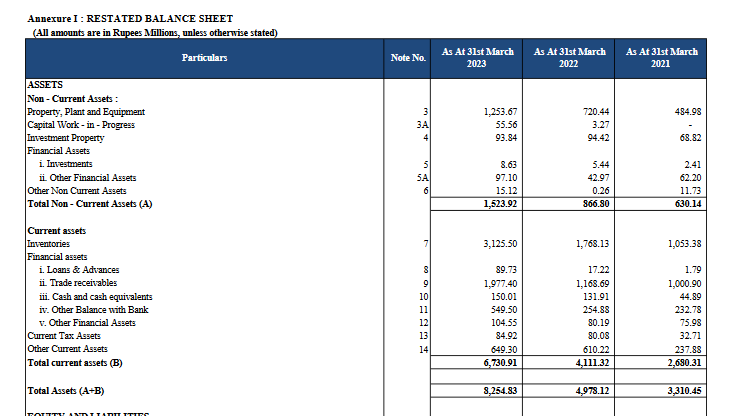

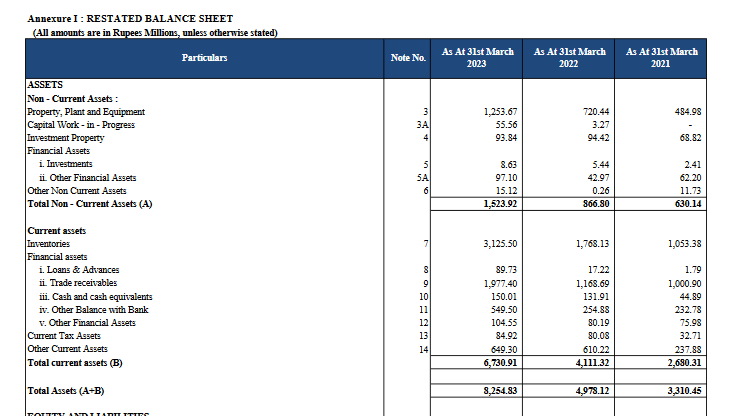

Balance sheet

Trade receivables 197 cr ,low considering it is a B2B business mostly with govt parties.

Cash/ bank balance is 70cr

Total borrowings 250 cr

Debt equity ratio 0.8 ( most peers operate at similar or higher debt)

Cashflow from operations (CFO) negative.

Contingent liabilities 277cr.

Points to consider

Vishnu Prakash has 36 years of experience in Water supply projects, which is their core area of focus. (78% of order book)

Robust order book of 3800cr ( more than 3x of current revenues) is a big plus.

In-house integration model and relations with govt departments through years of project execution is an advantage.

Geographical concentration in Rajasthan and UP is a risk ( 77% of order book). 67% of FY 23 revenues came from Rajasthan projects.

Also there is significant client concentration risk with 81% revenues coming from top 5 clients.

Cashflow from operations being negative, and business being high working capital intensive ( which may increase anytime if any big payment is further delayed), they will need to raise further money for working capital if revenue has to grown so steeply ( IPO proceeds of 150cr will be utilized for this)

Valuation

Vishnu Prakash R Punglia is valued at P/E of 13 ( bigger peers PNC Infra, HG Infra, NCC valued between 13-16, while RVNL at 18, ITD Cementation at 25)

To read more on how to predict listing gains

How to do IPO analysis for listing gain

Aeroflex Industries IPO Analysis

#themoatinvestor #dmoatinvestor #vishnuprakashrpungliaipo

Total order book stands at 3880cr (July '23) ( Annual Revenues 1170cr)

77% of order book is from Rajasthan (61%) and UP, so there is geographical concentration of 2 states.

81% revenues generated from top 5 clients, so there is very high client concentration.

Financials