RR Kabel Business analysis

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

RR Kabel, started in 1999 , by Shreegopal Rameshwarlal Kabra , based out of Vadodara , is one of the leading players in consumer electricals and FMEG ( fast moving electrical goods). RR Kabel is 5th largest player in wires & cables with a market share of 5%. RR Kabel was one of the leading exporters in FY22, with 9% export market share in wires & cables exported.

RR Kabel operates under 3 brands-

RR Kabel ( wires & cables) ( 20 years old)

RR ( consumer electricals like fan, lights)

Luminous ( fans, lights)

Product segments

1. Wires and cables

House wires- used in residential, commercial wires used for internal wiring

Industrial wires - used in control panels, industries , production lines

Power cables - used in power transmission and distribution

Specialty cables - used in solar, automotive, instrumentation, data centre etc.

2.FMEG

Fans

Lighting

Switchgear - modular switches, MCB, distribution box

Electrical appliances - Room heater, iron, water heater, air cooler

RR Kabel has 2 plants for wires & cables- Gujarat ( Waghodia) and Silvassa ( Daman), 3 plants for FMEG goods - Roorkee, Bangalore, Himachal (Gagret). 37% of FMEG goods are manufactured in-house. 100% of wires & cables manufactured in-house.

RR Kabel has 3,450 distributors, 3,656 dealers and 114,851 retailers.

In FY 20, RR Kabel acquired lighting business of Arraystorm Lighting. In 2022, they acquired home electrical busines of Luminous.

RR Kabel products are exported to 63 countries in North America, APAC, Europe and Middle East, major contributors UAE and UK.

Industry overview

Consumer electrical industry is Rs 1,81,150 cr in FY 23 , expected to grow at CAGR of 10% for next 4 years, out of which, domestic market for wires & cables industry is Rs 74,800cr, expected to grow at a CAGR of 13%.

Wires & cable (41% of industry)

In wires & cables, industry is shifting from unorganized to organized players due to priority to safety and awareness, GST and continuous spend on brand building by top branded players.

Growth drivers

Rural electrification driving increase in per capita consumption of electricity in India, green energy shift, real estate sector boosted by govt housing schemes and recovery of real estate demand.

Per capita consumption of electricity in India is 1255KWhr ( China 4300, US 13000)

FMEG Industry (59% of industry)

In FY23, FMEG industry is at Rs 1,06,350cr, projected CAGR of 8% for next 5 years.

Fans industry at Rs 13900 ( projected 7% CAGR)

Lighting market in India is estimated at Rs 33,600cr (projected 11% CAGR)

Switch and switchgear market is Rs 29160 cr (projected 7% CAGR)

Organized players control 72% of wires & cables industry, with leading players being Polycab, KEI Industries, Havells, Finolex, all listed apart from RR Kabel.

Points to consider

RR Kabel is 5th largest player in wires/ cables, with export revenues growing very fast (43% CAGR 2 year) and company increasing retail touchpoint reach by 3.5X in last 2 years.

Margins of RR Kabel are much lower than peers, despite predominantly being a B2C player,affected by the FMEG business.

Company has shown very good Q1 FY 24 results ( Q1 FY24 PAT 74cr vs Q1 FY 23 PAT of 18cr. PAT became 4x YOY)

Wires & cables business is subject to sharp fluctuations in Copper and Aluminium prices , as it takes some time to pass on the cost inflation to customers, so margins take a hit for some quarters.

Fresh issue is only 180cr ( out of total issue 1964cr), and company does not receive any proceedings of OFS. PE fund TPG capital is offloading 70% of its stake in OFS.

Valuation

RR Kabel is valued at P/E of 61 ( wrt FY23 PAT) and at P/E of 39 wrt F24 Q1 PAT annualized basis (Q1 PAT may not be replicated for the rest 3 quarters)

Comparable peers Polycab P/E at 50, KEI 46, Finolex 30, all of them trading at their peak PE ratio.

You may be interested in

How to do IPO analysis for listing gain

How to avoid companies like Brightcom/ BCG ? Investing red flags

Will Jio Financial disrupt Bajaj Finance

Zaggle Prepaid IPO Analysis

Follow us on twitter

#themoatinvestor #dmoatinvestor #rrkabelipo #listinggain

Operating metrics

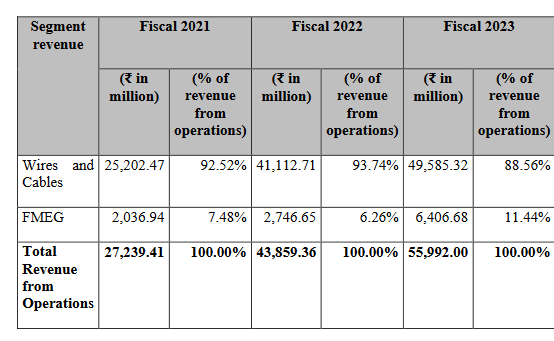

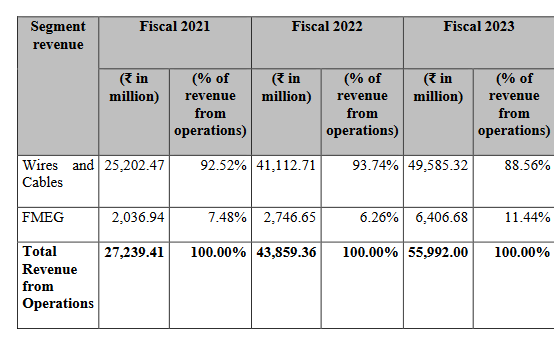

89% of revenues are from Wires & Cables, rest 11% FMEG ( this used to be 7% 2 years back). FMEG revenues have more than tripled in 2 years.

74% of revenues is retail (B2C), which is higher margin business.

Exports form 23% of revenues, with UAE & UK being top contributors, rest 77% from domestic.

RR Kabel has highest export revenues (1270cr) among peers, after Polycab. (1380cr)

RR Kabel has increased its network of electricians very fast ( 3.5 times in 2 years) in last 2 years. Current network stands at 2,71,264 electricians. Total retailer outlets are 1,06,626 ( Polycab 205000), 3450 distributors.

RR Kabel spends 60% of total ad budget (85cr FY 23 at 1.5% of revenues, lower than peers) on BTL activities, mostly for electrician engagement programs like Kabel Mela, Kabel Nukkad etc.

Rest 40% mainly goes in sports sponsorships like peers, IPL team KKR sponsor, and Pro Kabbadi League sponsor.

Future focus of company is to add high margin value added products in FMEG, grow distribution reach further, and expand product portfolio.

RR Kabel has >9% market share in 12 states. (overall market share 5%)

Financials

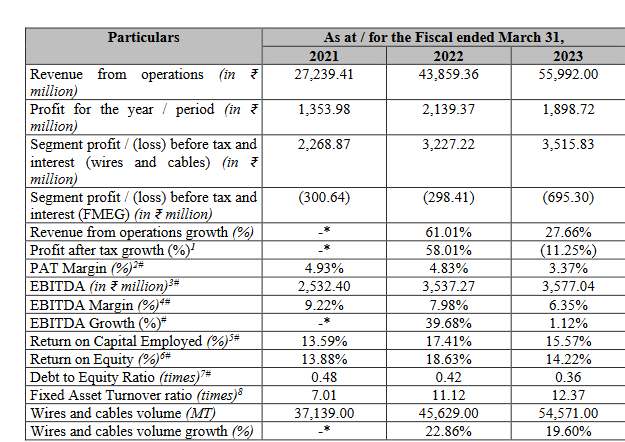

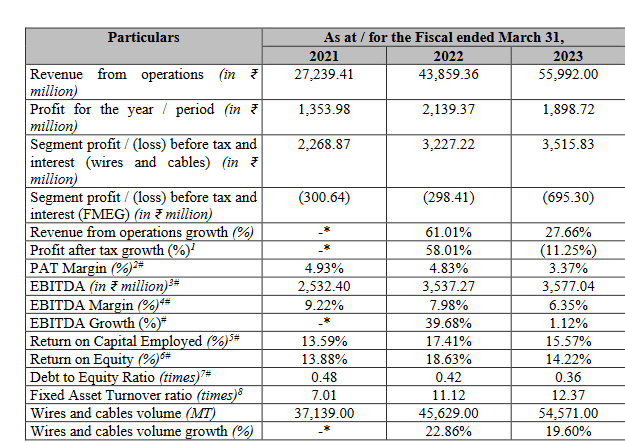

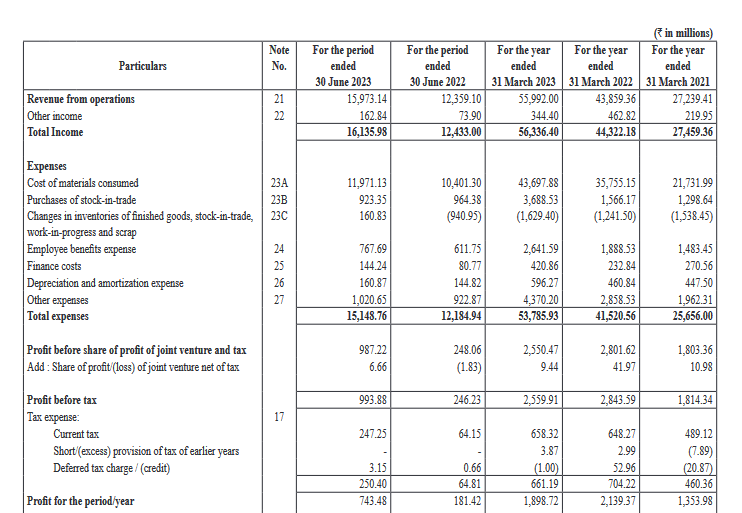

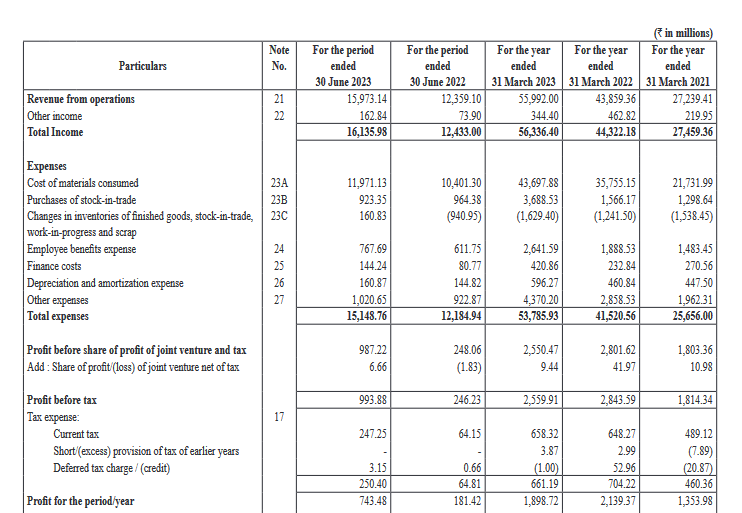

Annual revenues of RR Kabel is 5600cr. PAT 190cr.

Revenues increased at CAGR of 43% and PAT CAGR of 18% for the last 2 years. Profit growth less due to FMEG segment is in losses ( 69cr EBIT loss in F23, was 30cr in FY21), which is natural for new segment business until it achieves a certain scale.

84% of revenues is raw material cost, main raw materials being Copper, Aluminium, Galvanized Iron.

EBITDA margins 6.3%

PAT margins 3.7%

Margins are much lower than peers.

ROCE at 15.6%

Comparable peer in terms of revenue mix are Polycab, KEI. ( 87-91% revenues from wires /cables). Revenues taken are total revenues.

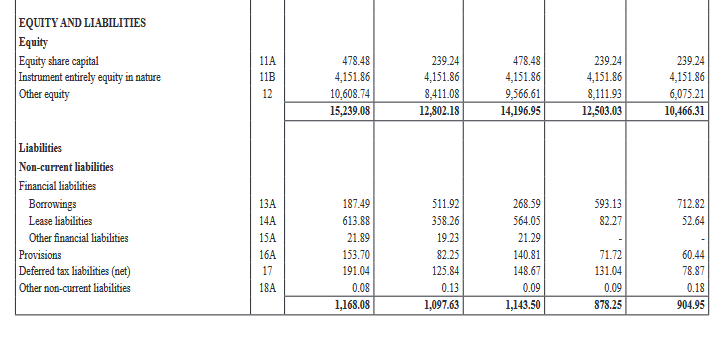

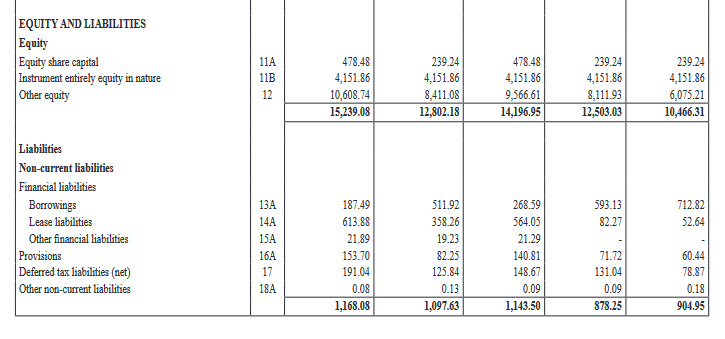

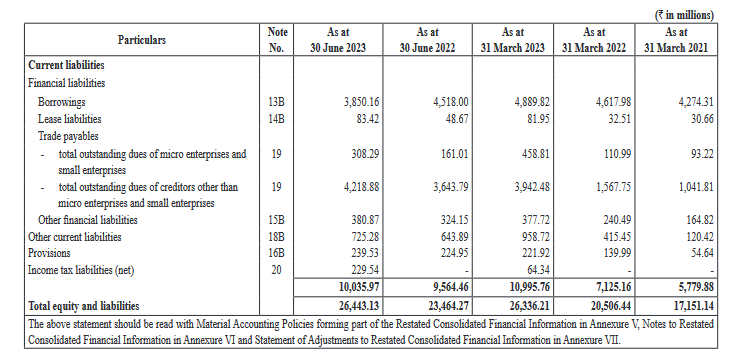

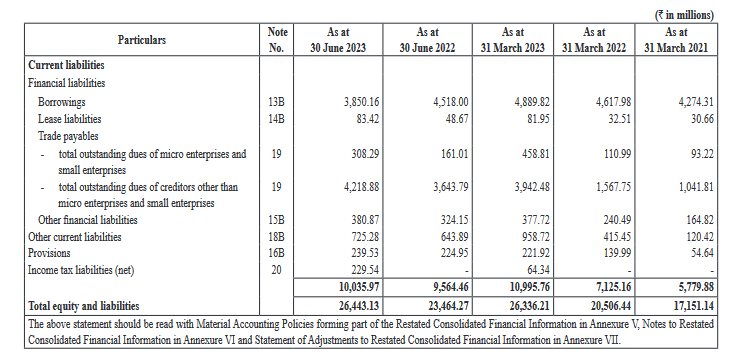

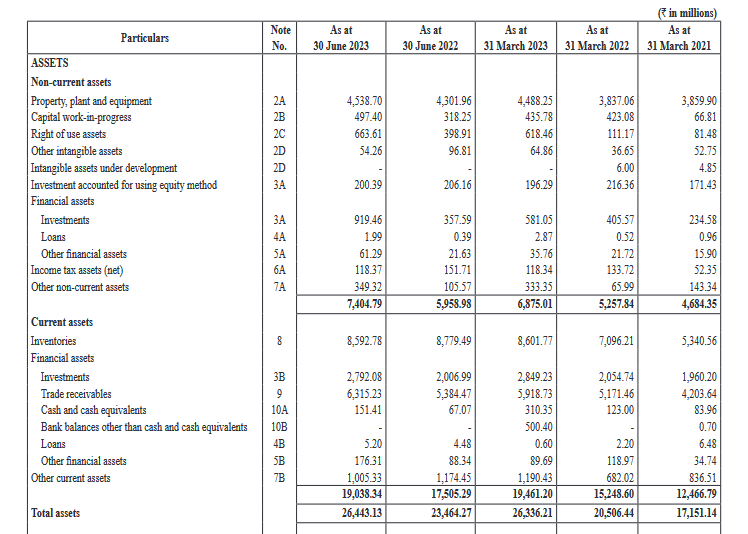

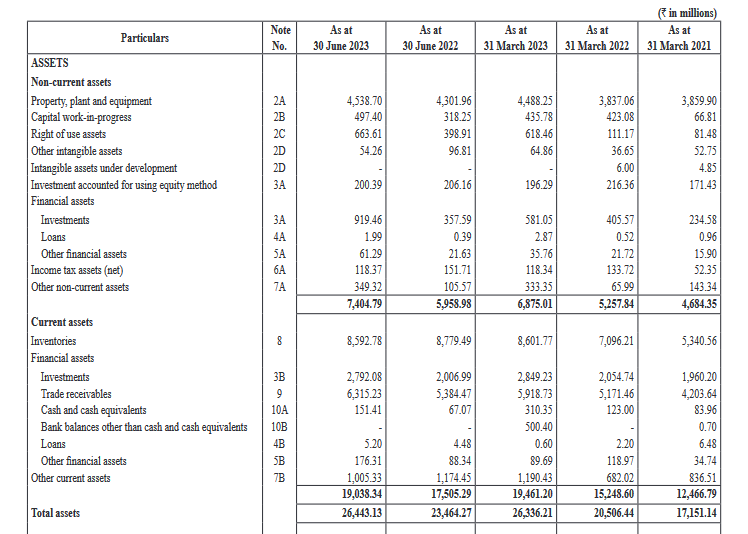

Balance sheet ( amount above in Rs millions)

Borrowing at 516cr ( mostly short term loans). 136 cr of IPO proceeds will go towards debt reduction.

Current debt/ equity ratio at 0.36.

RR Kabel operates with inventory of around 1010cr

Trade receivables 592 cr.

Cash equivalent of 81cr.

Cashflow from operations positive.