India Shelter Finance Business Analysis

Operating metrics

Loan book composition as on FY24- Sep'23

Home loans 58%

LAP 42%

Total AUM 5180cr

Loan to value for housing loans 55% , LAP 45%

Borrowing mix

Term loans 68% ( 57% banks)

NHB 18%

NCD 3%

Securitization 2%

ECB 8%

Care rating A+ ( as of Sep, '23)

They follow a phygitail model- physical onboarding of customers through a network of more than 1,500 relationship managers , coupled with use of digital tools.

India Shelter Finance follows an in-house origination model ( 97% of loans in-house sourcing) - sourcing, underwriting, valuation, collections and customer service, reducing turnaround times and transaction costs.

India Shelter Finance captures 100 data points through different front end app for customer sourcing, disbursement, underwriting, collections- which helps them improve efficiency , improve credit analytics, risk analytics , fraud analytics.

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

India Shelter Finance , started in 1998, was acquired by current promoter Anil Mehta in 2009. Majority stake owned by WestBridge Crossover Fund , Aravali Investment Holdings and Nexus fund. Target segment is the self-employed customer with a focus on first time borrowers ( 94% of total loans) in the low and middle income group in Tier II /III cities , with ticket size < 25 lakhs. All loans given to retail customers.

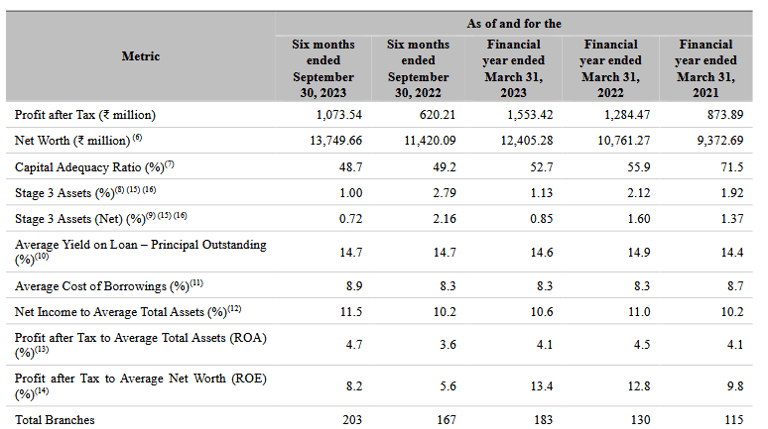

The operate through 203 branches spread across 15 states, based out of Gurgaon.

Total Asset under management ( AUM) 5180cr, 90% of which is from Tier 2/3 towns.

2 year AUM CAGR of 42%.

Home loans account for 58% of AUM, while loans against property 42.4%

Average ticket size 10.3 lakhs. Average Loan-to-Value is 51%.

Focus customers are self-construction/ purchase of residential properties by first-time home loan borrowers. 71% of customers were first-time borrowers.

Total branches 203 ( was 115 in Mar '23)

Branches ( major states)

Rajasthan 62

Maharashtra 30

MP 25

Gujarat 17

UP 16

Tamil Nadu 12

Top 3 states constitute 62% of AUM .

Industry overview

The Indian housing finance market grew at 13.5% CAGR in last 4 years on account of rise in disposable incomes, healthy demand, more players entering the segment. Since 4 years, affordability increased owing to steady property rates and increasing income. The total housing finance segment credit outstanding is Rs 31.1 trillion as of March 2023. The top 50 districts in the country accounted for 63% of the housing loan outstanding in the country in FY23 ( 73% in FY19), implying more housing loans are being distributed outside top 50 districts. India Shelter Finance Corporation is present in market which account for 44% of overall housing loans market. Housing loan market is projected to grow at 13-15% for next 3 years.

Region wise Distribution of housing loan market

South 36%

West 31%

North 15%

Central 11%

East 6%

NE 1%

Top 5 housing finance markets

Maharastra 23%

Karnataka 10%

Tamil nadu 9%

Gujarat 8%

Telengana 8%

Share of housing loans

PSU Banks 40%

HFCs 34%

Private Banks 20%

NBFCs 2%

Others 4%

Affordable housing finance

Affordable housing ( < Rs 25 lakhs ticket size) market is 37% of total housing loan market, projected to grow at 15-16% for coming 3 years as per CRISIL. Market share of PSU banks in affordable housing finance is 42%, HFCs is 36%, Private banks 14%. Since PSU banks mostly target salaried classes ( including NBFCs like Can Fin Homes, PNB Housing), non-salaried Tier III and rural market are catered by HFCs / NBFCs given most NBFCs have deep presence in few states, rather than scattered presence in all states.

South (31%) and West (30%) forms 61% of the market. Top 5 states Maharastra ( 19%) , Gujarat (11%), Tamil nadu (9%),UP(7%), Karnataka (6%) forms 52% of the market.

Share - Region wise

Rural 28%

Semi-urban 13.5%

Urban 58.5% ( was 62.8% in FY19)

Demand drivers

1. Rise in disposable income- India’s per capita income grew at a 10% CAGR between FY12-20,which will aid housing finance demand.

2. Increasing Urbanization ( 31% in 2011, 35% in 2021, 39-40% in 2031)

3. Govt initiatives- PM Aavas Yojana, Relaation of ECB norms for easier access to credit, increase in PSL threshold.

Top affordable housing finance companies are Aavas Financiers, Aptus Value Housing, Homefirst.

Financials

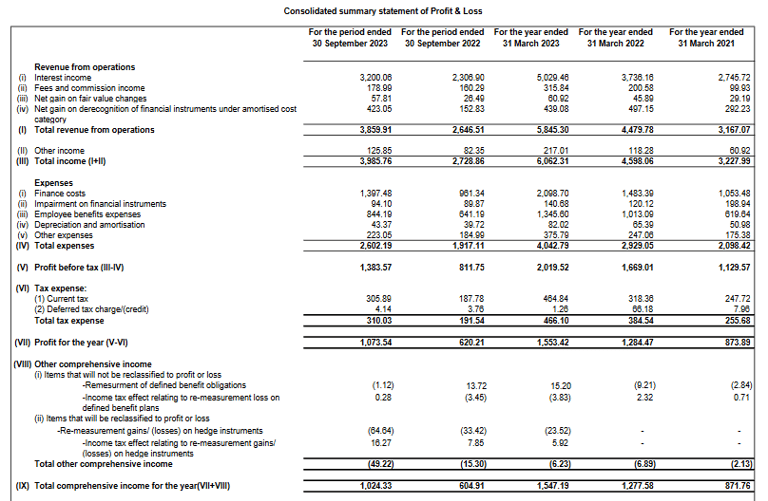

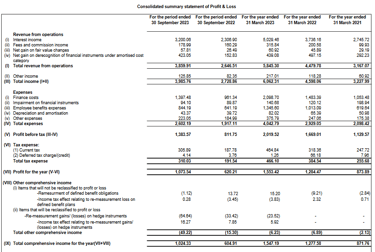

Total FY23 revenues of 580cr .( Revenue CAGR 2 years 34%).

PAT 150cr

Impairments 14cr.

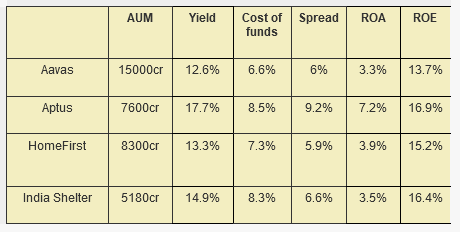

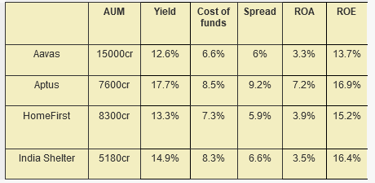

Comparable peer is Aavas and Home First.

Gross NPA is 1% in FY23 ( peers Aavas 1.74% Homefirst 1.74%)

NNPA 0.72% ( peers Aavas 0.76%, Homefirst 1.22%)

Financial ratios ( FY23)

Credit cost 0.4% ( Homefirst 0.4%, Aavas 0.1%)

CRAR 48.7% ( Tier-1 47.9%)

Gross stage 3 assets 1%

Net Stage 3 assets 0.72%

Rest as per table below.

Spreads are similar to peers.

ROA 3.5% ( Aavas 3.3%, Homefirst 3.9%)

Points to consider

Bigger HFCs are focussed on salaried customers in tier 1 cities, AHFCs ( Affordable housing finance cos) like India Shelter Finance are focussed on self employed customers who don't have proper income records ( ITRs), and in tier2/3 towns, rural .

AHFCs has higher NIMs of 5.5%-6% wrt bigger peers, owing to catering of riskier customer profile

Each AHFC have concentrated operations mostly in 2-4 states, with operations in core markets of 10 years, through which they have deep understanding of the market. India Shelter have similar advantages- but top state being Rajasthan, clashes with forte of Aavas Financiers.

Top 3 states constitute 62% of AUM, top 5 states 76% of AUM, similar to Homefirst. ( Aptus has much higher concentration risk)

Most loans are sourced in-house , and phygitail model of credit underwriting- leading to better risk management practice.

Almost half ( 98) of 203 branches have been added in last 2 years, so full realization will happen over 2-3 years.

Valuation

India Shelter Finance is valued at Price/ Book ratio 2.43

Peers Aavas Financiers at P/B 3.5 , Homefirst at 4.6 , Aptus at 4.6

Follow us on twitter

You may be interested in

Fedbank Financial Services analysis

Utkarsh Small Finance Bank analysis

SBFC Finance analysis

Will Jio Financial disrupt Bajaj Finance

#themoatinvestor #dmoatinvestor #indiashelterfinanceipo #listinggain