Fedbank Financial Services Business Analysis

Operating metrics

Loan book composition as on FY24 (Q1)

Gold 33%

Medium ticket LAP+Housing 25%

Small ticket LAP+Housing 24.5%

Unsecured business loans 16%

Total AUM 19430cr

86% of loanbook is secured

80% of borrowing is from banks.

They follow a phygitail model for collections. Doorstep gold loans ( currently a norm in NBFC industry) helps de-leveraging branch network. Fedbank has partnered with 1796 channel partners to complement 584 branches to deepen their reach.

Fedbank has been rated as Great Places to Work for last 3 years by Great Places to Work institute.

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

Valuation

Business

Fedbank Financial Services , promoted by Federal Bank is a focused retail loan NBFC (securitized) targeting self-employed individuals and the emerging MSME sector.

The operate through 584 branches spread across 17 states, based out of Mumbai.

Total Asset under management ( AUM) 9430cr, 71% of which is from rural/ semi-urban towns. 3 year AUM CAGR of 33%

86% of AUM are secured against gold or property.

Average ticket size 1.3 lakhs. Average Loan-to-Value is 51%.

Though they focus on the underserved category of retail loan , 87% of customers have an established credit history, 78% of them have CIBIL>650

Total branches 584

Branches ( major states)

Maharashtra 107

Gujarat 92

Tamil Nadu 77

Andhra 57

Telengana 49

Delhi NCR 38

Top 5 states constitute 78% of AUM of banking outlets in rural/ semi-urban areas.

Products

1.Gold loans

3.2 lakh gold loan accounts. 279 gold loan branch, 13 door step hubs

- doorstep appraisal

- instant disbursal at our customers’ premises before transferring the pledged gold to a nearby branch with in-transit security which includes an electronic safe with GPS for tracking.

- multi-tier authentication, online portal and mobile applications for real-time tracking

2.Small ticket LAP and housing loans

- self-employed customers with shops/ small busiess

- salaried customers with a medium income

- periphery of Tier 1 cities/Tier 2/ Tier 3 cities

- median income of Rs 5 lakh/ year

- irregular or minimal record of financial transactions but a healthy household cash flow and asset holdings, and property.

3.Medium ticket LAP

- MSMEs- including traders, wholesalers, distributors, retailers, self- employed professionals and small manufacturing companies.

- purpose - capital infusion,expansion of businesses, working capital, capital expenditure. Collateral- self- occupied residential and commercial properties

4.Unsecured business loans

- self-employed professionals and non-professionals, and salaried doctors.

- target customer segment- turnover of 1 cr per year and a minimum of five years of business experience in their current business

- provides funds to bridge working capital and business expansion

without requiring any collateral.

- underwriting through assessment of the financials, cash flows, GST and turnover

Digitization and analytics

Fed Fina spent 25cr in tech in last 3 years. They are able to capture significant amounts of data points through credit bureau data, API stack enabling independent validation from source, customer financials, observations from front-end team, and feedback from credit underwriting and management teams. 43% of customer transactions are digital.

Industry overview

Rural areas, which account for 47% of GDP, received just 8% of the overall banking credit. With advent of smartphones, UPI led digital trails, payment banks, flipkart/amazon online shopping, microfinance institutions- focus on rural credit is supposed to increase further. Currently, semi-urban ( tier 2/3) forms 13% and rural forms 8% of total credit.

According to the CRISIL Report, as of FY23, MSME credit demand is estimated to be around Rs 117 lakh crore, of which 21% of demand was met through organized financing. Traditional banks don't have much exposure to underserved or unserved MSMEs and self-employed individuals in rural/ semi-urban, leading to credit gap and borrowers resorting to informal sources.

Gold loans

India's private gold holdings is highest in the world at 27000 tonnes ( vs China 16000tonnes). Most lenders become cautious during slowdown in economic growth. As a result, SME credit gets affected as established lenders tighten their underwriting standards. Gold loans serve as a quick alternative to fund short term emergency of customers.( 3month to 6month) Counter cyclical nature of gold loans provides a cushion and acts as an active hedge for overall growth of NBFCs which have a good portfolio mix of gold loans and other loans. Share of organized players is 63%

Gold loans Demand triggers

1.to fund working capital and personal requirements for rural

2.doorstep gold loans model

3. gap between unorganized lender ( lends at > 30% pa) and organized lender lending rates

4. improved rural penetration of bank/ NBFC

5. emergence of Fintechs

Top NBFCs in gold loans are Muthoot Finance, Manappuram Finance, IIFL Finance control majority of NBFC gold loan market.

SME Finance

The top 5 states including Uttar Pradesh, West Bengal, Bihar, Maharashtra and Tamil Nadu together account for around 50% of market. Prominent players focusing on SME Finance are SBFC Finance, Five Star Finance, AU SFB. All other major NBFCs , small finance banks are aggressively eyeing to grow in this segment.

Drivers

1.UPI led digital trails, online shopping, utility bill payments creating more data points

2. huge credit gap

3. sharp rise in new SME registrations in FY23

4. emerging fintech models partnering with NBFCs

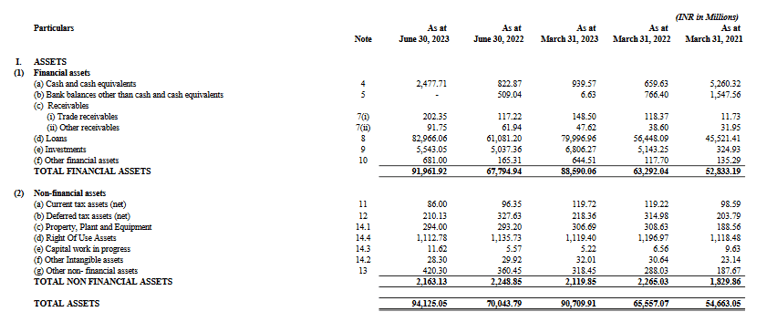

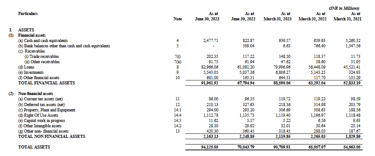

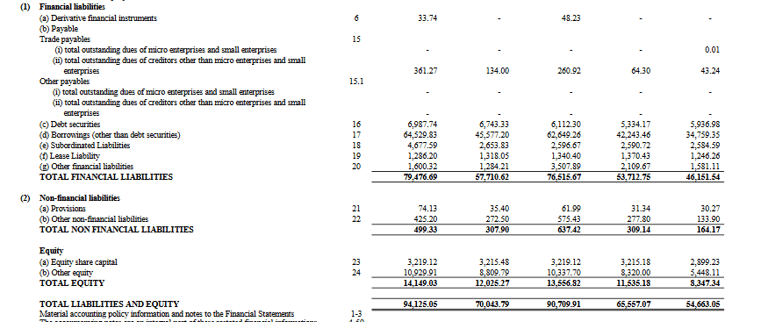

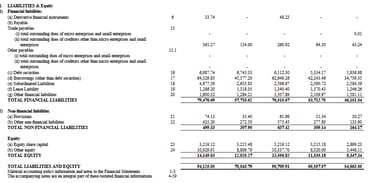

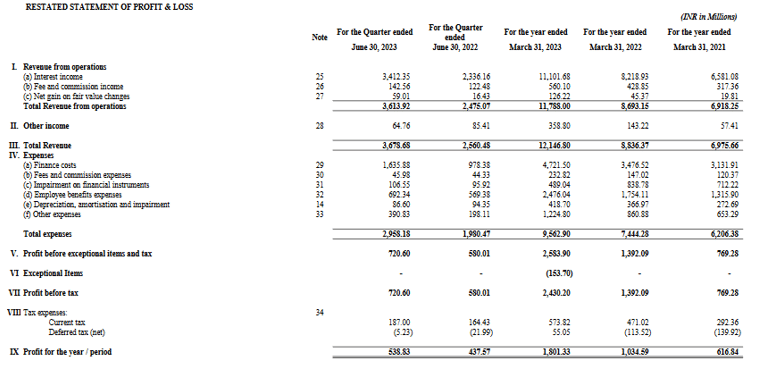

Financials

Total FY23 revenues of 1180cr . PAT 180cr ( 3 times in 2 years)

Operating profit 310cr ( has become 2 times in last 2 years ).

Impairments reduced from 71cr (FY21) to 49cr.

Comparable peer is IIFL ( though yields of IIFL are much higher, one must compare it with discretion)

Gross NPA is 2.26% in Q1 (increased from 2.03% FY23) ( peers SBFC 2.43%, IIFL 1.8%, Manappuram 1.3%)

GNPA FY22 2.22% , FY21 1.10%

NNPA Q1 1.76% ( FY23 1.59%, FY22 1.75%, FY21 0.71%) ( peers SBFC 1.41%, IIFL 1.1%, Manappuram 1.1%)

GNPA , NNPA has increased in Q1 vs FY23.

Financial ratios ( FY23)

Cost of funds 7.77% ( SBFC 8.2% , IIFL 8.7%)

Yield 15.7% ( SBFC 15.9%, IIFL 19.7%)

NIM 8.36% ( SBFC 7.7%, IIFL 15.8%)

Cost to income 51.5%

Credit cost 0.6% ( SBFC 0.6%)

ROA 2.3% (SBFC 2.9%, IIFL 3.3%)

ROE 14.3% (SBFC 9.9%, IIFL 9.8%)

CRAR 19.7% ( Tier 1 14.7%)

Points to consider

Having strong parentage (Federal Bank as promoter) will help Fedbank financial services to scale operations and in terms of risk management practices.

Very fast growth ( 33% AUM CAGR last 3 years) of loanbook was possible as it is less than 10000cr, may not be able to replicate this.

Though present in 17 states, 93% business comes from 6 states. But this style of deepening presence in few states is better than having few branches in all states.

Most loans are given to MSME and self employed, so economic downturns may affect Fedbank business more than other diversified NBFC.

Competition has heated up in gold loans segment - apart from NBFCs , banks are going aggressive in growing their gold loan book. Same for SME Finance. Deep rural network , non-traditional underwriting methods for sourcing unbanked customers will be defining competitive edge ( moat) for NBFCs like Fedbank Financial services vs others. As banks won't compete for unbanked deep rural customers.

Small finance banks have similar edge of serving unbanked customers, and are growing SME loanbook fast as they are moving from unsecured to secured.

Valuation

Fedbank Financial Services is valued at Price/ Book ratio 2.57.

Peers IIFL Finance at 2.3, SBFC Finance at 3.6

Detailed analysis of SBFC Finance ( recent IPO)

Follow us on twitter

You may be interested in

Utkarsh Small Finance Bank analysis

Will Jio Financial disrupt Bajaj Finance

How to avoid companies like Brightcom/ BCG ? Investing red flag

#themoatinvestor #dmoatinvestor #fedfinancialservicesipo #listinggain