Groww IPO Analysis

Operating metrics

Revenue per employee grew from Rs10.56 million in FY23 to Rs26.10 million in FY25, while our Adjusted EBITDA per employee grew from Rs3.85 million in FY23 to Rs15.43 million in FY25.

84% of customers were acquired organically in FY25. In Fiscal 2025, the average daily time spent on Groww platform by active Users (individually) was 65.50 minutes, engaging for a variety of reasons — to read the news, check their watchlists, make investments or monitor their portfolios. This engagement is reflected in their DAU/MAU ratio of Transacting Users, which was 56.29%. Groww's market share based on Retail Cash ADTO across BSE and NSE increased from 17.71% Q2 of FY25 to 21.60% for the Q3 FY25.

Gross margin for FY25 is 67.9%.

Employee count as on FY25 is 17,607, with a tech team of 491 members.

Marketing expenses stand at 6.7% of revenues. Capacity utilization is at 55%

Bifurcation of sales (according to channels)

Stores 80%

Own website/app 11.5%

Other online channels 8.5%

Contents

Business

Industry overview

Operating metrics

Financials

Points to consider

IPO Size/ Promoter holding/ Market cap

Purpose of IPO

Valuation

Business

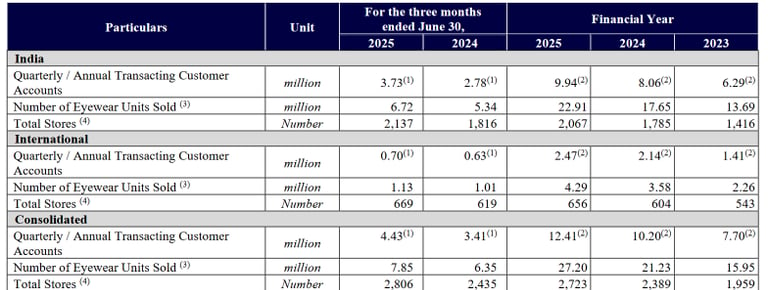

Groww is a technology-driven investment and wealth management platform offering a range of financial products — including equities, mutual funds, derivatives, IPOs, ETFs, bonds, and loans against securities. Customers can also avail margin trading facility and personal loans. It provides users with a unified digital interface via mobile app and web. Groww is promoted by Lalit Keshre, Harsh Jain, Ishan Bansal and Neeraj Singh-all colleagues at Flipkart. Groww is the largest stockbroker in India, which is a discount brokerage firm- meaning very minimal brokerage charges, started in 2016. Groww is India’s largest stock brokerage firm and fastest growing investment platform by active users on NSE as of June 30, 2025. As on June 30, 2025, the number of active users on NSE was 47.89 million, having grown approximately nine times from 2016. Further, Groww is the only investment app in India to cross 100 million cumulative downloads.

Groww has FY25 revenues of Rs 3900 cr. 45% of Active Users were less than 30 years and ~21% were between 31 - 35 years of age. The median age of active users was ~31 years. The number of Active Users grew at a CAGR of 52.74% from FY23 to FY25 . Groww is well-known across cities, towns and villages in India, with Active Users in 98% of pin-codes in India. 81% of active users are outside top 6 cities. Total Customer Assets on Groww platform grew at a CAGR of 91% from FY23 to FY25. Stocks (including customer funds deposited with Groww) accounted for 45% of the Total Customer Assets, and balance held in mutual funds.

2 year revenue CAGR of Groww is 89%.

Most of the technology developed is in-house. Their systems have the bandwidth to handle approximately 50 million users simultaneously and execute approximately 50 million orders per day.

Products

1. Broking Services

Their market share in retail Derivatives ADTO is 14% and retail Cash ADTO is 23.6%

2. Mutual funds

Groww is one of the foremost platforms for mutual funds distribution in India, with a 13% market share in SIP inflows. Groww offers direct-only mutual funds presently, where they do not charge customers for buying and selling units of mutual funds.

3. Margin Trading Facility ( MTF)

Groww has an outstanding MTF book of Rs 10,35cr which accounted for a 1.22% market share.

4. Consumer credit

Loans are distributed via 2 models:

Distribution model- Groww distributes personal loans to customers in partnership with third- party banks and NBFCs. The average loan per user was Rs 71,140 with an average tenure of approximately 15 months.

On-balance sheet - Subsidiary Groww Creditserv Technology Private Limited (GCS), holds a NBFC license through which they provide on-balance sheet personal loans. Average loan per user was Rs 204,000 with an average tenure of approximately 27 months. GCS had a loan book of Rs 1164 cr and an NPA Ratio of 1.67%

5. Wealth management

In September 2025, Groww completed the acquisition of Finwizard Technology Private Limited (FTPL).Through FTPL, we currently offer wealth management products such as distribution of Mutual Funds, PMS (including in-house manufacturing), insurance products. Active Customers on FTPL held assets aggregating to Rs 10170 cr. FTPL also employed 160 ‘Wealth partners' who are dedicated relationship managers, to provide personalized services to Affluent Customers.

Groww Asset Management

We forayed into asset management with acquisition of Indiabulls Asset Management Company Pvt Ltd in May 2023. Following this acquisition, they launched first NFO in June 2023 and currently offers 30 products, with 11 active funds and 19 passive funds (14 equity, 5 debt, 2 commodities, 8 ETFs, and 1 hybrid fund). Assets under management of Groww AMC stands at Rs 2520 cr currently.

Groww faces competition from other discount brokers like Zerodha, Angel One,Upstox and traditional brokers like Motilal Oswal, Sharekhan, ICICI Direct etc.

Financials

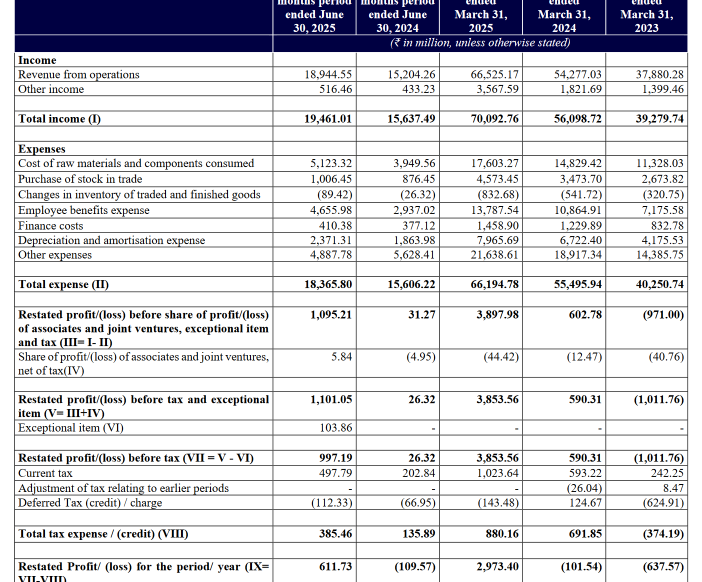

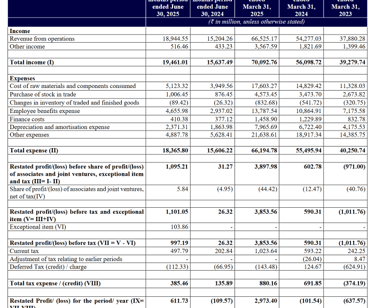

Total FY25 revenues of 7010cr .( Revenue CAGR 2 years 33.5%).

Titan Eye Plus revenues 800cr for FY25, EBIT Margin 10.7%

PAT Rs 30 cr vs Rs 10 cr loss last year.

Net cash flow from operations 1230cr.

Capex for FY25 is 420cr.

EBITDA margin 20%. ROCE 13.8%

Comparable peers Titan Eyewear division.

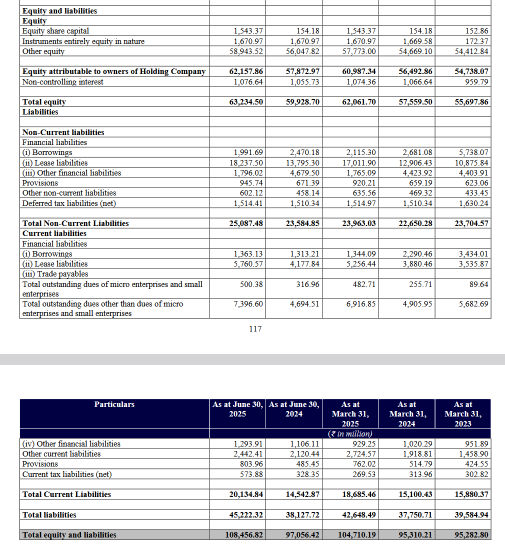

Goodwill 1875cr out of total assets 10845cr.

Receivables 140cr. Payables 790cr.

Inventory 1160cr. Cash 1970cr.

Borrowings 340cr. Equity 6320cr. Lease liabilities 2400cr.

Points to consider

77% of Indian market remains unorganized, with intense price competition which is a risk.

There is an integration risk from multiple acquisitions (Owndays, Stellio, Dealskart)

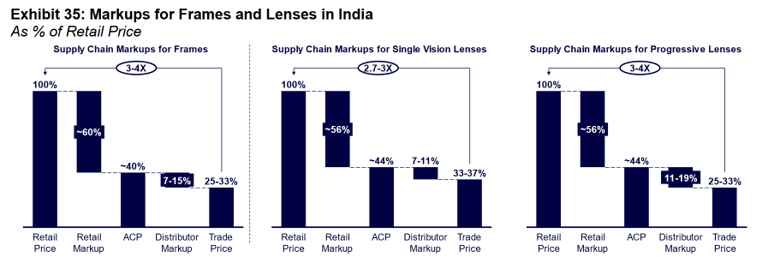

Supply chain dependency on raw material vendors for lenses/frames is there, raw materials constitute 25% of revenues. Significant portion of raw materials is imported from China- any tariffs , policy change will become a risk factor.

Due to lack of pan-India organized players , it presents an opportunity before Lenskart to capitalize on that.

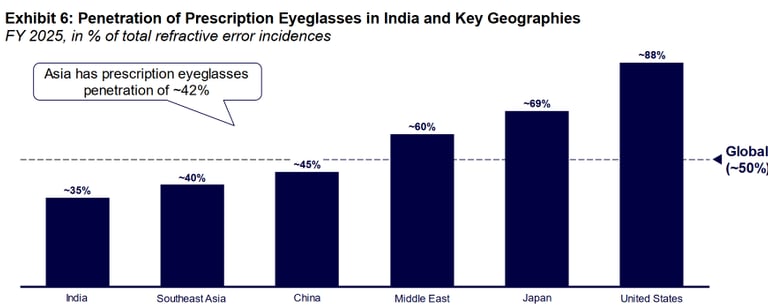

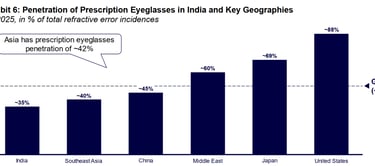

High incidences of refractive errors and low penetration of prescription eyeglasses at 35% presents a huge opportunity before organized players like Lenskart.

Rate of store closures have to be monitored. Out of 2806 stores in India, 111 stores were closed in FY25.

There is a technology risk where cost of LASIK surgeries goes down leading to affecting the prescription eyeglasses market for Lenskart.

IPO size /Promoter holding/ Market cap

Total offer 7280cr

Offer for Sale 5130cr

Fresh issue 2150cr

QIB- 75%

NII 15%

Retail 10%

Post listing promoter holding 17.5%

Price band- 382-402

Market cap post listing ~ 69730 cr

OFS sellers are SoftBank, Kedaara, Schroders, Alpha Wave, and the founding team

Purpose of IPO

Capital expenditure towards set-up of new CoCo stores in India 272cr

Expenditure for lease/rent/license agreements related payments for CoCo stores 591cr

Investing in technology and cloud infrastructure 213cr

Brand marketing and business promotion expenses 320cr

Valuation

Lenskart is valued at 285 P/E.

Follow us on twitter

You may be interested in

RR Kabel analysis

Hyundai Motors India analysis

Will Jio Financial disrupt Bajaj Finance

#themoatinvestor #dmoatinvestor #lenskart #listinggain

Industry overview

The Indian Investment & Wealth Management sector was valued at Rs 1.1 trillion as of March 2025, projected to grow to ₹2.2–₹2.6 trillion by FY2030, at a CAGR of 15–17%

Organized share is 23% (expected 31% by FY2030), leaving a huge scope of growth.

According to the “World Report on Vision” by the WHO published in October 2019, ~2.6 billion individuals were estimated to be affected by myopia and ~1.8 billion individuals by presbyopia. As per WHO estimates, these figures are projected to grow to ~3.4 billion and ~2.1 billion for myopia and presbyopia respectively by CY 2030P. The incidence of refractive errors has increased to ~4.0 billion (~49% of total population) in FY 2025 and is further projected to increase to ~4.7 billion (~55% of total population) by FY 2030P.

Major Growth Drivers:

-Increasing screen time leading to higher incidence of vision problems

-Rising disposable incomes, fashion eyewear adoption

-Expansion of organized retail and digital adoption

-Growing demand for affordable vision care in tier 2–3 cities

Penetration of prescription eyeglasses

Developed markets such as Japan and the United States have higher prescription eyeglasses penetration rates at ~69% and ~88% of the refractive error incidences, respectively, as of FY 2025, driven by better awareness, accessibility and affordability. Meanwhile, India lags with a penetration of ~35% of total refractive error incidences.

Low penetration of optometrists

Number of optometrists penetration is 35-50 per million population in India which is low compared to US - 110 . Optical store density is also low. Number of optical stores in India is 60 per million population whereas in US it is 130.

Average selling price of prescription eyeglasses is Rs 2370 in India as on FY25, that of sunglasses is Rs 1417,that of contact lenses Rs 219.