Pyramid Technoplast Business analysis

Business

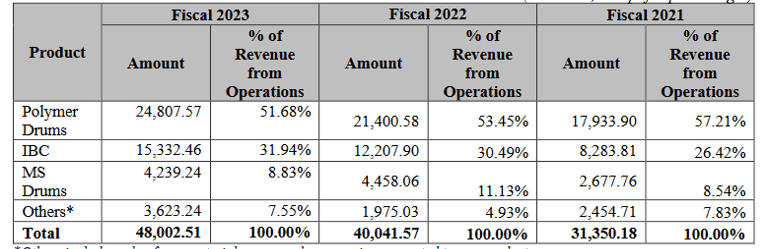

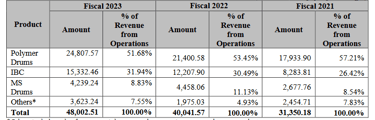

Pyramid Technoplast is an industrial packaging company started in 1997. It manufactures polymer based molded products (Polymer Drums) used for packaging. Products find their use in chemical, agrochemical, speciality chemical and pharmaceutical companies.They have 3 products-

Intermediate bulk containers (IBC) ( installed capacity 12800 MTPA)

Polymer drums ( installed capacity 20600 MTPA)

Mild steel drums ( installed capacity 6200 MTPA)

Total 6 manufacturing units spread across Gujarat ( 4) and Dadra & Nagar Haveli ( 2). 4 of the 6 plants are operating at capacity utilisation > 75%

Technology involved is blow moulding and injection moulding.Pyramid Technoplast is amongst the global leaders of IBC of 1000 l category.

The Polymer Drums market of India is projected to grow at 10% CAGR and the MS Drums market of India is projected to grow at 8% CAGR.

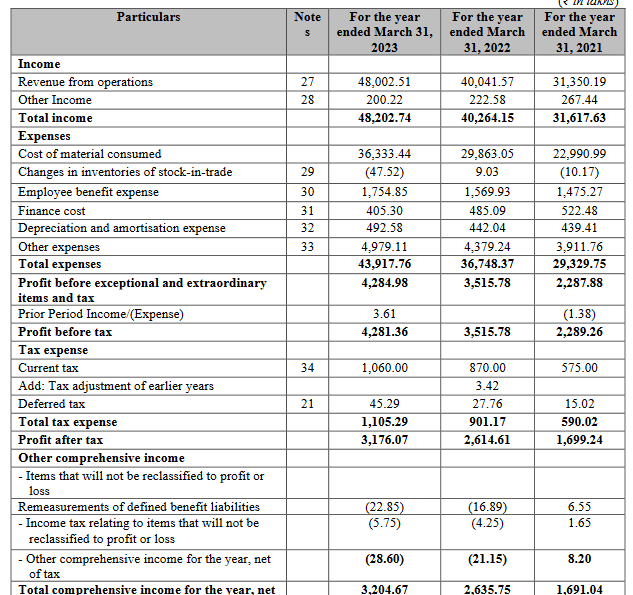

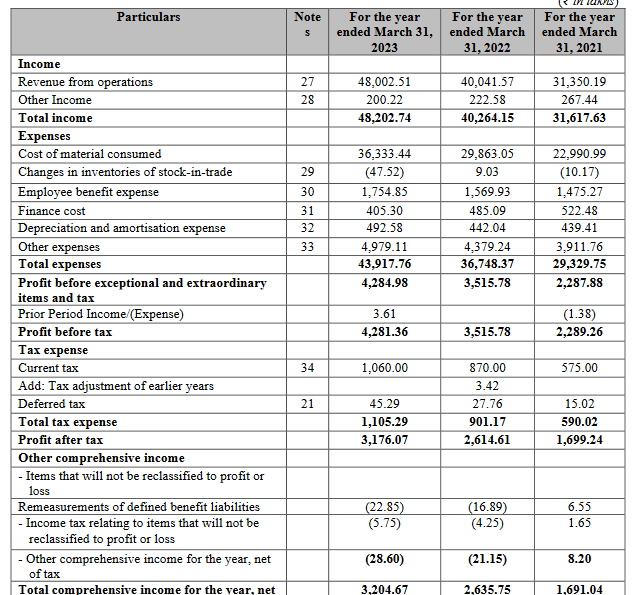

The chemicals industry is projected to grow at 9.3%Financials

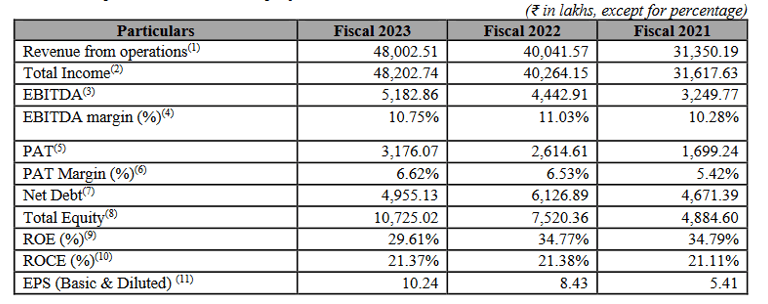

Profits have become 2X in last 3 years.

EBITDA margins are 10-11% ( Market leader Time Technoplast operates at 13%)

PAT margins have expanded from 5.5% to 6.6%

ROCE consistent at healthy 21%

75% of revenues is raw material cost.

Balance sheet

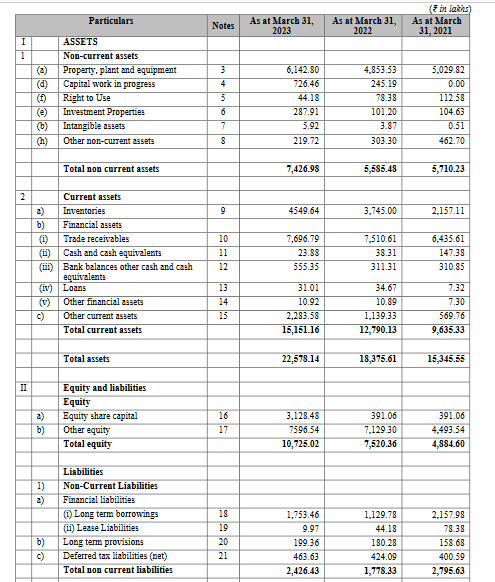

Trade receivables 77 cr , not high, considering it is a B2B business.

Cash/ cash equivalent is 5.8cr

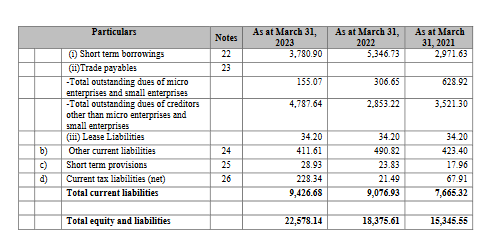

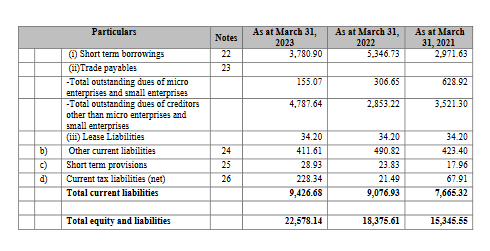

Total borrowings 55 cr ( 40cr from IPO will be used to reduce this debt)

Debt equity ratio 0.51

Cashflow from operations (CFO) of F23 adequate, but inadequate for last 2 years.

Points to consider

Raw materials are polymer including polypropelene and polyethylene, are imported by company from Middle- East countries, which are subject to fluctuations in crude oil prices.

Currently, they don't have any forex currency hedging practice for addressing crude volatility.

They purchase raw material under short term contracts only.

For MS drums, raw material is mild steel, which constitutes 80% of revenues of MS drums.

Working capital of the company is 90cr, and they have no balance in terms of cash/ cash equivalent, and generate PAT of 31 cr. So, as revenues grows, they will have to finance working capital needs through borrowing, as for capex, they will need the surplus generated from the profits, though they are getting 40cr from IPO for working capital that may suffice for near term.

Top 10 customers contribute 27% of revenues ( adequately diversified)

Valuation

Pyramid Technoplast is getting listed at P/E of 18

Market leader Time Technoplast trading at P/E of 14 ( high debt and low ROCE)

To learn more on IPO listing gains

How to do IPO analysis for listing gains

Aeroflex Industries IPO Analysis

#themoatinvestor #dmoatinvestor #pyramidtechnoplastipo