Options trading changing cyclicality of Broking Industry

87% of brokerage income of Angel is from F&O. 24% of NSE F&O turnover by Retail investors, 35% by prop traders. Find how cyclicality of brokerage income is getting changed

Total active clients on NSE 3.23 crore. Total demat accounts 11.4 crore

Upstox has lost most clients in last year, 52 lakh to 32 lakh, implying these 20 lakh might have opened accounts but not traded once in 1 year- people are opening accounts but not trading in that account.

Active clients vs Revenues trend

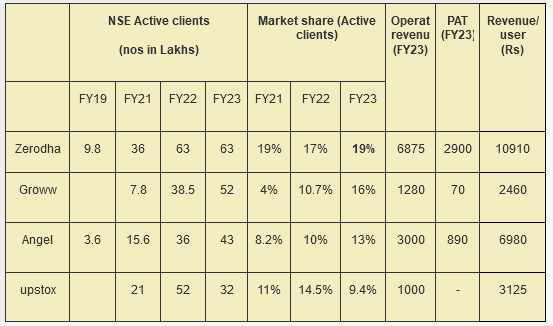

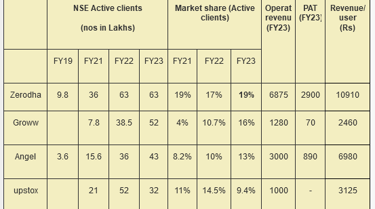

Until last year, Upstox and Groww were not able to convert their substantial client base into revenues, with similar client base Zerodha and Angel One are generating much higher revenues, which may lead to possibility of inferring that active traders who trade in high volumes are not using Groww & Upstox . ( as all are discount brokers having similar client base and similar brokerage, high volume/ trader will only lead to higher revenues, which will come from only traders who trade regularly)

Groww seems to have found a way to convert userbase into revenues in FY23,turning profitable for the first time. As we speak, Groww has toppled Zerodha in active userbase count as on Sept '23, which stands at 66.3 lakh ( Zerodha 64.8 lakh). While active userbase means nothing as we have seen- if Groww is unable to find ways to engage users meaningfully (where they find value in the platform),it is likely that serious traders will migrate to Zerodha or other platforms ( whose word of mouth is stronger, of course considering the fact the incumbents remain ahead in terms of features, technical glitches etc and does not get complacent)

Contents

- Dramatic shifts in NSE Active clients

- Active clients vs Revenues trends

- Rise of Angel One among traditional brokers

- ADTO trends- cash market vs F&O volumes

- So huge options volumes? Premium vs Notional turnover

- Who trades Equity F&O?

- Cash market turnover trends & Intraday leverage

- Decreasing cyclicality of discount brokerage firms' income

Dramatic shifts in NSE Active clients

There has been a huge shift in the NSE Active clients ( defined as persons who has traded at least once in last 1 year) post covid as we all observed. We have also heard about rising option traders. Let's get deeper into how these changing dynamics are impacting the broking industry , especially the discount brokerage firms- given that top 4 discount brokerage now control 57% of the market.

Surging profits of Zerodha for last 2 years, Groww turning profitable-, rise of Angel One- all these point to the fact that discount brokerage is the way forward- and all others including HDFC Securities ( Sky),Kotak (Neo), Paytm, Bajaj Finance, PhonePe are jumping into this. Considering only around 4 crore investors in India today, there is enough room for everyone to capture some share.

Number of active clients / Market share (F 23)

Zerodha 63 lakh / 19%

Groww 52 lakh /16%

Angel 43 lakh /13%

Upstox 32 lakh / 9.4%

ICICI Sec 25 lakh / 7.4%

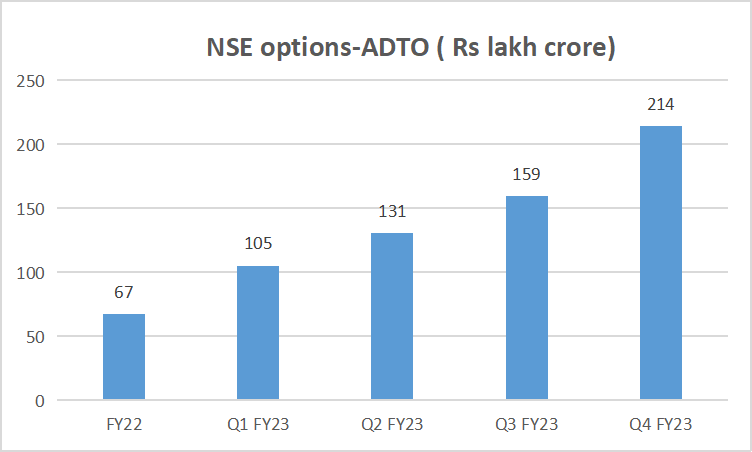

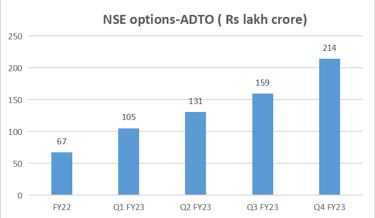

Average daily turnover- ADTO stands around Rs 156 lakh crore, which is driven by option trading volumes is increasing at breakneck speed, FY21 grew by 77% , FY22 grew by 266%, and in FY23 grew by 220% - back to back 3 years of very high growth, indicating a huge fresh inflow of new option traders in the market every year. But is this huge surge driven solely by retail investors? We will soon find out.

Point to be noted is, despite market being choppy in FY23 , ADTO has surged 220% in FY23 YOY.

So huge Options volumes? Premium vs Notional Turnover

Data given for options is notional turnover, which is often flawed way to look at options volumes. Let's say a stock priced Rs 1000 has lot size of 500, and premium of Rs30. So for trading 1 lot ( buy+sell), notional turnover comes as Rs (1000+30) 500x2=Rs 10.3 lakh. But premium turnover will be only Rs (500x30)x2=Rs 30000. Premium turnover is the amount actually paid for trading that option contract.

Total premium turnover of NSE comes at around 0.2-0.4% of notional turnover.

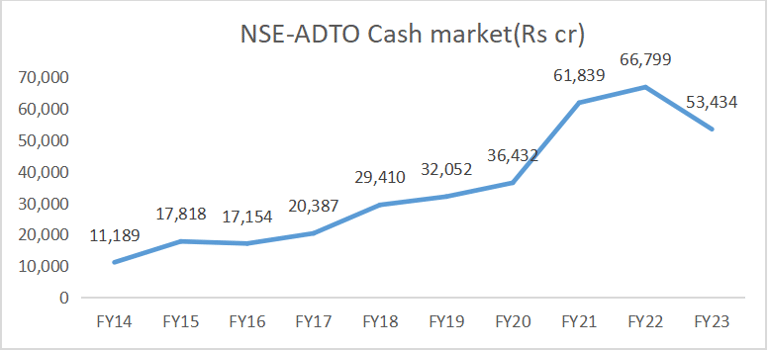

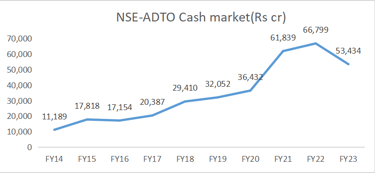

Cash market volume (decreased 21% YoY) may optically look negligible wrt options volumes. Nevertheless, looking at the exponential growth, option traders are not leaving the market as expected. Or fresh inflow of new traders is so high that it is offsetting the decline due to loss making traders leaving the market.

Observe in the quarterly trend options figures of FY23 above ( NSE options ADTO). Despite overall market in FY23 was choppy, and sentiments negative for significant part of the year, option trading volumes continued to surge quarter-on-quarter unabated.

Recent SEBI report released in Feb '23 reports based on trading data of top10 brokers revealed average 1.2 lakhs loss / F&O trader. 89% of F&O traders are in losses .

If that is the case, the bigger brokers will keep making money and industry will grow. Given the demographics ( most traders < 35 yrs age) , and huge number of youtube options videos, new traders will keep coming to market trying their luck with options. But the growth rate may moderate. 200% growth in ADTO is abnormal.

This reduces the cyclicality of the broking business income ( ideally broking businesses do well when markets are in bull run ). More on this as we go on.

Who trades Equity F&O?

Rise of Angel One among traditional brokers

Among traditional brokers, rise of Angel is phenomenal from only 1.6 lakh clients in FY15 to 43 lakh clients in FY23, since they shifted their strategy to digital only broker from F19 from being a traditional broker. They were on the bus just at the right time to ride the wave of option trading post covid, with hoardes of new investors flocking the market. Notably, unlike other 2 market leaders mentioned, they have been able to convert their customer base into revenues, as 30% of revenues in FY23 comes from newly acquired customers last year.

ADTO Trends - cash market vs F&O volumes

Out of 3.23 crore NSE active clients , estimated 45 lakhs are F&O traders. This was 7 lakh in F19, so 500% jump. 90% of 45 lakh are option traders, 11% futures.

Compared to FY20, retail+HNI reduced from 38.1% to 32.9%. Only retail traders constitute 23.9% F&O volumes in FY23( 25% in FY22). DIIs who formed 0.3% in FY20 are now at 5.1%. ( Here HNIs = partnership/LLP, trust, AIF etc)

So it's not that only retail traders are trading options,every participant including FIIs, DIIs, corporates have increased their presence in options markets.

Equity derivatives instrument wise

Index options 82%

Stock options 7%

Index futures 4%

Stock futures 8%

Cash market turnover trends & Intraday leverage norms